Latin America inbound M&A reached USD 40.6 billion across 600 deals in 2025, a 45% jump from 2024 driven by US, Spanish, and Chinese acquirers.

Buying a company in Latin America takes 6 to 9 months from letter of intent to close. The process covers strategy, target screening, valuation, due diligence, deal structuring, financing, and post-close integration. Brazil leads the region with 60% of deal value.

The Startup VC has operated portfolio companies like Biz Latin Hub across 17 Latin American countries since 2014. Craig Dempsey’s family office builds and acquires service businesses with hands-on operational support. This playbook shows acquirers how to source, value, and structure buy-side deals. It covers Brazil, Mexico, Colombia, Chile, and Peru. Learn more about our investment focus and how we partner with acquirers.

Why Should Acquirers Look at Latin America for M&A Deals?

Latin America offers acquirers rising deal volume and attractive EBITDA multiples. Proprietary deals face less competition than in North America. The region recorded around 2,650 M&A deals worth nearly USD 96 billion in the first 11 months of 2025. Total deal value rose 13% year over year.

The macro tailwinds are clear. US investment in LatAm M&A surged 407% to USD 11.8 billion in 2025. Spain followed at USD 8.4 billion across 28 deals. China invested USD 4.7 billion. About 62% of executives now say the M&A opportunity in Latin America has never been greater.

| Country | Deal Volume Share | Top Sectors |

|---|---|---|

| Brazil | 60%+ of regional value | Fintech, Energy, Industrial |

| Mexico | 15% | Manufacturing, IT, Retail |

| Chile | 8% | Mining, Energy, SaaS |

| Colombia | 6% | Financial services, IT |

| Peru | 4% | Mining, Consumer |

Five sectors drive deal flow in 2025:

- Fintech. Accounts for 24% of all LatAm M&A activity, the most active category.

- AI, data, and automation. Captures 17% of deals as buyers chase platform plays.

- IT services. Holds 13% share with nearshoring tailwinds from US clients.

- Utility and energy. Top dollar-value sector at USD 29.3 billion across 125 deals.

- Industrial products. Grew from 15% of deals in 2013 to 30% in 2023.

For acquirers backing portfolio platforms, see our investment focus page for sector and stage targets.

What Are the Main Steps to Buy a Company in Latin America?

You can buy a company in Latin America by following a seven-step process from strategy through post-close integration. The full process takes 6 to 9 months for mid-market deals. Brazilian deals can take longer because of antitrust review and central bank registration.

The seven steps are:

- Strategy and mandate. Define investment thesis, target size, geography, and sector.

- Target screening and outreach. Build a target list of 50 to 200 companies via bankers, brokers, and proprietary research.

- LOI and exclusivity. Issue a non-binding letter of intent after CIM review; lock in 60 to 90 days of exclusivity.

- Due diligence. Run financial, legal, tax, labor, and operational diligence in parallel.

- Deal structure and SPA. Negotiate share purchase agreement, escrow, earnouts, and reps and warranties.

- Regulatory clearance and closing. File with CADE in Brazil, COFECE in Mexico, or FNE in Chile if thresholds apply.

- Post-merger integration. Onboard management, align operations, and execute the value-creation plan.

| Stage | Typical Duration | Key Output |

|---|---|---|

| Strategy and mandate | 4 to 8 weeks | Investment thesis, target criteria |

| Target screening | 8 to 12 weeks | Shortlist of 10 to 20 targets |

| LOI to exclusivity | 2 to 4 weeks | Signed LOI, NDA, data room access |

| Due diligence | 6 to 10 weeks | DD report, red flag list |

| SPA negotiation | 4 to 8 weeks | Signed SPA, escrow agreement |

| Regulatory and closing | 4 to 12 weeks | Antitrust clearance, funds flow |

| Post-close integration | 90 to 180 days | Integration plan, 100-day report |

Information gaps are the biggest LatAm-specific risk. Public registries are often outdated. Many strong companies operate under the radar without audited financials. Brazilian share deals of USD 100,000 or more must register with the Central Bank of Brazil (BACEN).

For detailed walkthroughs of each step, read our guides to finding acquisition targets in Latin America and performing due diligence in Latin America.

How Do You Find and Screen Acquisition Targets in Latin America?

You can find acquisition targets in Latin America by combining banker-driven auctions with proprietary outreach to off-market owners. Brokered deals bring you marketed opportunities at higher valuations. Proprietary deal flow opens access to off-market companies invisible in standard channels.

Five sourcing channels work in LatAm:

- Regional investment banks. BTG Pactual, Itau BBA, Bradesco BBI, and Santander run most mid-market auctions.

- Local M&A boutiques. Country-specialist firms handle owner-operator deals under USD 50 million.

- Family office and PE networks. Patria, Advent International, and L Catterton share deal flow informally.

- Search funds and ETA platforms. Search-fund operators look for owner succession deals in USD 5 to 30 million range.

- Direct proprietary outreach. Cold outreach to founders identified via industry databases, LinkedIn, and trade associations.

What Screening Filters Should Buyers Apply?

Buyers should apply five screening filters before deeper review. Filters cut a long list of 200 candidates down to 10 to 20 priority targets. Time spent on screening saves diligence cost later.

The five filters are:

- Minimum EBITDA. Most institutional buyers screen for USD 1 million in EBITDA or higher.

- Recurring revenue. Subscription, contract, or long-tenure customer base preferred.

- Founder succession. Owners aged 55 plus or seeking exit accelerate timeline.

- Geographic concentration. Single-country or single-city focus simplifies diligence.

- Strategic fit. Add-on potential to existing platform, sector overlap, or talent acquisition.

How Do You Build a Proprietary Pipeline?

You can build a proprietary pipeline by mapping the universe, prioritizing by fit, and reaching owners directly. The pipeline approach takes 12 to 18 months to mature. It produces deals at 1 to 2 turns of EBITDA below auction prices.

Steps to build a pipeline:

- Map the universe. Use databases like S&P Capital IQ, Pitchbook, and local registries to list every target by sector and country.

- Score by fit. Rank candidates on revenue, EBITDA, ownership age, and strategic relevance.

- Make first contact. Send a personalized note from a senior partner; reference specific business attributes.

- Nurture relationships. Quarterly check-ins over 12 to 24 months until the owner is ready to transact.

How Do You Value a Target Company in Latin America?

You can value a Latin American target by combining three methods. Use EBITDA multiple comparables, DCF with a country risk premium, and precedent transactions. EBITDA multiples are the most common starting point for mid-market deals. DCF analysis matters more for high-growth or cyclical businesses.

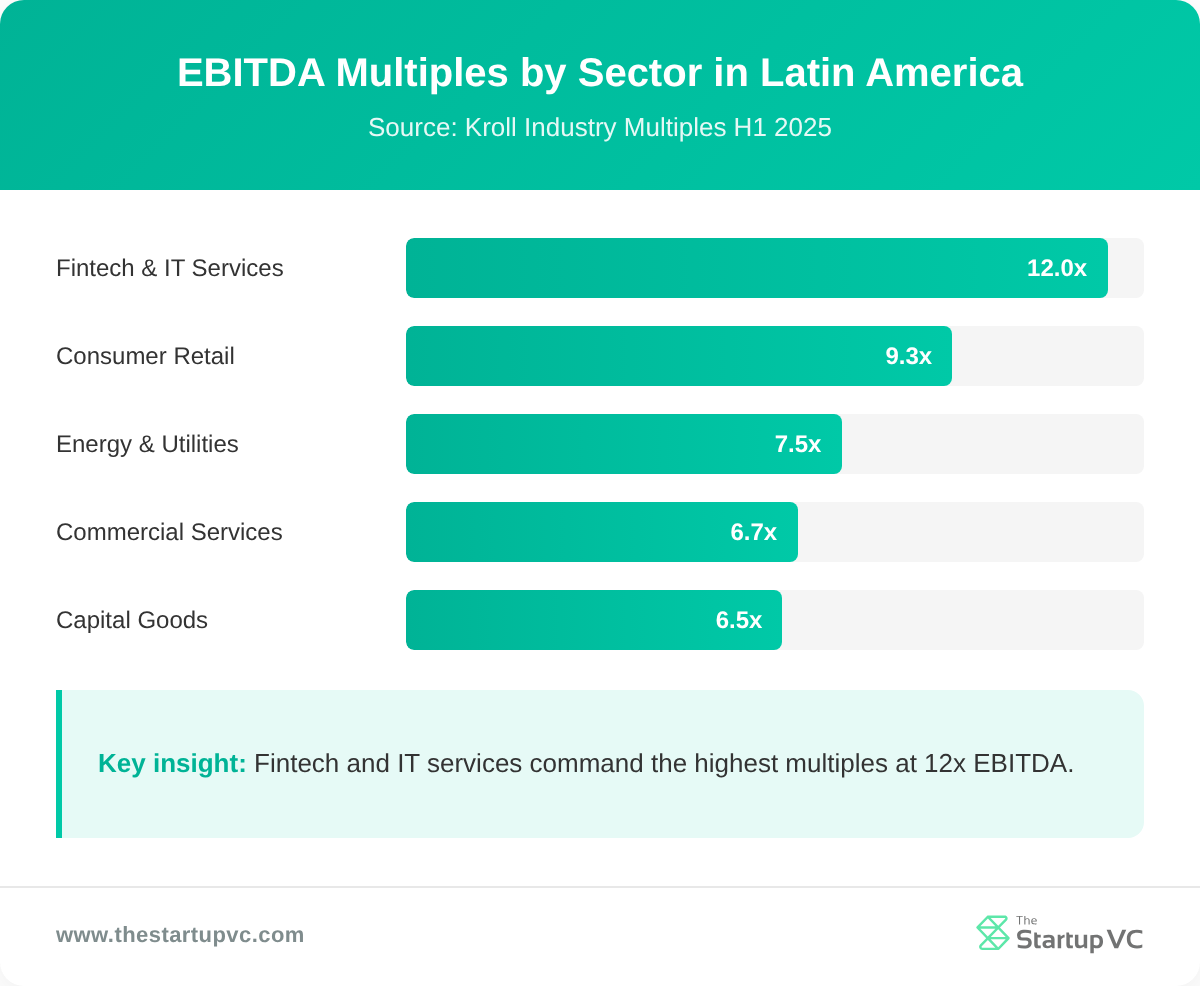

What EBITDA Multiples Apply in Latin America?

EBITDA multiples in Latin America vary by sector and held stable in the first half of 2025. The median LatAm EV/EBITDA multiple ranges from 6x to 10x depending on industry. Multiples sit roughly 2 to 4 turns below US averages.

| Sector | Median EV/EBITDA (H1 2025) | Change vs. 2024 |

|---|---|---|

| Consumer discretionary retail | 9.3x | +3.0 |

| Materials | 6.0x | -1.3 |

| Capital goods | 6.5x | -1.8 |

| Commercial and professional services | 6.7x | -1.8 |

| Energy and utilities | 7.5x | Stable |

| Fintech and IT services | 10x to 14x | +1.0 |

Source: Kroll Industry Multiples Latin America Q1-Q2 2025.

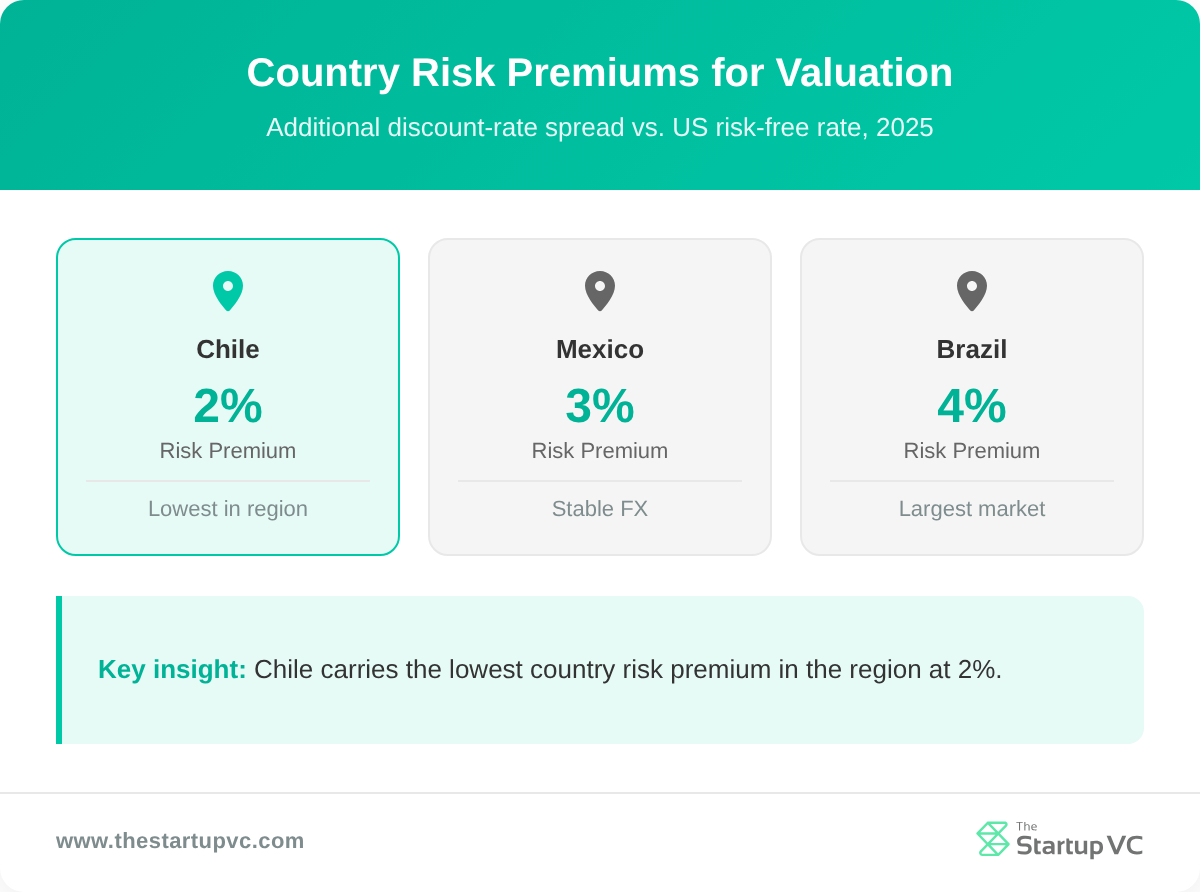

How Do You Adjust for Country Risk?

You can adjust for country risk by adding a country-risk premium to your discount rate. The country risk premium reflects sovereign default risk, currency volatility, and political instability. Premiums range from 2% to 12% across the region.

Country risk premiums in 2025:

- Chile. Around 2% above the US risk-free rate.

- Mexico. Around 3%.

- Brazil. Around 4%.

- Peru. Around 5%.

- Colombia. Around 6%.

- Argentina. Around 12% because of high inflation and capital controls.

LatAm real GDP growth is forecast at 2.5% in 2025, up from 2.2% in 2024. Higher growth supports valuation premiums for stable cash-flow businesses. For a deeper guide, see how to value a company in Latin America.

How Do You Perform Due Diligence in Latin America?

You can perform due diligence in Latin America by running five workstreams in parallel: financial, legal, tax, labor, and operational. Each stream needs local counsel in the target country. The full diligence cycle takes 6 to 10 weeks.

What Are the Five Core Diligence Workstreams?

The five core workstreams cover the highest-risk areas for LatAm buyers:

- Financial. Quality of earnings, working capital, debt-like items, normalized EBITDA.

- Legal. Corporate records, material contracts, litigation, intellectual property, regulatory compliance.

- Tax. Income tax, VAT, transfer pricing, social security, withholding obligations.

- Labor. Employment contracts, benefits, social charges, union obligations, dismissal contingencies.

- Operational. Customer concentration, supplier dependence, technology, ESG, real estate.

Labor liability is the highest-frequency hidden risk. Informal contracts and unpaid social charges transfer to buyers. Public registries are often incomplete. Reputational due diligence on owners and key managers is essential.

What LatAm-Specific Red Flags Should Buyers Watch?

Buyers should watch for six red flags unique to Latin American targets:

- Informal employment. Workers off the books still create future labor claims.

- Successor tax liability. Brazilian asset deals trigger inherited tax and labor obligations.

- Anti-bribery exposure. FCPA, UK Bribery Act, and Brazil’s Lei Anticorrupcao apply to cross-border deals.

- Currency mismatch. Revenue in local currency with USD debt creates hedging risk.

- Related-party transactions. Owner-operated businesses often mix personal and corporate expenses.

- Environmental liability. Mining, agriculture, and manufacturing carry decade-long cleanup risk.

For deeper coverage, read our full guide on how to perform due diligence in Latin America.

How Do You Structure a Cross-Border Acquisition in Latin America?

You can structure a cross-border acquisition in Latin America by making three choices. Choose between share and asset deals, select a holding company jurisdiction, and price the deal with earnouts and escrow. Structure choices drive tax outcomes, regulatory burden, and successor liability. Most deals use a local SPV held by a foreign parent.

Share Deal vs. Asset Deal: Which Works Better?

Share deals work better in most LatAm jurisdictions because they avoid successor tax liability. A share deal transfers ownership of the legal entity. The buyer inherits all assets and all liabilities of the target. An asset deal transfers selected assets and contracts only.

| Factor | Share Deal | Asset Deal |

|---|---|---|

| Tax basis step-up | No | Yes |

| Successor liability | Inherited fully | Limited (but full in Brazil) |

| Speed to close | Faster | Slower, contract by contract |

| Regulatory friction | Lower | Higher (asset transfer permits) |

| Best for | Mexico, Chile, Colombia | Argentina, distressed Brazil targets |

Brazilian asset deals still carry successor liability for pre-closing tax, labor, consumer, and environmental obligations. This makes share deals the default in Brazil despite tax basis disadvantages.

What Holding Company Jurisdictions Work for LatAm Deals?

Five holding jurisdictions dominate LatAm acquisition structuring:

- Netherlands. Tax treaty network with Brazil, Mexico, and most LatAm countries.

- Luxembourg. Strong for Brazilian and Argentine targets; flexible debt structures.

- Spain. Best for Mexican targets due to favorable Spain-Mexico treaty.

- Delaware. Default for US acquirers; works well when no LatAm treaty applies.

- BVI and Cayman. Common for PE funds; less favorable post-OECD transparency rules.

For a deeper breakdown of jurisdictions and structures, see cross-border acquisition structure in Latin America.

What Antitrust and Regulatory Filings Apply?

Antitrust filings add 30 to 90 days to the M&A timeline. Filings apply when deal size or market share exceeds country thresholds.

Key regulators:

- CADE (Brazil). Mandatory filing for deals where combined revenue exceeds BRL 750 million and target revenue exceeds BRL 75 million.

- COFECE (Mexico). Threshold-based filing for deals over MXN 1.36 billion or 35% market share.

- FNE (Chile). Filing required when combined sales exceed UF 2.5 million.

- SIC (Colombia). Filing for deals over assets thresholds tied to monthly minimum wages.

- INDECOPI (Peru). New merger control regime active since 2021.

What Deal Terms Bridge Valuation Gaps?

Earnouts bridge valuation gaps when buyer and seller disagree on price. Typical LatAm earnouts cover 20% to 40% of purchase price over 2 to 3 years.

Common deal terms in LatAm:

- Escrow. 10% to 20% of price held for 12 to 24 months against indemnity claims.

- Earnout. 20% to 40% tied to revenue, EBITDA, or specific milestones.

- Reps and warranties insurance. Increasingly common; premiums 2% to 4% of coverage.

- Working capital adjustment. Standard true-up at closing.

- MAC clause. Material adverse change protection between signing and closing.

How Do You Finance an Acquisition in Latin America?

You can finance an acquisition in Latin America by combining equity, seller financing, private credit, and limited bank debt. Leveraged buyouts are rare because of currency volatility and high local interest rates. Most LatAm deals are equity-heavy with selective debt overlay.

What Are the Main Sources of Acquisition Capital?

Five sources of acquisition capital dominate LatAm deals:

- Private equity. Advent International, Patria, General Atlantic, L Catterton, and Vinci Partners lead regional PE.

- Family offices. Single-family and multi-family offices increasingly active in mid-market.

- Search fund capital. Backers fund individual searchers for owner-succession deals under USD 30 million.

- Bank debt. Local banks offer term loans at 12% to 18% in BRL or MXN; USD debt at 8% to 12%.

- Seller financing. Deferred payments and seller notes cover 10% to 30% of purchase price.

How Does Private Credit Change the Picture?

Private credit is reshaping LatAm acquisition financing in 2025. Over 40 active private debt investors operate across Mexico, Brazil, Colombia, Chile, and Argentina. Private credit globally crossed USD 1.5 trillion AUM in 2024.

| Capital Source | Typical Deal Size | Cost of Capital | Best For |

|---|---|---|---|

| PE equity | USD 25M+ | 18-25% IRR target | Platform deals |

| Search fund | USD 5-30M | 25-35% IRR target | Owner succession |

| Family office | USD 5-100M | 15-20% IRR target | Long-hold platforms |

| Local bank debt | USD 1-50M | 12-18% local FX | Asset-backed deals |

| Private credit | USD 10-200M | 9-14% USD | Unitranche financings |

| Seller note | USD 1-50M | 6-10% | Bridge financing |

Currency volatility requires hedging instruments. High local interest rates make USD debt cheaper than local debt for cash-flow-positive targets. Search funds and family offices fill the gap left by scarce leveraged debt.

For a complete breakdown of financing structures, see how to finance an acquisition in Latin America.

What Questions Do Acquirers Ask Most Often About M&A in Latin America?

How long does an acquisition take in Latin America?

An acquisition in Latin America takes 6 to 9 months from signed LOI to close for mid-market deals. Antitrust review adds 30 to 90 days. Brazilian deals also require Central Bank of Brazil (BACEN) registration.

How much does it cost to buy a company in Latin America?

Transaction costs run 2% to 5% of deal value for mid-market acquisitions. Advisory fees take 1% to 3%. Legal, tax, and due diligence fees add 0.5% to 1.5%. Reps and warranties insurance adds 2% to 4% of coverage when used.

Which countries are the most active for M&A in Latin America?

The most active countries for M&A in Latin America are Brazil, Mexico, Chile, Colombia, and Peru. These five account for over 85% of regional deal volume. Brazil alone holds more than 60% of total deal value.

Do foreign buyers need local partners in Latin America?

Foreign buyers do not need local partners in most Latin American countries. Foreign ownership of 100% is allowed in nearly all sectors. Restricted sectors include media, certain border-zone real estate, and natural resource extraction in some countries.

What is the biggest risk in buying a Latin American company?

The biggest risk in buying a Latin American company is hidden labor liability. Informal contracts, unpaid social charges, and dismissal contingencies transfer to buyers in share deals. Brazilian asset deals also inherit pre-closing tax and labor obligations.

How do you handle currency risk in cross-border acquisitions?

You can handle currency risk by funding the deal in local currency where the target operates. Forward contracts and currency swaps hedge transaction-stage exposure. Operating cash flows in matching currency reduce ongoing FX mismatch.

Ready to Acquire a Company in Latin America?

Buying a company in Latin America rewards acquirers who combine local diligence with operational discipline. The Startup VC is Craig Dempsey’s family office and company builder. Our team operates portfolio companies across 17 Latin American countries through Biz Latin Hub. We back acquirers with on-the-ground entity setup, hiring, compliance, and integration support.

To discuss a buy-side mandate, deal sourcing, or post-close operating support, meet Craig Dempsey or Contact us today.