Cross-border M&A in Latin America hit USD 40.6 billion across 600 inbound deals in 2025.

Latin America recorded 2,650 M&A deals worth USD 96 billion in the first 11 months of 2025. Brazil captured 60% of regional deal value. US buyers led with USD 11.8 billion, followed by Spain at USD 8.4 billion.

The Startup VC is Craig Dempsey’s family office and company builder. Portfolio company Biz Latin Hub operates across 17 Latin American countries. Buy-side structure decisions set the tax basis and cash repatriation path for the next decade. This guide covers vehicles, treaties, holding jurisdictions, FX rules, and pre-close restructuring.

What Is a Cross-Border Acquisition in Latin America?

A cross-border acquisition in Latin America is a deal where a foreign buyer purchases a Latin American target. The deal runs as a share sale, asset sale, or merger. Structure choice drives tax exposure, FX registration, and how cash moves back to the parent.

Cross-border deals made up about 50% of total Latin America M&A volume in 2025. Inbound activity grew 45% by value, from USD 27.9 billion in 2024 to USD 40.6 billion in 2025. Deal count rose from 365 to 600 inbound transactions.

Brazil leads the region with 60% of deal value and 55% of transaction volume. Chile, Mexico, Colombia, Argentina, and Peru follow by volume. US strategic and financial buyers drove the surge, with deal value up 407% year over year.

Structure decisions matter because rules differ sharply across countries. An asset purchase that works in Mexico can trigger successor liability in Brazil. A Cayman holding that fits a US fund may break treaty access in Chile. For a fuller view of the broader buy-side process, see our guide on how to buy a company in Latin America.

Which Acquisition Vehicles Work Best for Buying a Latin American Target?

The best acquisition vehicles for Latin American targets are the share purchase, asset purchase, and statutory merger. Share deals dominate in Brazil, Mexico, and Chile because of liability and tax efficiency.

Each structure carries trade-offs:

- Share purchase. The buyer acquires the target’s equity and steps into all existing rights, contracts, and liabilities. Lowest restructuring cost but inherits all skeletons.

- Asset purchase. The buyer picks specific assets and liabilities. Cleaner risk profile but triggers transfer taxes, contract reassignments, and often successor liability.

- Statutory merger. The target merges into a buyer entity or vice versa. Used for in-country roll-ups but rarely for first-time foreign buyers.

Brazil deserves a separate flag. Asset deals expose buyers to joint or subsidiary successor liability for pre-closing tax, labor, consumer, and environmental obligations. Brazilian law also requires a post-closing purchase price allocation between tangible assets, intangibles, and goodwill, which sets the deductibility profile.

Antitrust review adds time across jurisdictions. Filings with CADE in Brazil, CNA in Mexico, or FNE in Chile add 30 to 90 days to closing. Mexico’s CNA replaced COFECE in July 2025.

| Country | Most Common Vehicle | Key Risk Flag |

|---|---|---|

| Brazil | Share purchase | Successor liability on asset deals |

| Mexico | Share purchase | Antitrust filing with CNA |

| Chile | Share purchase | FNE merger control |

| Colombia | Share purchase | SIC merger control plus FX registration |

| Panama | Share purchase | Used as holding jurisdiction |

How Do You Choose a Holding Company Jurisdiction for LatAm Deals?

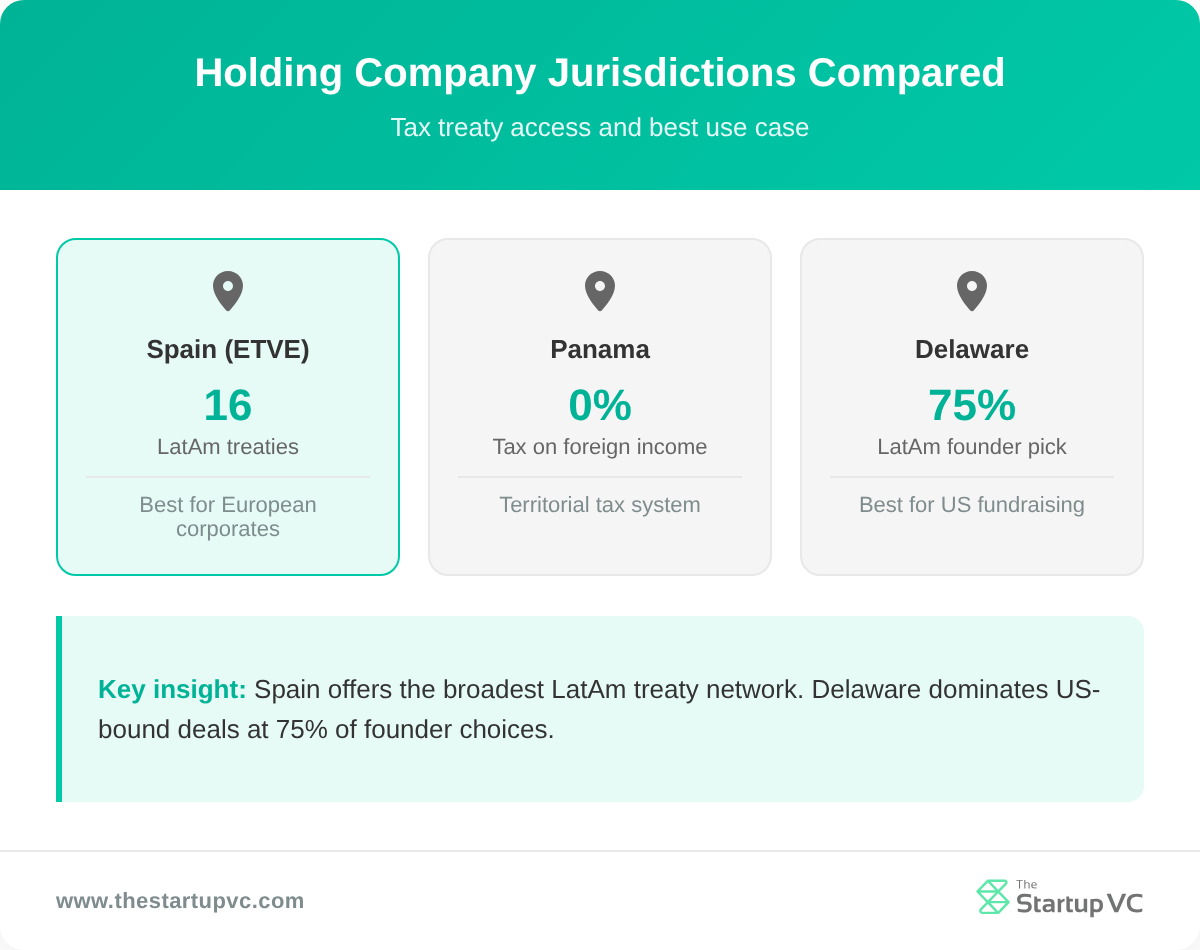

You choose a holding company jurisdiction by matching tax treaties, substance rules, and investor expectations to the target country. The most-used jurisdictions are Delaware, Panama, Spain, the Netherlands, and Luxembourg.

Each option has a distinct profile. The fit depends on whether the buyer is a US fund, a European corporate, or a family office.

Why Do Latin Founders Use Delaware Holdings?

Delaware is used by 75% of Latin American founders raising US capital. Investor familiarity and the Court of Chancery drive the choice. Another 24% use the Cayman/LLC sandwich for the same reason.

Delaware imposes no state corporate income tax on income from out-of-state subsidiaries. The General Corporation Law is the global benchmark for shareholder rights. Y Combinator’s preference cemented Delaware as the default for US-bound LatAm startups.

Delaware works best when the buyer expects future US fundraising. The trade-off is no treaty network with LatAm countries, which raises withholding tax on dividends and royalties.

When Does a Panama Holding Make Sense?

A Panama holding makes sense when the buyer wants territorial taxation and is not bound to US treaty needs. Panama’s S.A. and Private Interest Foundation are common asset-holding vehicles.

Under Panama’s territorial tax system, foreign-source income is exempt from local tax. The Sociedad Anónima needs no minimum capital, though USD 10,000 is recommended. Private Interest Foundations work for estate planning, asset protection, and as holding companies for shares in other entities. For a deeper look at Panama’s broader business market, see our Panama startup hub guide.

Panama sits on the EU non-cooperative list as of 2026. This can affect withholding tax treatment from EU sources. US, Mexican, and intra-LatAm buyers face fewer hurdles.

Why Use a Spanish ETVE for LatAm Investments?

A Spanish ETVE works for LatAm investments because Spain has the world’s most extensive treaty network with Latin America. Spain holds treaties with Argentina, Brazil, Chile, Colombia, Mexico, Panama, and 10 more LatAm jurisdictions.

The Entidad de Tenencia de Valores Extranjeros regime exempts qualifying foreign dividends and capital gains from Spanish corporate tax. Dividends from the ETVE to non-resident shareholders carry no Spanish withholding. The Spain-Mexico, Spain-Chile, and Spain-Colombia treaties cut LatAm-source withholding rates well below domestic levels.

European corporates and family offices use ETVEs as a regional holdco. The structure works less well when the ultimate investor sits in a treaty-poor jurisdiction.

| Jurisdiction | Tax Treaty Network with LatAm | Best Fit |

|---|---|---|

| Delaware | Limited (US treaties only) | US-bound buyers and funds |

| Panama | Limited but territorial | Asset holding and estate planning |

| Spain (ETVE) | 16 LatAm treaties | European corporates investing across LatAm |

| Netherlands | Strong | Large multinationals with EU substance |

| Luxembourg | Strong | EU funds and large groups |

How Do Tax Treaties Affect Cross-Border Acquisition Structure in Latin America?

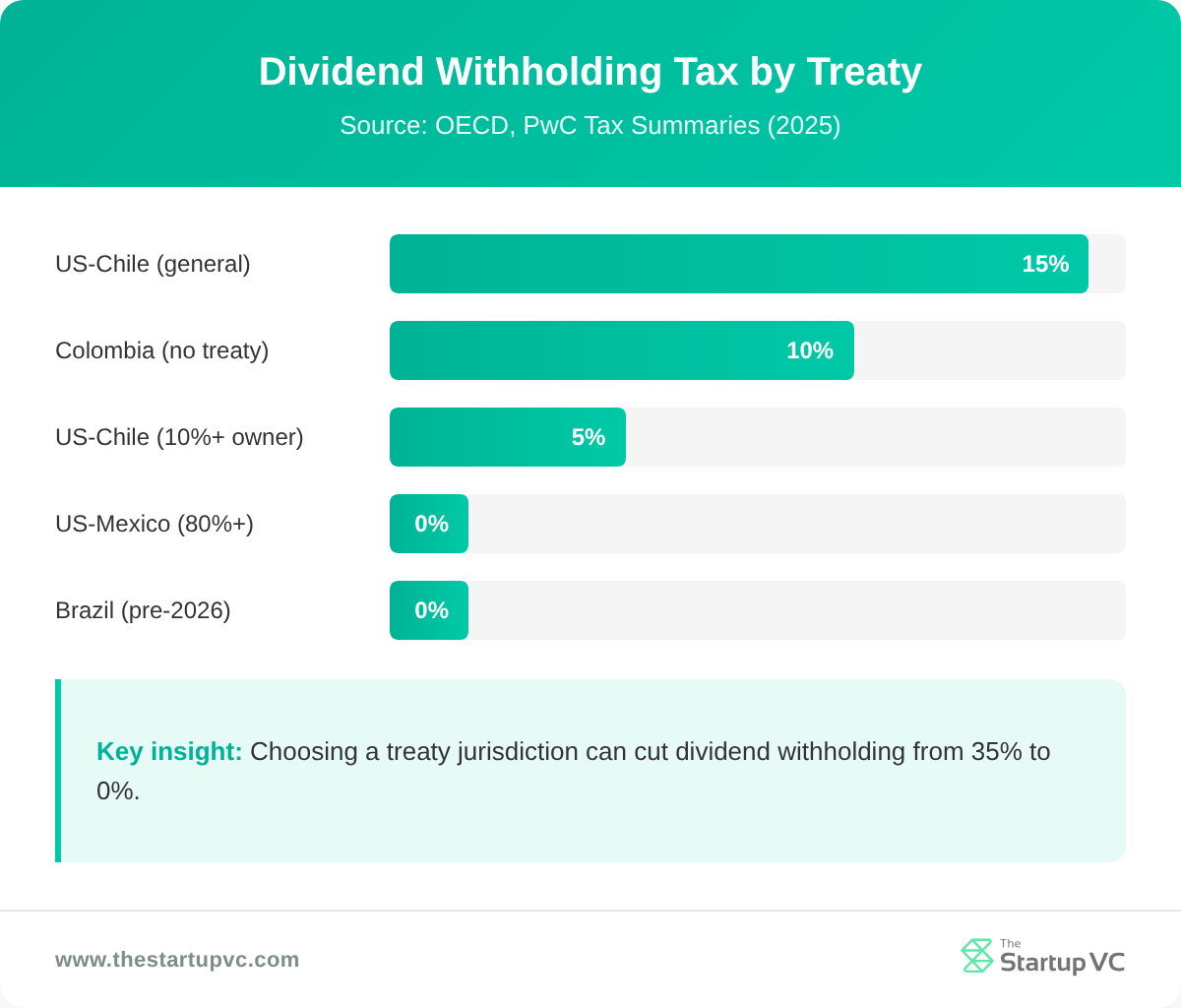

Tax treaties affect cross-border acquisition structure by cutting withholding tax on outbound cash flows. They reduce the tax on dividends, interest, and royalties from target to holding company. The right treaty saves 10 to 25 percentage points per dollar repatriated.

The biggest impact is on dividend withholding. Without a treaty, Latin American source countries can withhold 10% to 35% on outbound dividends. Treaty rates often drop to 5% or 0%.

Key treaty rates to know:

- US-Chile treaty (2024). Caps dividend withholding at 15%. A 5% reduced rate applies when a corporate owner holds at least 10% of voting stock.

- US-Mexico treaty. Grants a full withholding exemption on dividends paid by 80%-or-more owned Mexican subsidiaries to US parents.

- Colombia. Imposes 10% dividend withholding on profits already taxed at corporate level, unless a tax treaty reduces the rate.

- Brazil MLI. The Multilateral Instrument takes effect January 1, 2026, modifying treaties with Canada, Chile, Mexico, Portugal, South Korea, and Switzerland.

Spain’s network is the standout. With treaties covering 16 LatAm countries, a Spanish ETVE often delivers the lowest blended withholding rate for European groups. To learn more about The Startup VC’s investment approach, visit our investment focus page.

Substance rules matter too. Many treaties now include principal purpose tests. A pure paper holding with no employees, no office, and no decision-makers risks being denied treaty benefits.

How Do You Manage FX, Capital Controls, and Repatriation After Closing?

You manage FX, capital controls, and repatriation by registering the inbound investment with the local central bank. You also channel all cash flows through authorized FX intermediaries. Failure to register blocks future repatriation of capital, dividends, and royalties.

Each country has its own rules:

| Country | Registration | Recent Change |

|---|---|---|

| Brazil | IED module at Central Bank | IOF-FX on repatriation cut to 0% in June 2025 |

| Colombia | Banco de la República Form F4 or F5 | New digital SIC platform live in 2025 |

| Argentina | Central Bank registration | Most FX controls lifted April 2025 |

| Mexico | None for FDI | Free FX market |

| Chile | None for FDI | Free FX market |

Brazil’s IED registration with the Central Bank’s Foreign Direct Investment module is the gateway to repatriation. Without registered capital, buyers cannot remit dividends or sell shares back to foreign accounts. In June 2025, Brazil cut the IOF-FX tax on repatriation flows to 0%. The rate sits in a Provisional Measure pending Congress conversion.

Brazil also brings new dividend rules. Law 15,270/2025 imposes a 10% dividend withholding tax starting 2026 on distributions above BRL 50,000 per month. Dividends from profits earned through December 2025 stay exempt if distribution is approved by year-end 2025.

Argentina shifted sharply in 2025. The government lifted most currency controls on April 14, 2025, letting individuals and businesses buy US dollars without restriction. Non-residents can now repatriate direct investments without prior Central Bank approval. The capital must have settled through the FX market after April 21, 2025. A 180-day holding period also applies.

Colombia requires every foreign investor to register with Banco de la República using Form F4 or F5. The new digital SIC platform speeds processing but increases penalties for late filings or incorrect reporting. Delays here block repatriation and trigger fines.

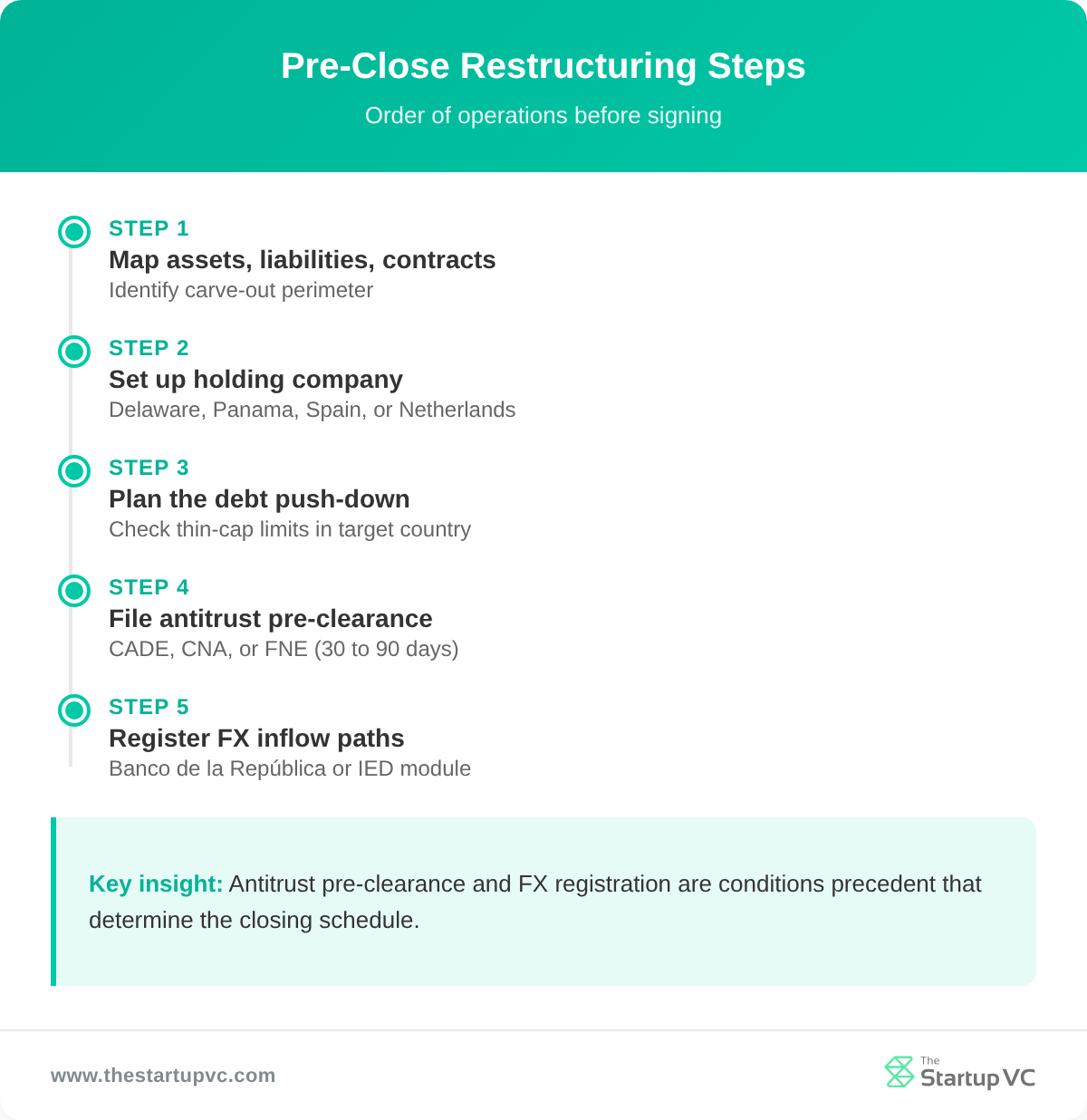

What Pre-Close Restructuring Steps Should Buyers Run Before Signing?

Pre-close restructuring steps include carving out non-core assets, pushing down acquisition debt, registering the holding company, and clearing antitrust filings. These steps are often conditions precedent to closing.

Mid-market deals in Latin America run 45 to 90 days of due diligence before signing. The deal size band is USD 50 million to USD 500 million. Total transactions take 6 to 12 months from kickoff to closing. Antitrust review adds another 30 to 90 days. Buyers who plan structure early avoid last-minute scrambles.

Run these steps in order:

- Map assets, liabilities, and contracts. Identify which target assets, employees, and contracts come over, especially in carve-outs where the unit is tangled with the parent.

- Set up the holding company. Form the Delaware, Panama, Spanish, or Dutch entity before signing so it is the named buyer in the SPA.

- Plan the debt push-down. Decide where acquisition debt sits, balancing interest deductibility against thin-capitalization limits in the target country.

- File antitrust pre-clearances. Submit to CADE, CNA, or FNE in parallel with diligence to avoid blowing the closing schedule.

- Register FX inflow paths. Pre-clear the capital injection route with Banco de la República in Colombia or the Central Bank’s IED module in Brazil.

- Run a tax-neutrality check. Confirm the chosen structure does not trigger immediate capital gains or transfer taxes inside the target country.

Brazil deserves extra care. Pre-closing reorganizations must factor successor liability for tax, labor, consumer, and environmental claims under the target’s pre-deal operations. A spin-off done badly can leave the buyer liable for issues it thought were carved out.

To plan how acquisition debt fits into the overall structure, see our guide on financing an acquisition in Latin America.

What Questions Do Buyers Ask Most Often About Cross-Border Acquisition Structure in Latin America?

How long does a cross-border acquisition take in Latin America?

A cross-border acquisition takes 6 to 12 months from kickoff to closing in Latin America. Mid-market deals run 45 to 90 days of due diligence, plus 30 to 90 days for antitrust review.

Which holding jurisdiction is best for buying a Brazilian target?

Spain or the Netherlands work best for buying Brazilian targets because both have favorable treaties and substance options. Spain’s treaty network is the broadest across the region.

What withholding tax applies to dividends from Mexico to a US parent?

Dividends from Mexico to a US parent qualify for a full withholding exemption. The parent must own 80% or more of the Mexican subsidiary. This sits under the US-Mexico tax treaty.

Do I need to register foreign investment in Colombia?

Yes, you must register foreign investment in Colombia with Banco de la República using Form F4 or F5. Without registration, you cannot repatriate capital, dividends, or sale proceeds.

How much does a typical cross-border LatAm acquisition cost in legal and tax fees?

A typical mid-market cross-border LatAm acquisition runs USD 500,000 to USD 2 million in fees. This covers combined legal, tax, and antitrust work. Brazilian deals sit at the higher end due to successor liability diligence.

What is the biggest mistake foreign buyers make on LatAm deals?

The biggest mistake foreign buyers make is choosing a holding jurisdiction with no treaty access to the target country. This locks in higher withholding tax on every dividend, royalty, and interest payment.

Ready to Structure Your Latin American Acquisition?

The Startup VC is Craig Dempsey’s family office and company builder. Portfolio companies operate across 17 Latin American markets. We help foreign buyers structure acquisition vehicles, pick holding jurisdictions, register FX inflows, and clear antitrust filings before signing. Our team brings hands-on experience from Biz Latin Hub, GGI, and MTP across the region. Contact us today to plan your next Latin American deal.