Latin America inbound M&A hit USD 40.6 billion across 600 deals in 2025, as buyers blended cash, seller notes, and cross-border debt.

Buyers fund Latin American acquisitions with five tools. These are cash, seller notes at 6% to 10% interest, earnouts worth 10% to 31% of price, mezzanine debt, and US-dollar SPV financing.

The Startup VC structures and backs acquisitions across Latin America as a family office and company builder. Our portfolio company Biz Latin Hub operates in 17 countries, giving us direct experience with local lenders and deal terms. Below, you will find each financing tool, typical terms, and how to combine them.

What Are the Main Ways to Finance an Acquisition in Latin America?

The main ways to finance a Latin American acquisition are cash, seller notes, earnouts, mezzanine debt, and bank debt. Most buyers combine two or three. High regional interest rates push many toward private debt and US-dollar structures.

Latin America inbound M&A reached USD 40.6 billion across 600 deals in 2025. That marks a 45% jump from 2024, driven by US, Spanish, and Chinese acquirers. Over 40 active private debt investors now operate across Mexico, Brazil, Colombia, Chile, and Argentina.

Each tool fits a different part of the deal. Here is how the five main options compare:

| Financing Tool | Typical Cost | Best For |

|---|---|---|

| Cash | None (your capital) | Speed and seller certainty |

| Seller note | 6% to 10% interest | Bridging part of the price |

| Earnout | 10% to 31% of price | Closing valuation gaps |

| Mezzanine debt | 10% to 14% return | Filling the senior debt gap |

| US-dollar SPV debt | Market rate, cheaper than local | Cross-border deals |

Buyers rarely fund a deal with one tool alone. A common structure pairs a cash down payment with a seller note and an earnout. Larger deals add mezzanine debt or bank debt on top. The right mix depends on deal size, target cash flow, and currency exposure.

You can read our full guide on how to buy a company in Latin America for the broader acquisition process. This article focuses only on the financing layer.

How Do Seller Notes Work in Latin American Acquisitions?

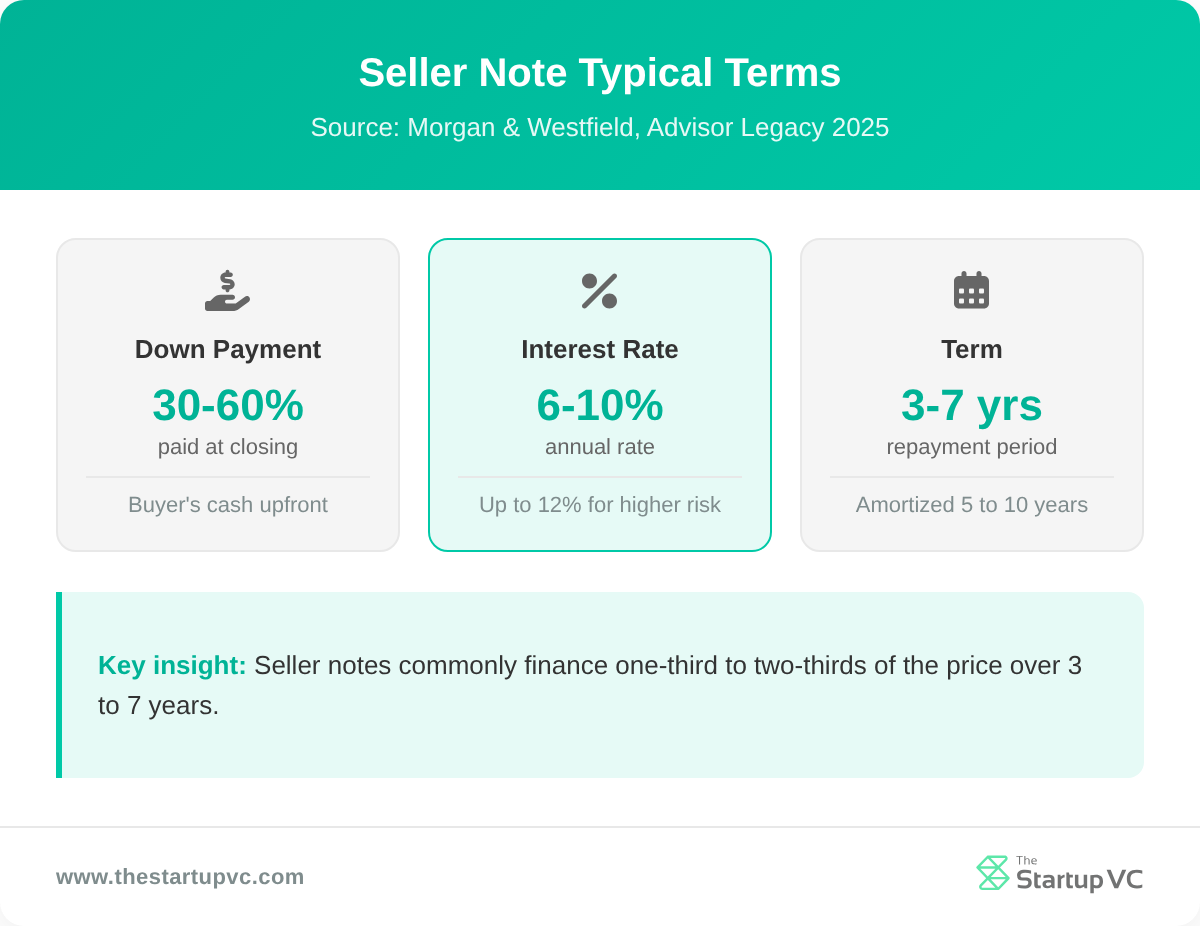

Seller notes work by letting the seller finance part of the price through a deferred payment. The buyer pays a down payment at closing. The seller then receives the rest over several years, plus interest.

Seller notes usually cover one-third to two-thirds of the sale price. Buyers typically put 30% to 60% down at closing. Interest rates run from 6% to 10%, sometimes up to 12% for higher-risk deals. Repayment terms last 3 to 7 years.

A promissory note sets the core terms. It defines the interest rate, payment schedule, and maturity date. It also covers default consequences and any balloon payment. Sellers often secure the note against business assets to protect their position.

Sellers in Latin America often accept notes for three reasons:

- Faster close. Deferred payment keeps the deal moving when bank debt is slow or costly.

- Higher price. Buyers pay more when sellers carry part of the risk.

- Tax timing. Spreading payments over years can ease the seller’s tax burden.

A seller note also signals seller confidence. A seller who finances part of the price believes the business will keep performing. That trust matters to other lenders and lowers buyer risk.

How Does an Earnout Structure Reduce Acquisition Risk?

An earnout reduces risk by tying part of the price to the target’s future performance. The seller earns extra payments only if the business hits agreed financial targets. This protects the buyer if results fall short.

Earnouts usually make up 10% to 25% of the purchase price. The 2024 median outside life sciences reached 31% of closing payments. The median earnout period is 24 months, though some run one to five years. About 22% of private deals in 2024 included an earnout.

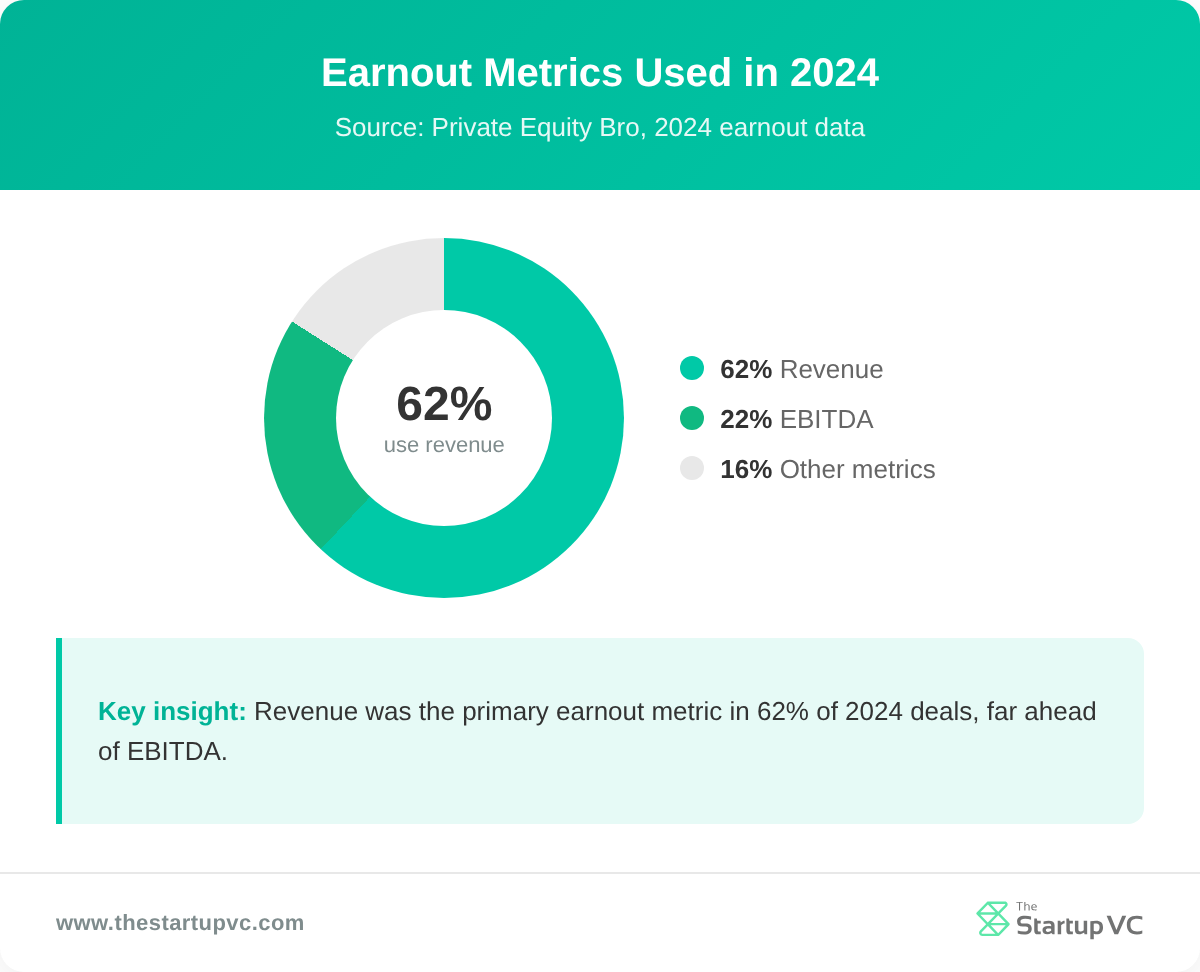

Most earnouts measure revenue or profit. The metric choice shapes how the seller behaves after closing:

| Metric | Share of 2024 Earnouts | What It Rewards |

|---|---|---|

| Revenue | 62% | Top-line growth |

| EBITDA | 22% | Profitable growth |

Earnouts bridge the gap when buyer and seller disagree on price. The seller bets on strong future results. The buyer pays the full price only if those results arrive. Both sides share the risk fairly.

Earnouts also cause disputes if terms are vague. You must define the metric and accounting method in writing. Spell out how revenue or EBITDA gets measured. Clear terms prevent fights over the payout later.

How Can Mezzanine and Bank Debt Fund a LatAm Acquisition?

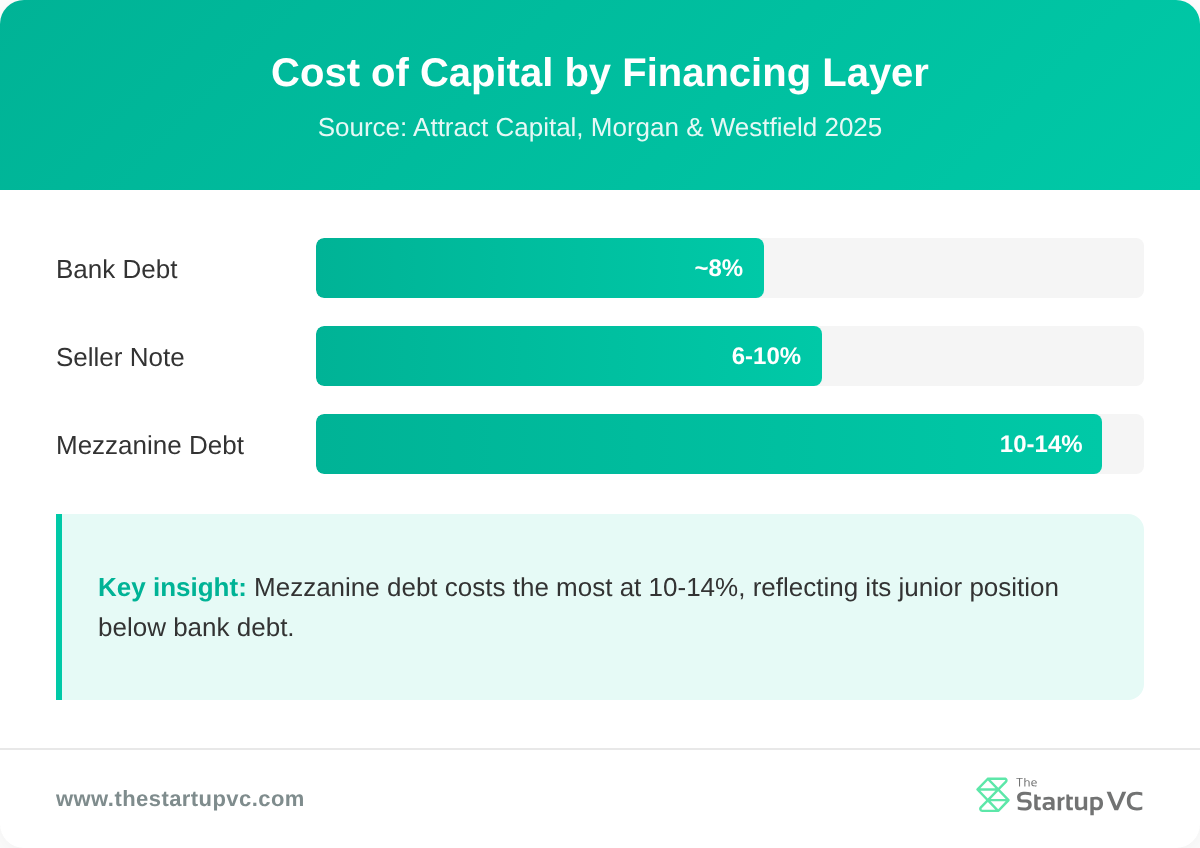

Mezzanine and bank debt fund a LatAm acquisition by adding leverage on top of your cash. Bank debt is the cheapest layer. Mezzanine debt fills the gap when bank lending runs out.

Local banks in Latin America cap how much debt a business can take on. High regional interest rates also make bank loans expensive. These limits push many buyers toward private debt and mezzanine financing. Over 40 private debt investors now serve the region.

Mezzanine debt sits between senior bank debt and equity. It can take the form of unsecured debt or preferred stock. Lenders often get an option to convert into equity. Mezzanine loans usually yield 10% to 14% for the lender.

Here is how the two debt layers compare:

| Feature | Bank Debt | Mezzanine Debt |

|---|---|---|

| Cost | Lower, market rate | 10% to 14% |

| Security | Senior, secured | Junior, often unsecured |

| Availability in LatAm | Limited, capped | Growing fast |

| Equity option | No | Often yes |

Mezzanine debt suits buyouts where bank debt is too small. It fills the space between cheap senior debt and your own equity. This lets you fund a larger deal without giving up control. The higher cost reflects the lender’s junior position.

Why Do Buyers Use US-Domiciled SPVs and Rollover Equity?

Buyers use US-domiciled SPVs and rollover equity to lower their cost of capital and keep sellers invested. An SPV taps cheaper US-dollar debt. Rollover equity keeps the seller’s skin in the game.

A US-domiciled SPV is a holding company that owns the target. Lenders route leveraged finance through it. The SPV gives lenders a familiar legal framework and access to cheaper dollar capital. In cross-border deals, the loan agreement often falls under New York law. Local law governs the closing in the target country.

For the full vehicle and tax treaty analysis, see our guide on how to structure a cross-border acquisition in Latin America. The SPV choice affects both financing cost and tax.

Rollover equity is the part of the seller’s stake not cashed out at closing. The seller reinvests it into the new entity. In private equity deals, sellers commonly roll 10% to 40% of their proceeds. Many deals land in the 20% to 40% range.

Rollover equity helps buyers in three ways:

- Lower cash need. Less money changes hands at closing.

- Aligned seller. The seller stays invested in future results.

- Strong signal. A rolling seller shows real confidence in the business.

Both tools shift risk and cost in the buyer’s favor. The SPV cuts borrowing cost. The rollover keeps the seller working toward the same goal. Together they make cross-border deals cheaper and safer.

What Questions Do Buyers Ask Most Often About Acquisition Financing in Latin America?

How much of the price can a seller note cover?

A seller note can cover one-third to two-thirds of the sale price. Buyers usually put 30% to 60% down at closing. Interest runs 6% to 10% over a 3 to 7 year term.

How long does an earnout last?

An earnout lasts a median of 24 months for most deals. Some run from one to five years. The seller earns extra pay only if the business hits its targets.

Why is bank debt limited in Latin America?

Bank debt is limited because local banks cap total borrowing and charge high interest. High regional rates make loans costly. Buyers often add mezzanine debt or private credit to fill the gap.

How does a US-domiciled SPV cut costs?

A US-domiciled SPV cuts costs by accessing cheaper US-dollar debt. It gives lenders a familiar New York law framework. This often beats borrowing in local currency at high local rates.

How much equity do sellers usually roll over?

Sellers usually roll over 10% to 40% of their proceeds. Many private equity deals land in the 20% to 40% range. The rollover keeps the seller invested after closing.

What does mezzanine debt cost?

Mezzanine debt costs 10% to 14% in lender return. It sits between bank debt and equity. Lenders often want an option to convert their loan into equity.

Ready to Finance Your Next Acquisition in Latin America?

The Startup VC structures, backs, and guides acquisitions across Latin America. We are Craig Dempsey’s family office and company builder, with deep regional experience through Biz Latin Hub in 17 countries. We help buyers blend cash, seller notes, earnouts, and cross-border debt into deals that close. Explore our investment focus to see the ventures we back. Contact us today to structure your next acquisition.