M&A in Brazil hit BRL 187.8 billion across 1,142 deals through August 2025, the largest deal market in Latin America.

Foreign buyers now drive 41% of Brazil’s deal value. Most acquisitions close in three to six months. CADE clears about 95% of filings, and deals over BRL 750 million need its antitrust approval before closing.

The Startup VC has operated portfolio companies like Biz Latin Hub across 17 Latin American countries since 2014. Craig Dempsey’s family office builds and buys service businesses with hands-on support. This guide covers buying, selling, deal structures, CADE review, and taxes for M&A in Brazil.

Why Is Brazil the Top M&A Market in Latin America?

Brazil is Latin America’s top M&A market because it holds about 60% of regional deal value. The country also drove 55% of the region’s deal volume in 2025. No rival market comes close on either measure.

Four forces keep Brazil ahead of its neighbors:

- Largest economy. Brazil holds roughly 60% of Latin America’s M&A deal value.

- Strong rebound. It logged 1,142 deals worth BRL 187.8 billion through August 2025.

- Foreign demand. Overseas buyers reached 41% of 2025 deal value, up from 31%.

- Deep sectors. Energy alone logged a record 72 reported deals in 2024.

That rebound marked a 33% rise over the same period in 2024. Internet, software, and IT services led by deal count. Foreign buyers drove much of the momentum. Their share by deal count rose to 34% in 2025, up from 26%. The United States is the leading source of cross-border deals.

Three of Brazil’s largest 2025 deals show where capital flows:

| Deal | Acquirer | Sector |

|---|---|---|

| Mantiqueira transmission line | State Grid (China) | Energy |

| Motiva 20-airport platform | ASUR (Mexico) | Infrastructure |

| BASF Brazil coatings unit | Sherwin-Williams (US) | Industrial |

Energy, infrastructure, and financial services anchor most large Brazilian M&A. The Netherlands, France, Argentina, and Spain also send active buyers. Our investment focus page shows the sectors and stages we back across the region.

How Do You Buy a Company in Brazil?

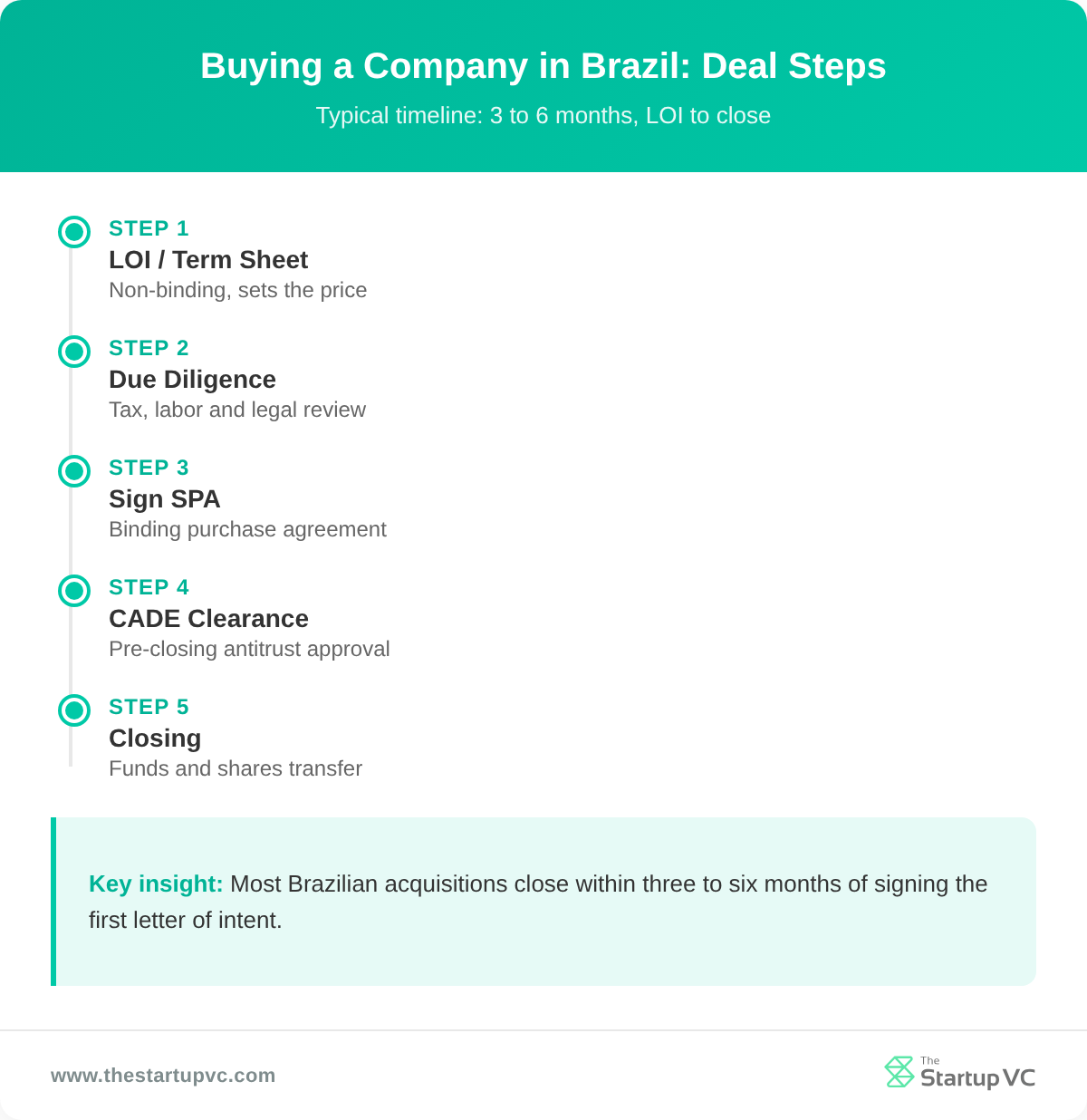

You can buy a company in Brazil by following a clear deal sequence over three to six months. The process moves from a letter of intent to due diligence and a signed contract. Larger or more complex targets take longer.

Most Brazilian acquisitions follow five steps:

- Letter of intent. Sign a non-binding LOI, MOU, or term sheet to set price and terms.

- Due diligence. Review financial, tax, labor, and legal records before signing.

- Share purchase agreement. Negotiate a binding SPA with indemnities and warranties.

- Regulatory clearance. File with CADE and register foreign capital where required.

- Closing. Transfer shares or quotas and pay the agreed price.

Due diligence is the heart of the process. Brazilian courts read successor liability broadly. Hidden labor and tax exposures are common. Buyers manage these risks with indemnity clauses and warranties rather than price cuts. For a regional view, read our guide on how to buy a company in Latin America.

What Deal Structures Are Common in Brazilian M&A?

The most common deal structures in Brazilian M&A are share deals and asset deals. Share and quota purchases dominate the market. They are simpler and more tax-efficient than asset deals.

Ownership form depends on the company type. A Sociedade Limitada (Ltda) holds ownership as quotas. Transferring quotas requires amending the Articles of Association. It also needs consent from partners holding at least 75% of capital. A Sociedade Anônima (S.A.) holds shares in a register book. An S.A. can issue multiple share classes with different rights.

| Feature | Share or Quota Deal | Asset Deal |

|---|---|---|

| What transfers | Equity in the company | Selected assets and contracts |

| Liabilities | Buyer assumes company history | Buyer picks assets, but CTN 133 applies |

| Indirect taxes | Avoids ITBI, ICMS, and ISS | Can trigger ITBI, ICMS, and ISS |

| Speed | Faster, less paperwork | Slower, asset by asset |

Asset deals stay rare for one main reason. Under Article 133 of the National Tax Code, the buyer inherits the seller’s taxes. A buyer who continues the business is fully liable for pre-closing taxes. That makes share deals the safer default for most buyers.

What Rules Apply to Foreign Buyers in Brazil?

The main rules for foreign buyers are capital registration and sector ownership limits. Brazil welcomes foreign capital in most industries. A few sectors still cap how much foreigners can own.

Foreign direct investment must be registered with the Central Bank of Brazil (BACEN). Registration uses the SCE-IED system under Lei 14.286/2021. Transfers of USD 100,000 or more need an SCE-IED code at the time of the exchange.

Some sectors limit foreign ownership:

- Rural land. Foreign owners cannot exceed 25% of any municipality’s area.

- Media. Journalism and open-TV firms cap foreign capital at 30%.

- Maritime transport. Foreign investors may hold up to 49% of shares.

- Financial institutions. Any rise in foreign stakes needs Central Bank clearance.

Aviation rules changed recently. Lei 13.842/2019 now allows 100% foreign capital in domestic airlines. The old rule had required 80% Brazilian voting capital.

How Do You Sell a Business in Brazil?

You can sell a business in Brazil by cleaning up the company before buyers arrive. Brazilian deals depend heavily on seller indemnities. Clean records raise your price and speed up the sale.

Sellers should prepare these items first:

- Tax certificates. Reconcile federal, state, and municipal filings and clear debts.

- Labor clearance. Obtain a clean Labor Court certificate (CNDT).

- Litigation review. Cover the last five years of tax and labor disputes.

- Clean financials. Produce audited statements buyers and banks can trust.

Most owners hire a local investment bank to run the sale. BTG Pactual ranked as Latin America’s top M&A advisory house in 2025. It handled US$15 billion in deal volume, including the BRF-Marfrig merger. Itaú BBA led Brazilian equities with 56% market share. These banks run competitive auctions that lift final prices.

For the full owner’s playbook, see our guide on how to sell a company in Latin America.

How Are Brazilian Companies Valued for Sale?

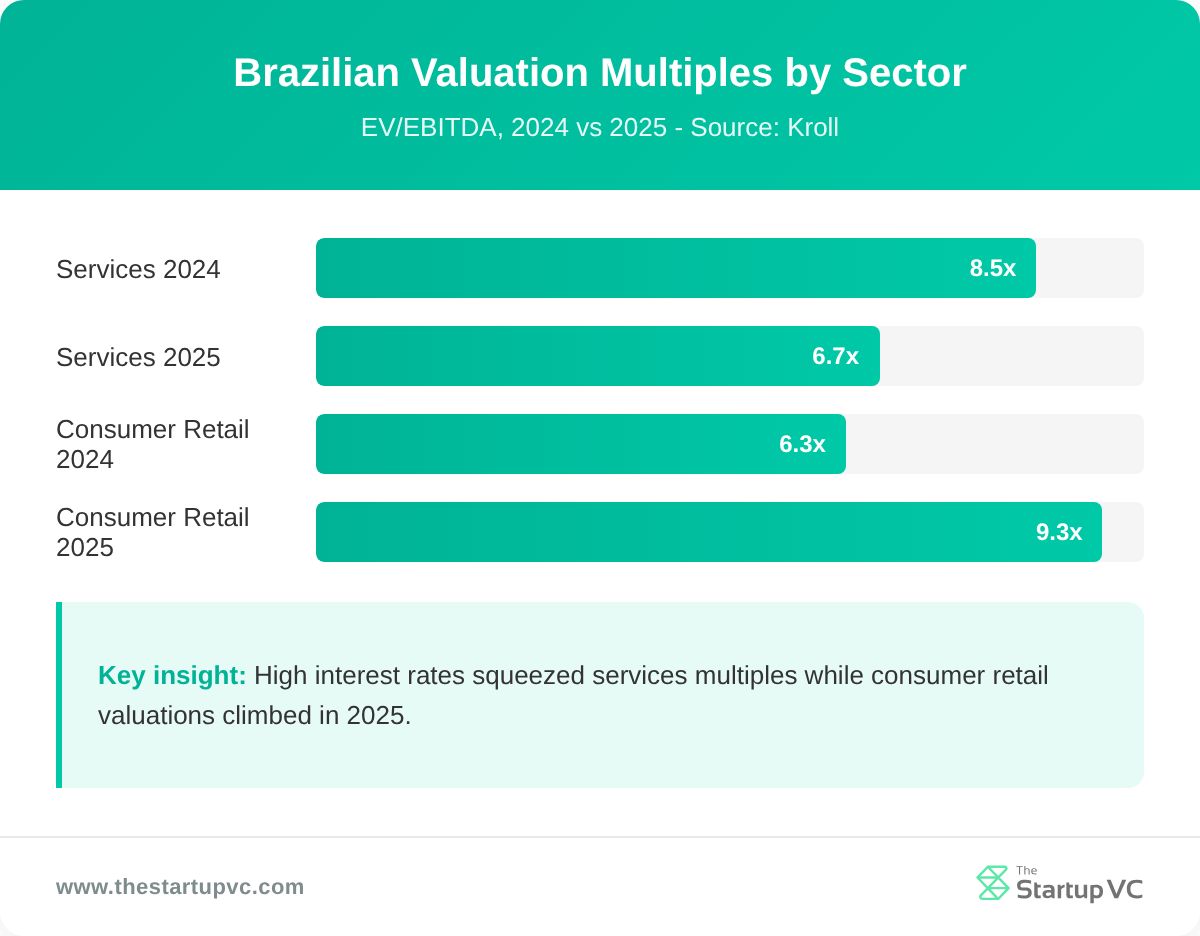

Brazilian companies are valued by applying EBITDA multiples and discounted cash flow. Most Brazilian and Latin American targets trade at 4x to 12x EV/EBITDA. The exact multiple depends on sector, growth, and revenue quality.

High interest rates weigh on these numbers. Brazil’s Selic rate rose from 12.25% in late 2024 to about 15% by mid-2025. Higher rates lift discount rates and compress the multiples buyers will pay.

Recent sector multiples show the spread:

| Sector | EV/EBITDA (2025) | Trend vs end-2024 |

|---|---|---|

| Services | ~6.7x | Down from 8.5x |

| Consumer and retail | ~9.3x | Up from 6.3x |

Recurring revenue commands the top of the range. Multi-country firms with stable contracts attract the best offers. You can compare methods in our guide on how to value a company in Latin America.

How Do Owners Exit in Brazil Today?

Owners exit in Brazil today mostly by selling to strategic or private equity buyers. The B3 stock exchange IPO window has stayed nearly shut since 2021. Listings fell from 46 IPOs in 2021 to about 5 small deals in 2024.

Brazilian owners now exit through three main routes:

- Trade sales. Sell to a strategic buyer or PE fund, the most common exit.

- Take-privates. Delist a public company, as with the Cielo delisting in August 2024.

- Block trades. Sell large share blocks on the B3 exchange.

High rates also push deals toward creative terms. Earn-outs and vendor loans help bridge price gaps. Buyers usually hold 5% to 15% of the price in escrow. That holdback lasts about 12 to 18 months to cover claims.

How Does CADE Review Mergers in Brazil?

CADE reviews mergers in Brazil by checking whether a deal harms competition before it closes. CADE is the Conselho Administrativo de Defesa Econômica, Brazil’s antitrust authority. Filing is mandatory and happens before closing under a suspensory regime. Closing too early counts as gun jumping and can void the deal.

What Are CADE’s Notification Thresholds?

CADE’s notification thresholds are two revenue tests that both must be met. A filing is mandatory only when one group earns at least BRL 750 million in Brazil. The other party group must earn at least BRL 75 million. Both figures cover annual gross revenue in the year before the deal.

Two cost items apply to every filing:

- Filing fee. A flat BRL 85,000 taxa processual, due before review and non-refundable.

- Gun-jumping fines. Penalties run from BRL 60,000 to BRL 60 million for early closing.

CADE has enforced these fines in practice. It fined OGX BRL 3 million for closing a Petrobras asset deal too early.

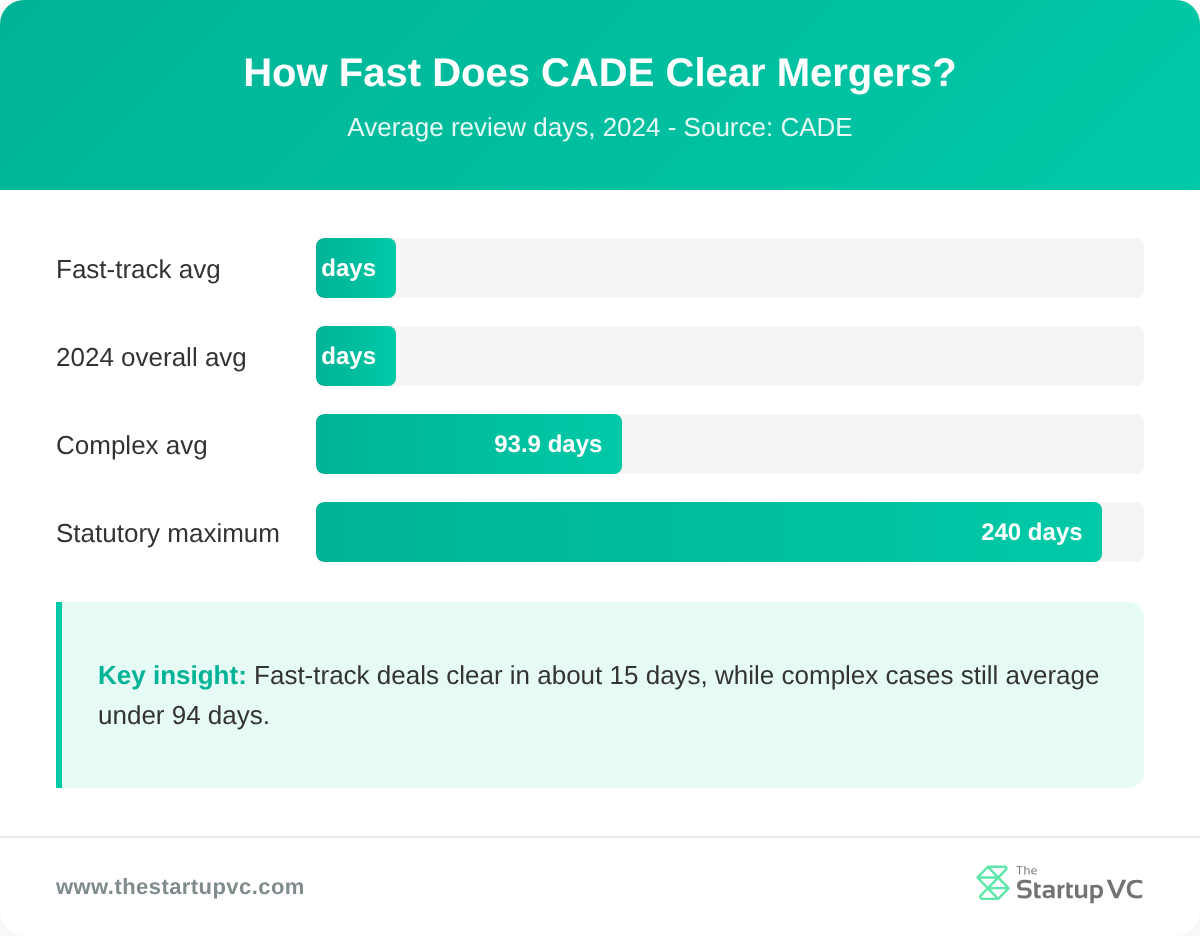

How Long Does CADE Review Take?

CADE review takes from about 15 days to 330 days, depending on complexity. Simple deals move on a fast track. Complex deals follow the ordinary procedure with a longer statutory clock.

| Track | When It Applies | Statutory Limit | 2024 Average |

|---|---|---|---|

| Fast-track (sumário) | Low overlap or simple links | 30 days | 15.1 days |

| Ordinary | Complex or high-overlap deals | 240 days plus 90 | 93.9 days |

Most deals qualify for the fast track. CADE clears low-complexity cases in about two weeks. Complex reviews can extend to 330 days when CADE needs more time. In 2024 about 95% of its 712 filings cleared with no restrictions.

CADE still conditions deals that threaten competition. On 10 December 2025, it conditionally approved the Petz-Cobasi pet-retail merger. The parties had to divest 26 stores in São Paulo.

What Taxes Apply When Buying or Selling a Company in Brazil?

The main taxes in Brazilian M&A are capital gains for sellers and transfer taxes on assets. The buyer and seller face different bills. Deal structure shapes the total tax cost. A new consumption tax reform will also affect future deals.

How Are Sellers Taxed on a Brazilian Sale?

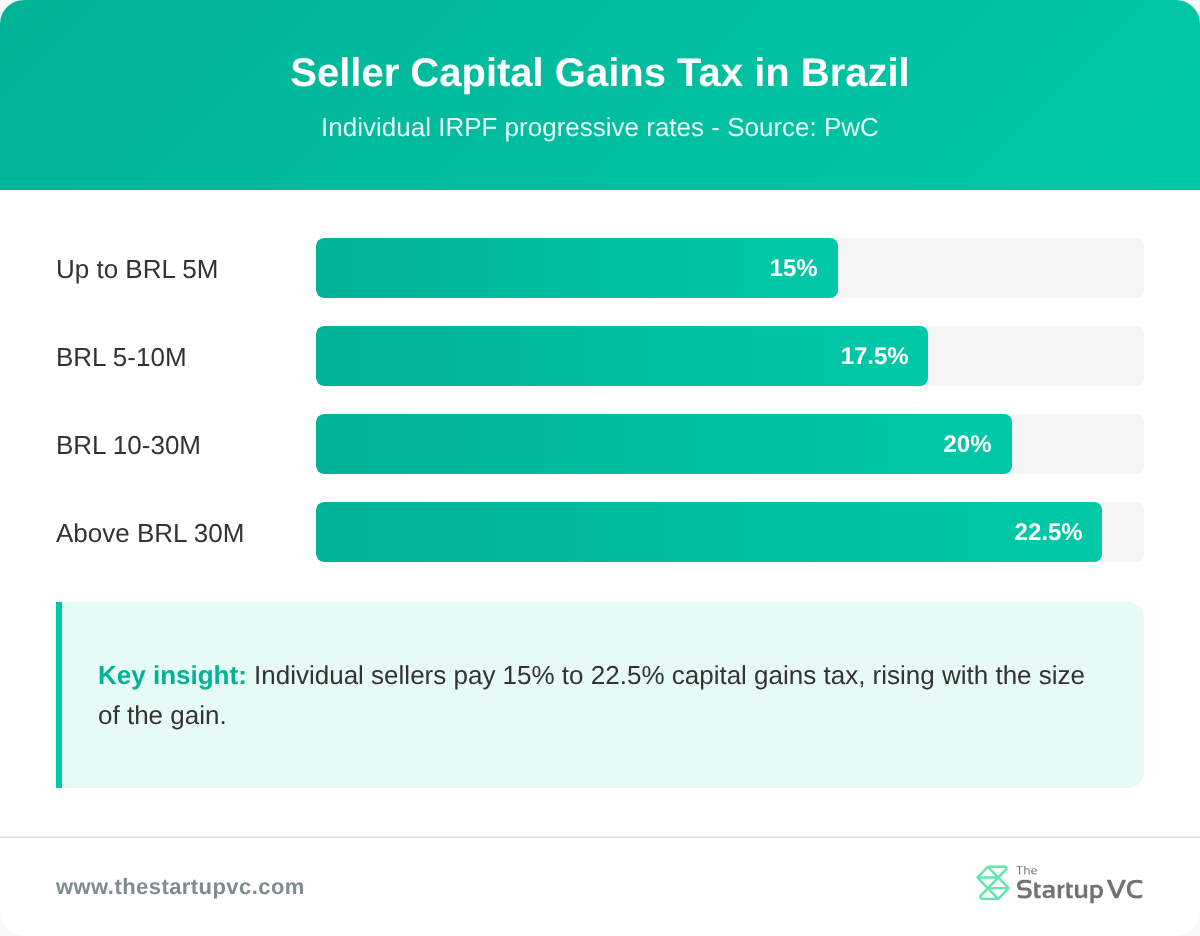

Sellers are taxed on the capital gain from the sale, at progressive rates. Individuals pay 15% on gains up to BRL 5 million. The rate climbs to 22.5% on gains above BRL 30 million. Corporate sellers instead pay about 34% as ordinary income.

Individual seller capital gains tax follows four brackets:

| Gain (BRL) | Rate |

|---|---|

| Up to 5 million | 15% |

| 5 to 10 million | 17.5% |

| 10 to 30 million | 20% |

| Above 30 million | 22.5% |

Foreign sellers face special rules. They pay the same 15% starting rate, withheld by the Brazilian buyer. A flat 25% applies if the seller sits in a tax haven.

What Tax Benefits Can Buyers Claim?

Buyers can claim goodwill amortization and lower transfer taxes on share deals. The biggest benefit is ágio, or goodwill based on expected future profits. After merging with the target, the buyer deducts ágio against income tax. The deduction runs at up to 1/60 per month, over at least five years.

To claim ágio, buyers must follow strict steps. An independent expert prepares a purchase price allocation report. The buyer files it with the Receita Federal within 13 months of the deal.

Structure choice also drives transfer taxes:

- Share deals. Avoid ITBI and most indirect taxes like ICMS and ISS.

- Asset deals. Trigger ITBI of about 2% to 3% on real estate.

Brazil’s tax reform will reshape these costs. Laws EC 132/2023 and LC 214/2025 replace five taxes with a dual VAT. The new CBS and IBS phase in through 2033, changing how buyers price deals.

What Questions Do Founders Ask Most Often About M&A in Brazil?

How Long Does an M&A Deal Take in Brazil?

An M&A deal in Brazil takes about three to six months from LOI to close. Complex deals run longer. CADE clearance adds 15 days on the fast track. Ordinary CADE reviews can stretch the timeline to several months.

Can Foreigners Buy 100% of a Brazilian Company?

Yes, foreigners can buy 100% of most Brazilian companies. A few sectors cap foreign ownership, such as media and maritime transport. Buyers must register foreign capital with the Central Bank of Brazil. Rural land and border zones carry extra limits.

Do You Need CADE Approval for Every Deal?

No. You need CADE approval only when both revenue thresholds are met. One group must earn at least BRL 750 million in Brazil. The other must earn at least BRL 75 million. Smaller deals skip the filing.

How Much Does It Cost to File with CADE?

Filing with CADE costs a flat BRL 85,000 fee. The fee is due before review starts. It is non-refundable, even if you withdraw the deal. Closing early can add fines up to BRL 60 million.

Should Buyers Choose a Share Deal or an Asset Deal?

Buyers should usually choose a share deal in Brazil. Share deals avoid transfer taxes like ITBI, ICMS, and ISS. They also involve less paperwork. Asset deals make sense when buyers want to leave liabilities behind.

What Is the Biggest Risk When Buying in Brazil?

The biggest risk is hidden labor and tax liabilities. Brazilian courts apply successor liability broadly. Buyers can inherit the seller’s past debts after closing. Strong due diligence and indemnity clauses reduce this risk.

Ready to Buy or Sell a Company in Brazil?

Buying or selling a company in Brazil rewards careful planning and local insight. The Startup VC is Craig Dempsey’s family office and company builder. We create, back, and guide ventures across Latin America. Our team has run portfolio companies like Biz Latin Hub in 17 countries. We bring hands-on deal, tax, and operational support to every transaction. Ready to move on a Brazilian deal? Contact us today to plan your next step.