Latin American services companies trade at a median 6.7x EV/EBITDA in 2025, with recurring-revenue firms reaching 8x to 12x.

Business valuation in Latin America combines three methods: DCF, market multiples, and comparable transactions. Buyers adjust each result for country risk premia near 3.5%, currency swings, and inflation. Recurring revenue and multi-country scale push values well above the regional median.

The Startup VC builds and backs service ventures across Latin America, including Biz Latin Hub in 17 countries. This guide covers each valuation method, sector EBITDA multiples, DCF construction, and the country risk and FX adjustments that shape every LatAm deal.

What Is Business Valuation in Latin America?

Business valuation in Latin America is the process of estimating what a company is worth before a sale or investment. It combines financial data with regional risk factors that buyers price in. The result guides both sell-side and buy-side negotiations.

A services company in Latin America trades at a median 6.7x EV/EBITDA in 2025. That figure fell from 8.5x at the end of 2024. The number you reach depends on your business model and risk profile.

Five factors drive the valuation of a services company in Latin America:

- Recurring revenue share. Predictable income raises the multiple buyers will pay.

- EBITDA margin. Higher margins signal a healthier, more efficient business.

- Customer concentration. Relying on a few clients lowers value.

- Growth rate. Faster growth supports a higher price.

- Geographic scale. Multi-country operations command a premium.

The region remains active for dealmaking. Latin America recorded 2,650 M&A deals worth US$96 billion in 2025. That volume rose 13% from 2024. Strong deal flow gives sellers more comparable benchmarks to anchor a price.

If you want to raise your number before a sale, see our guide on how to increase the valuation of a services company in Latin America.

What Are the Main Methods to Value a Company in Latin America?

The main methods to value a company in Latin America are DCF, market multiples, and comparable transactions. Each method suits a different business profile and data set. Most advisors run two or three methods and triangulate the results.

Five business valuation methods appear most often in practice:

| Method | Best For | How It Works |

|---|---|---|

| DCF | Mature firms with predictable cash flows | Discounts future cash flows to today |

| EBITDA multiples | Larger, professionally managed companies | Applies a sector multiple to EBITDA |

| Revenue-based | High-growth or recurring-revenue firms | Applies a multiple to annual revenue |

| SDE | Small, owner-operated businesses | Adjusts earnings for owner pay |

| Comparable transactions | Sectors with recent M&A deals | Uses prices paid in similar deals |

SDE fits smaller, owner-operated businesses. EBITDA multiples fit larger, professionally managed companies. DCF works best for mature businesses with predictable cash flows.

Comparable transactions use recent deal prices in the same sector and country. This method works well in Latin America because regional M&A data has grown. Buyers trust prices that real acquirers paid for similar firms. The connective thread runs from selling to buying, so both sides should know all three methods.

Each method answers a slightly different question. DCF asks what future cash is worth today. Multiples ask what the market pays for similar earnings now. Comparable transactions ask what buyers actually paid in real deals. Smart advisors weigh all three and explain any gap between them.

Method choice also depends on data quality. Public comparables are thin in many LatAm markets. Private deal data fills part of that gap. When clean financials exist, DCF gives the most defensible number. When they do not, multiples and recent transactions carry more weight.

Founders preparing an exit can read our companion guide on how to sell a company in Latin America. Acquirers should review how to buy a company in Latin America before bidding.

How Do You Build a DCF Valuation for a LatAm Company?

You build a DCF valuation for a LatAm company by projecting cash flows and discounting them with a risk-adjusted rate. A standard DCF needs two inputs: cash flow forecasts and a discount rate. Both inputs are harder to set in emerging markets.

How Do You Project Cash Flows?

You project cash flows by forecasting revenue, costs, and capital needs over five to ten years. Use realistic growth rates tied to the local market. Latin American growth is projected to slow to 1.8% in 2026 from 2.2% in 2025. Anchor your forecast to these macro trends, not to optimistic targets.

How Do You Set the Discount Rate?

You set the discount rate by building a WACC and adding emerging-market premiums. Add industry and country risk premiums for volatile sectors or emerging markets. This raises the discount rate and lowers the present value of future cash flows.

Many advisors model cash flows in US dollars to avoid local currency noise. You can convert a local-currency WACC to dollars with this formula:

> US$ WACC = (1 + Local WACC) x (1 + US$ inflation) / (1 + Local inflation) – 1Emerging market firms often carry lower debt than developed-market peers. Consider a dynamic WACC where leverage rises toward a developed-market level by the end of the forecast.

How Do You Calculate Terminal Value?

You calculate terminal value by capturing cash flows beyond the forecast window. Most models use a growth rate that matches long-run inflation. In high-inflation markets, a dollar-based model keeps that rate realistic. A too-high terminal growth rate can inflate the result by millions.

Terminal value often makes up most of a DCF result. That makes the discount rate and growth assumption critical. Small changes in either input move the final number a lot. Always test a range of rates before you commit to one valuation.

What EBITDA Multiples Apply to Latin American Companies?

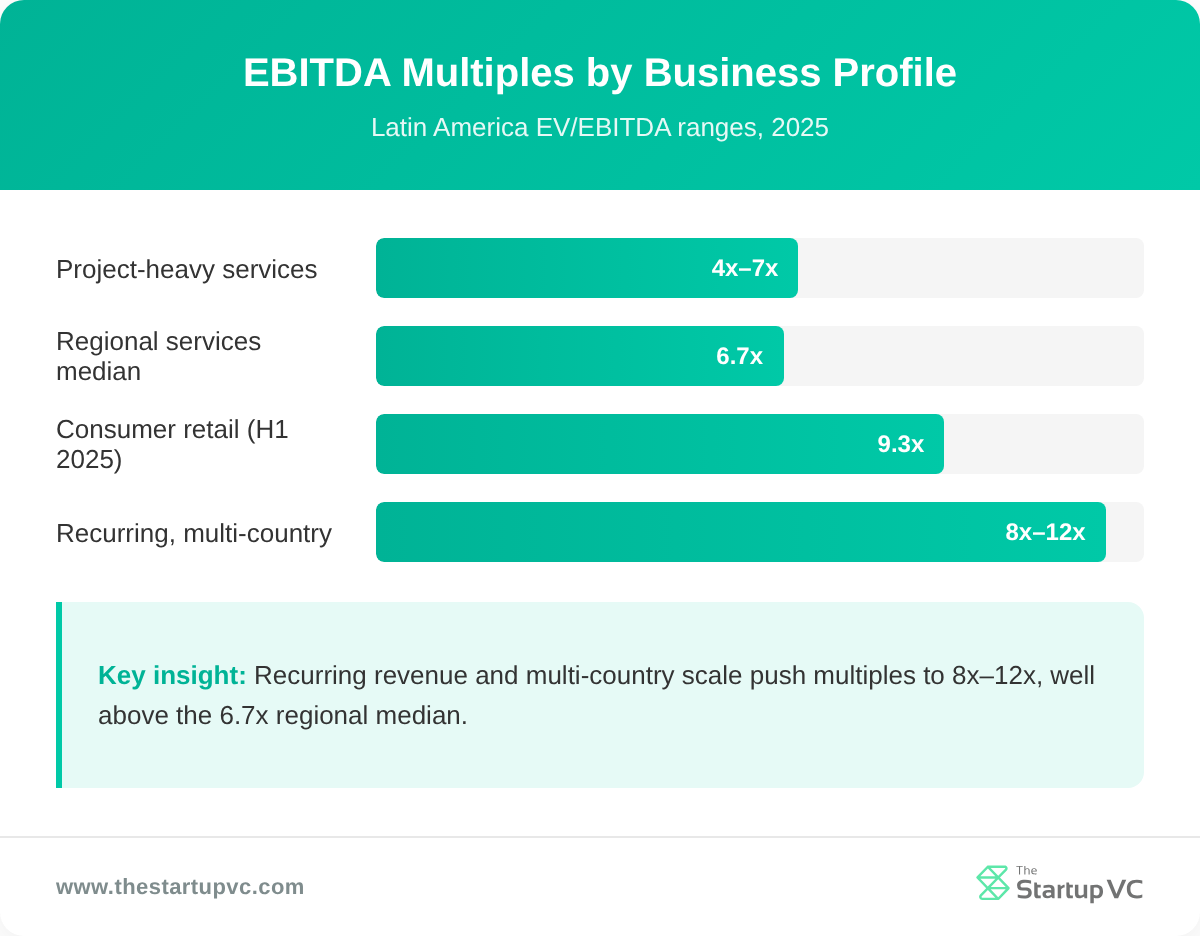

EBITDA multiples for Latin American companies range from about 4x to 12x, depending on the sector and business model. The services median is 6.7x EV/EBITDA in 2025. That fell from 8.5x at the end of 2024. Your multiple moves up or down from this baseline based on quality signals.

Business model shapes the multiple more than any other factor. The table below shows typical ranges across common services profiles.

| Business Profile | Typical EV/EBITDA |

|---|---|

| Project-heavy services | 4x to 7x |

| Regional services median | 6.7x |

| Recurring revenue, multi-country | 8x to 12x |

| Consumer distribution/retail (H1 2025) | 9.3x |

Recurring revenue is the single biggest lever. It can lift valuation by 1.5x to 3x on the EBITDA multiple. Firms with 70% or more recurring revenue trade at 7x to 12x ARR. Multi-country platforms with recurring revenue can reach 10x to 12x.

Buyers reward predictable income above all else. In one survey, 66% of investment bankers said recurring revenue will be the most important characteristic to acquirers in 2026. A B2B services firm that shifts from project work to contracts can reprice its entire business.

Multiples also move with the cycle. The services median fell from 8.5x to 6.7x in just six months. By contrast, consumer distribution and retail rose to 9.3x in H1 2025 from 6.3x at the end of 2024. Sector timing can matter as much as company quality. Track current data before you anchor on a number.

Apply multiples with care across the region. A multiple drawn from a Chilean deal does not transfer cleanly to an Argentine firm. Country risk, currency, and inflation all reshape the fair multiple. Use local comparables where you can find them.

How Do Country Risk and FX Adjustments Affect LatAm Valuations?

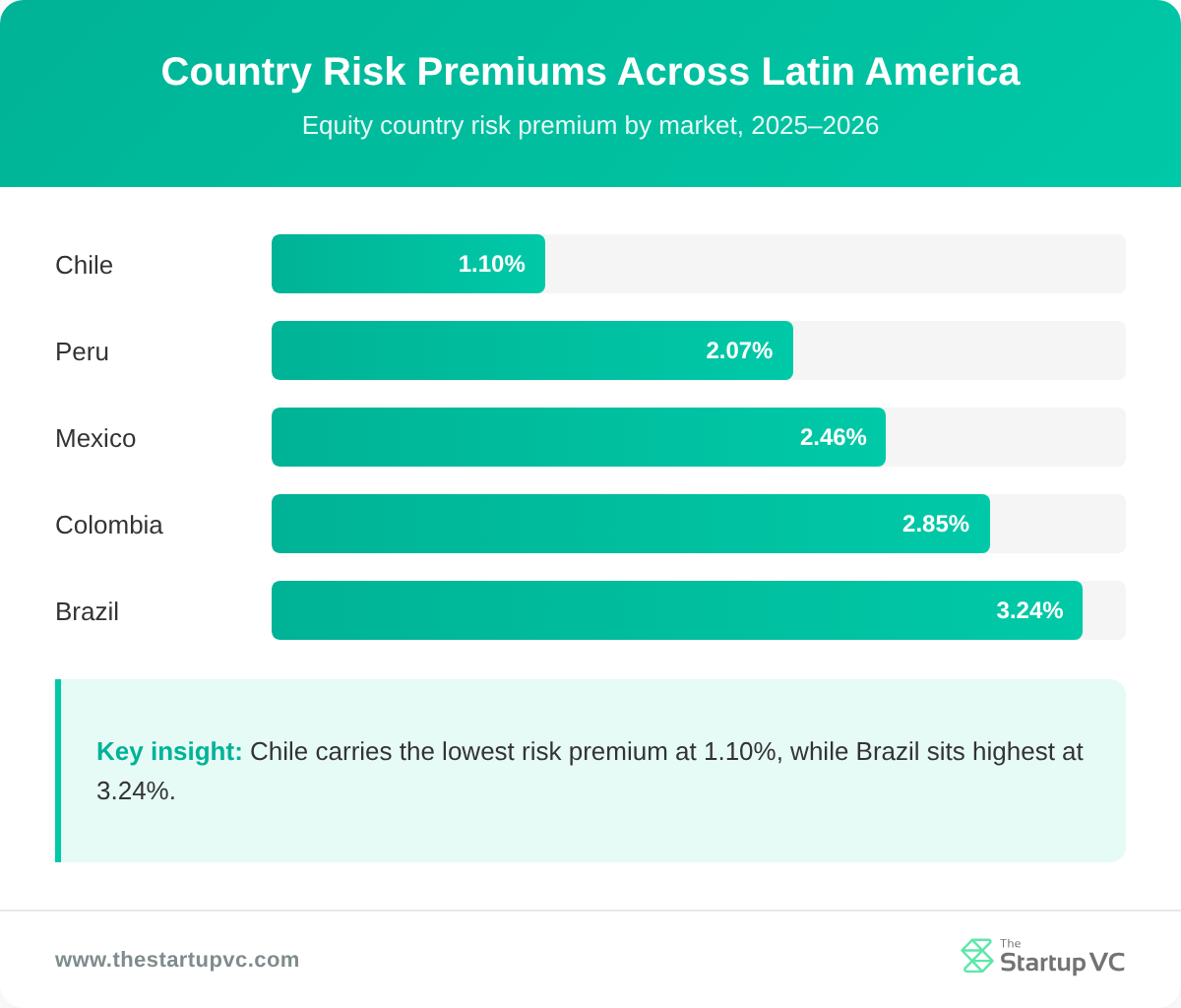

Country risk and FX adjustments lower LatAm valuations by raising the discount rate and shrinking dollar cash flows. Damodaran estimates the average Latin American country risk premium at roughly 3.5%. This premium gets added on top of a base cost of capital.

Country risk varies widely across the region. The table below shows recent equity country risk premiums by market.

| Country | Country Risk Premium |

|---|---|

| Chile | ~1.10% |

| Peru | ~2.07% |

| Mexico | ~2.46% |

| Colombia | ~2.85% |

| Brazil | ~3.24% |

Damodaran ties risk to where a company earns revenue, not where it is incorporated. A firm selling across several countries blends their premiums. This rule matters for regional platforms with mixed revenue sources.

How Do You Adjust for Currency and Inflation?

You adjust for currency and inflation by deriving forward FX rates from inflation differentials. Forward rates come from the spot FX rate and the inflation gap between two currencies. High inflation erodes local cash flows when converted to dollars.

Recent conditions show why this matters:

- Argentina. Inflation fell from a peak near 300% in April 2023 to about 40% in June 2025, yet the peso stays overvalued.

- Brazil. The Selic policy rate sits at 15%, which raises discount rates and pressures valuations.

- Regional growth. Slower growth of 1.8% in 2026 trims forward cash flow forecasts.

These adjustments explain why a LatAm firm often values below a US peer with identical financials. The gap reflects risk, not weaker operations.

Reforms can shrink that gap over time. Stronger institutions, lower public debt, and stable currencies all help. Damodaran notes these changes could cut country risk by one to two points. A lower premium would lift values across the region.

Buyers and sellers should agree on the risk inputs early. A one-point change in the premium shifts the price by a wide margin. Document the source for every premium you apply. Clear assumptions speed up the negotiation and reduce later disputes.

What Questions Do Founders Ask Most Often About Valuing a Company in Latin America?

What is the most common valuation method in Latin America?

The most common method is the EBITDA multiple for established firms. Advisors apply a sector multiple to EBITDA, then adjust for risk. DCF and comparable transactions often confirm the result.

How much is my Latin American services company worth?

Your company is worth roughly 6.7x EBITDA at the 2025 regional median. Project-heavy firms sit near 4x to 7x. Recurring-revenue, multi-country firms reach 8x to 12x.

Why are LatAm valuations lower than US valuations?

LatAm valuations are lower because buyers add a country risk premium near 3.5%. Currency swings and inflation also shrink dollar cash flows. Identical financials yield a lower price than in the US.

How does recurring revenue change my valuation?

Recurring revenue raises your valuation by 1.5x to 3x on the EBITDA multiple. Firms with 70% or more recurring revenue trade at 7x to 12x ARR. It is the strongest single lever you control.

Which countries carry the lowest valuation risk?

Chile carries the lowest country risk premium at about 1.10%. Peru and Mexico follow near 2%. Brazil sits highest among major markets at about 3.24%.

When is the best time to get a valuation?

The best time is 12 to 18 months before a planned sale. This gives you room to raise recurring revenue and margins. An early valuation reveals which levers move your number most.

Ready to Value Your Latin American Company?

The Startup VC is Craig Dempsey’s family office and company builder across Latin America. We create, back, and guide scalable ventures, drawing on real operating experience from companies like Biz Latin Hub in 17 countries. Our team helps founders value, prepare, and grow service businesses before a sale or raise. We bring hands-on playbooks, regional networks, and compliance know-how to every deal. Learn more about our investment focus or read about founder Craig Dempsey. Contact us today to start the conversation.