Selling a company in Latin America takes 6 to 12 months. Four sell-side stages drive the process: prepare, market, diligence, and close.

Latin America saw 700+ M&A deals worth over EUR 280 billion in 2024. Deal counts rose 12% in 2025. Brazil drives 60% of regional deal value. Strategic buyers grew acquisitions 26% in H1 2025.

The Startup VC has worked alongside Latin American founders across 17 markets through Biz Latin Hub. Craig Dempsey has guided founder exits, cross-border deals, and post-close transitions. Below, you will find the full sell-side playbook. Topics include deal structures, the four-stage timeline, total costs, tax exposure by country, and top founder mistakes.

What Does It Mean to Sell a Company in Latin America?

Selling a company in Latin America means transferring ownership of your business to a buyer. You use one of three legal structures: share sale, asset sale, or merger.

In a share sale, the buyer takes over your company’s equity. Assets, liabilities, contracts, and obligations all transfer with the shares. In an asset sale, the buyer purchases selected balance sheet items. Liabilities can stay with the seller. In a merger, two entities combine into a single surviving company.

Sellers usually prefer share sales. They produce cleaner exits and simpler post-closing duties. Buyers often prefer asset sales. They limit exposure to unknown legal liabilities from the seller’s entity.

| Structure | Seller Benefit | Buyer Benefit | Common in LatAm |

|---|---|---|---|

| Share sale | Clean exit, simpler taxes | Full continuity of contracts | Most common for tech/SaaS |

| Asset sale | Selective transfer | Avoids hidden liabilities | Common in distressed sales |

| Merger | Tax-deferred in some cases | Combined synergies | Used for cross-border combinations |

Latin American jurisdictions add layers the US deal flow does not. In Brazil, due diligence finishes before the acquisition agreement is signed. Most LatAm targets are family-owned or led by long-tenured teams. That adds diplomatic work on top of legal review.

M&A accounts for 67% of all VC-backed exits in Latin America. Latin America recorded 79 VC-backed exits worth USD 1.8 billion in 2024. The total recovered to USD 4.9 billion across 63 transactions in 2025.

Why Are Founders Selling Companies in Latin America Right Now?

Founders are selling companies in Latin America right now because three trends have converged. Deal activity has rebounded. Valuations have stabilized. Buyer demand has returned across multiple sectors.

Latin America M&A activity rose 12% year-over-year in 2025 after three years of decline. Brazil, Mexico, Chile, Argentina, and Colombia lead the regional recovery. Strategic buyers drove the largest gains.

Several forces are pushing founders to exit now:

- Strategic buyer demand. Sales to strategics jumped 26% in H1 2025. Deal value more than doubled.

- PE divestment pressure. Private equity firms accounted for 71% of capital deployed in 2024 divestments. That drives continued sell-side momentum.

- Sector tailwinds. Fintech accounted for 24% of April 2025 M&A activity. AI, Data, and Automation reached 17%. IT Services followed at 13%.

- Unicorn pipeline. Latin America has 50+ unicorns as of early 2025. These create acquisition target pools for global buyers.

- Closing window concerns. 2026 macro uncertainty pushed many founders to close deals in 2025 rather than risk a worse environment.

Recent landmark exits show the appetite. Biz Latin Hub was acquired by Vistra in December 2025. Kaspi acquired Brazil’s Stone. Strategic buyers and PE funds compete for the same targets across the region.

Energy, financial services, and manufacturing are emerging growth drivers. Founders in these sectors face strong buyer competition right now.

Cross-border deal flow is also growing. US, European, and Asian acquirers all want exposure to Latin America’s 650 million consumers. Founder exits in 2025 increasingly closed at premium multiples over 2023 levels. The window favors prepared sellers.

What Are the Main Steps in a LatAm M&A Process?

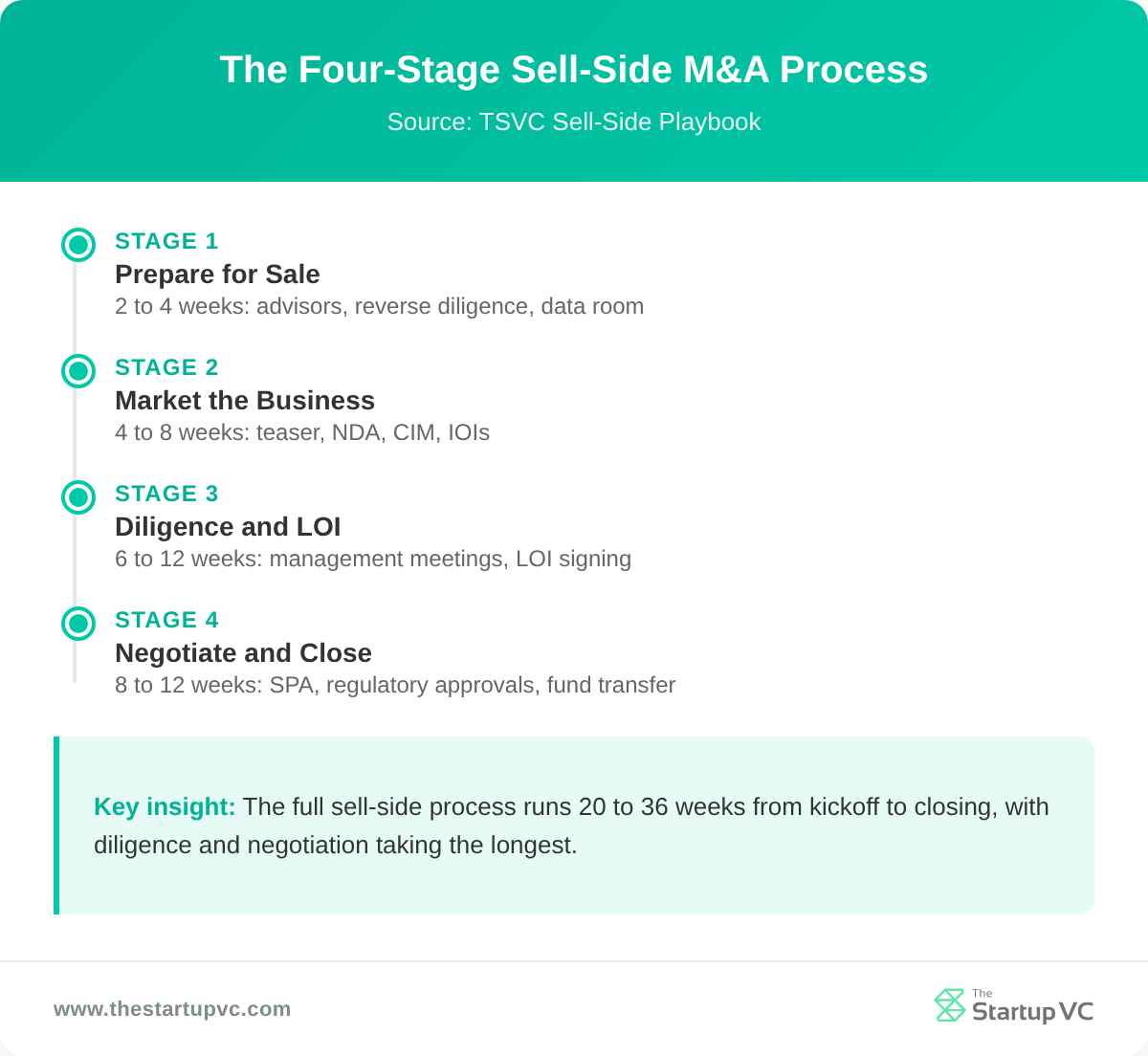

A LatAm M&A process follows four sell-side stages. These are preparation, marketing, due diligence with bid evaluation, and final negotiation through closing.

Each stage has clear deliverables and decision points. Skipping or rushing any stage typically reduces final sale price.

Stage 1: Prepare for Sale

Preparation takes 2 to 4 weeks. You assemble your advisory team, choose an auction strategy, and run reverse due diligence on your own company.

Reverse diligence surfaces issues before buyers find them. You fix or disclose them on your terms. Key deliverables include:

- Three to five years of audited financial statements

- A current capitalization table with all share classes

- A product or service overview document

- Customer concentration and contract reports

- IP, employment, and tax filings ready for the data room

Your advisory team usually includes a sell-side M&A advisor or investment bank. You also add corporate counsel in your jurisdiction and a tax advisor. For cross-border deals, add local counsel in each country where you have entities. Most founders also engage a quality of earnings (QoE) firm to validate financials.

Stage 2: Market the Business

Marketing engages multiple buyers and builds competitive tension. The sequence is teaser, NDA, CIM, then VDR access.

The Teaser is anonymous. It identifies industry, geography, and size band only. Once a buyer signs the NDA, you share the Confidential Information Memorandum (CIM). Qualified bidders enter the Virtual Data Room (VDR) and submit Indications of Interest (IOIs).

Marketing typically runs 4 to 8 weeks. Your advisor manages outreach to a curated list of 20 to 100 buyers. Strategic acquirers, private equity firms, and family offices all receive the Teaser. The auction style can be broad (wide net) or targeted (5 to 15 named bidders).

Stage 3: Run Due Diligence and Evaluate Bids

Management presentations and Letter of Intent (LOI) submissions take 4 to 6 weeks. Buyers conduct financial, legal, tax, and commercial diligence. You select the top bidders for management meetings.

The LOI is the most critical document of the entire process. You lose 95% of your negotiation power once it is signed. Lock in price, structure, escrow, and key terms before signing.

Stage 4: Negotiate and Close

Final negotiation and closing takes 8 to 12 weeks. You and the buyer draft the definitive Share Purchase Agreement (SPA) or Asset Purchase Agreement (APA). Regulatory filings, escrow setup, and fund transfer follow.

In Brazil and most LatAm jurisdictions, diligence wraps before signing. That shifts more risk to the front end of the timeline. Cross-border deals add antitrust filings in CADE (Brazil), COFECE (Mexico), or FNE (Chile).

Negotiation focuses on representations and warranties, indemnity caps, escrow size, and earnout structure. Most buyers ask for survival periods of 12 to 24 months for general reps. Tax and fundamental reps often survive 6 to 7 years.

How Long Does It Take to Sell a Business in Latin America?

Selling a business in Latin America takes 6 to 12 months from kickoff to closing. The industry average for global M&A is seven months. LatAm deals trend slightly longer due to cross-border complexity.

The four stages distribute time unevenly. Marketing and diligence take the longest. The table below shows typical durations.

| Stage | Duration | Drivers of Variation |

|---|---|---|

| Preparation | 2-4 weeks | Quality of existing records |

| Marketing | 4-8 weeks | Auction breadth and buyer interest |

| Diligence + LOI | 6-12 weeks | Deal size and complexity |

| Negotiation + Close | 8-12 weeks | Regulatory approvals required |

Mid-market deals (USD 50-500 million) typically run 45-90 days of diligence alone. Large cross-border deals over USD 500 million can take 90-180 days of diligence. For deeper coverage, see our Latin America M&A due diligence guide.

Several factors stretch LatAm timelines:

- Family-owned targets. Legacy record-keeping requires reconstruction before diligence can finalize.

- Regulatory review. Antitrust filings in CADE, COFECE, or FNE add 30 to 90 days.

- Currency and tax planning. Cross-border deals require treaty mapping in multiple jurisdictions.

- Buyer financing. Lender diligence and commitment letters extend close timelines.

- Brazilian custom. Diligence finalizes before signing in Brazil, unlike many US deals.

Clean software-heavy targets with sophisticated sellers can compress diligence to 3-4 weeks. Most LatAm founder-led companies do not hit that timeline.

How Much Does a LatAm Founder Exit Cost?

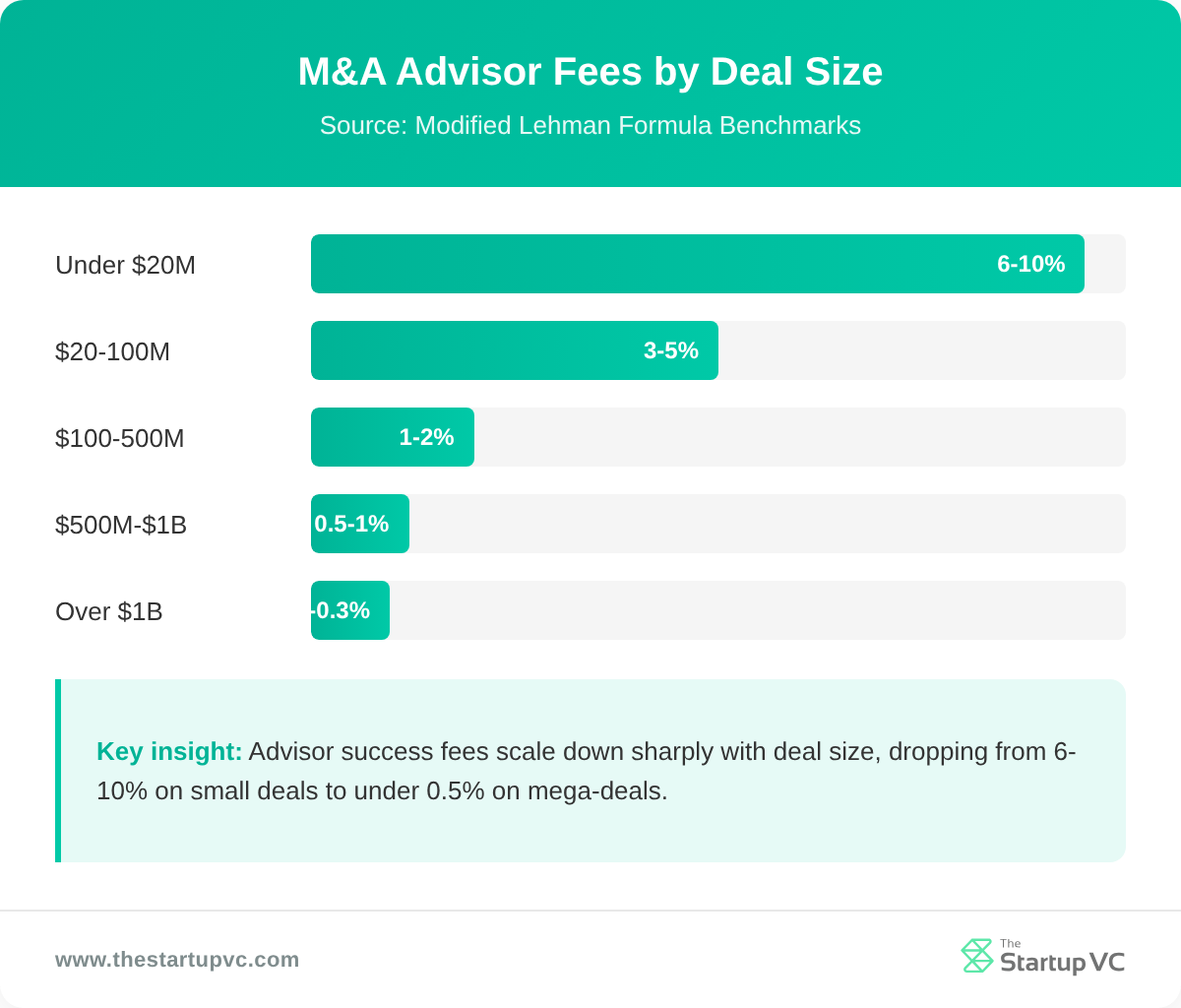

A LatAm founder exit costs 8% to 20% of the gross sale price. The total covers advisor fees, legal costs, taxes, and escrow holdbacks combined. The biggest line items are advisor success fees, capital gains tax, and indemnity escrow.

Advisor and Legal Fees

M&A advisor success fees in the middle market typically run 1% to 4% of total sale price. The Modified Lehman formula (3-3-2-1-1) is common for sell-side mandates. The Double Lehman scale (10-8-6-4-2) sometimes applies to deals under USD 20 million.

A USD 500 million deal might carry a 1% advisor fee, or USD 5 million. A USD 5 billion deal might run 0.2-0.3%, or USD 10-15 million. Legal counsel typically adds USD 500,000 to USD 2 million for mid-market deals.

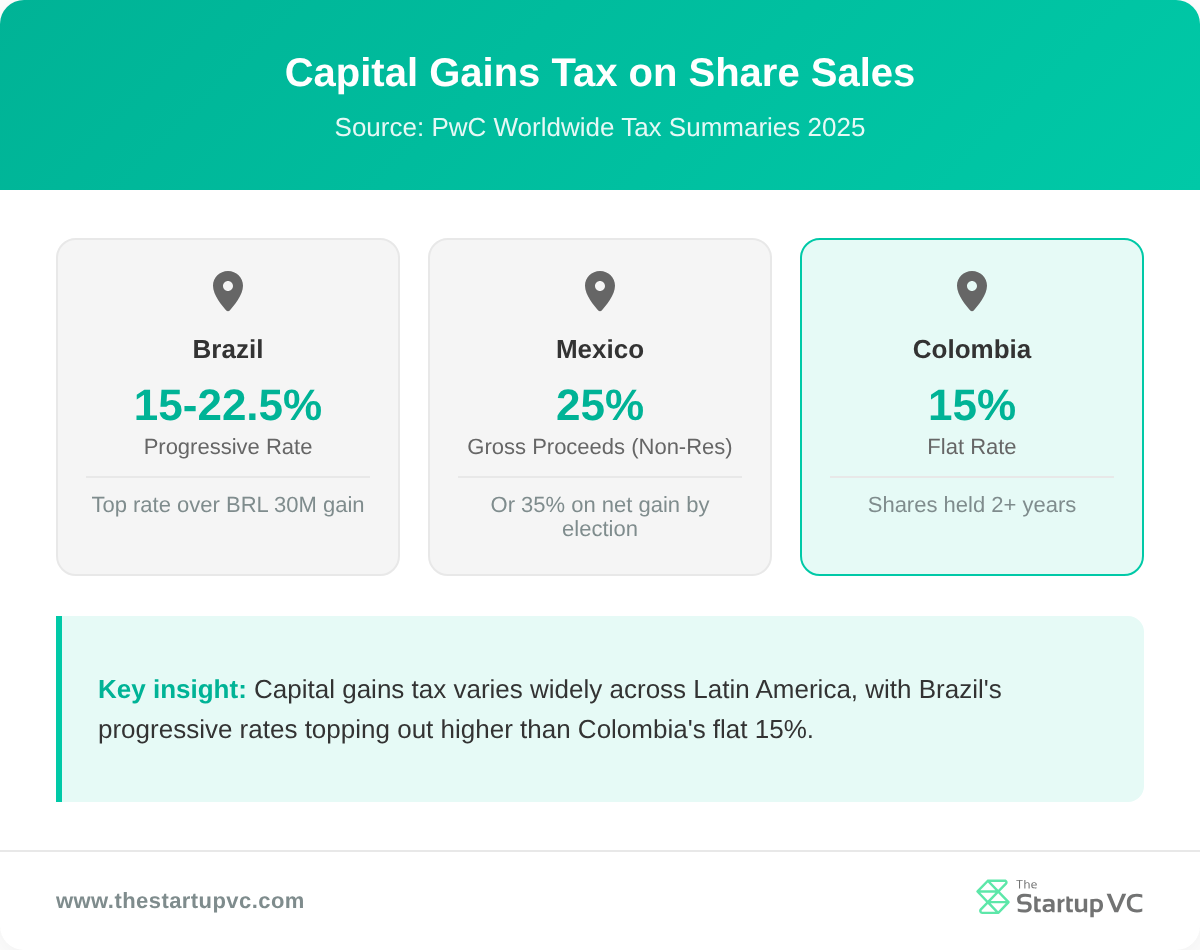

Capital Gains Tax by Country

Latin America has wide capital gains tax variation across the major markets. Founders selling shares face these rates:

| Country | Capital Gains Rate | Notes |

|---|---|---|

| Brazil | 15-22.5% | Progressive, top rate over BRL 30M |

| Mexico | 25% gross OR 35% net | Non-resident election available |

| Colombia | 15% | If shares held 2+ years |

| Chile | 10% | Article 107 for listed shares |

| Argentina | 15% | Standard rate on share sales |

Non-residents in low-tax jurisdictions face a flat 25% rate on Brazilian capital gains. Tax treaty positions can lower withholding obligations in Mexico, Chile, and Colombia.

Escrow, Holdbacks, and Insurance

Indemnity escrows in LatAm deals hold 5% to 10% of purchase price for 12 to 18 months. The escrow secures seller representations and warranties.

Buyers can purchase reps and warranties insurance for 10-15% coverage of deal value. This reduces or eliminates escrow requirements. RWI premiums typically run 3-5% of coverage limits in Latin American transactions.

What Mistakes Do Founders Make When Selling a Company in Latin America?

The mistakes founders make when selling a company in Latin America fall into five categories. These are weak preparation, divided focus, sloppy LOIs, single-buyer negotiations, and ignored tax exposure.

Each mistake can cost millions at closing or kill the deal entirely.

Going to Market Unprepared

Lack of seller preparedness is the top sell-side error. Founders underestimate the time required to clean up financial records, customer contracts, IP filings, and statutory registers.

Buyer diligence requests typically include 200 to 500 documents. Missing or outdated records signal poor management and trigger price reductions. Start preparation 12 to 18 months before launch. See our guide to preparing a company for sale in Latin America for the complete checklist.

Letting the Deal Distract You from the Business

Most deal-killing errors happen when founders divide focus between running a deal and running the company. Performance dips during the sale process trigger buyer walkaway.

Two fatal deal killers come from divided focus:

- Losing a major customer. Even one large customer exit during diligence can cut valuation 15-30%.

- Missing financial projections. Buyers reprice or walk if quarterly results miss the projections in your CIM.

Hire an advisor to run the sale process. Keep your operational team focused on hitting numbers.

Weak LOI Drafting

Skimping on LOI details is a top-five seller error. Founders lose 95% of their negotiating power after the LOI is signed.

Lock these terms in the LOI:

- Purchase price and form of consideration

- Earnout structure and milestones

- Escrow size and duration

- Exclusivity period length

- Representations and warranties scope

Single-Buyer Negotiations

Single-buyer negotiations destroy competitive tension. Becoming emotionally attached to one bidder early in the process shifts power to the buyer.

A buyer who senses they are the favorite will push for lower price and weaker terms. Keep two to four serious bidders engaged until signing.

Underestimating Cross-Border Tax

Latin American founders frequently underestimate cross-border tax exposure. Capital gains rates, withholding obligations, and treaty positions vary widely across Brazil, Mexico, Colombia, and Chile.

Failing to plan can cost 5-15% of net proceeds at closing. Pre-sale tax structuring through holding companies or treaty residency planning can save founders millions. Engage tax counsel 6-12 months before launching the sale process.

What Questions Do Founders Ask Most Often About Selling a Company in Latin America?

How Much Is My Company Worth?

Your company is worth what a buyer will pay, anchored to comparable transactions. Latin American mid-market companies transact at 4-8x EBITDA. SaaS and fintech deals run 8-15x revenue multiples. A formal valuation report sets your reserve price before going to market. See our guide to valuing a company in Latin America for the full methodology.

Who Buys Latin American Companies?

The main buyers of Latin American companies are strategic acquirers and private equity firms. Strategic buyers drove 26% more deals in H1 2025 than the prior year. PE firms accounted for the majority of buyer activity for deals over EUR 400 million.

How Do I Keep the Sale Confidential?

You keep the sale confidential by using staged disclosure. NDAs are the first document executed before any company information is shared. The Teaser document is anonymous and identifies only industry, geography, and size band. CIM access requires a signed NDA.

Do I Have to Stay After the Sale?

Yes, most founders stay after the sale for 12 to 36 months. Earnouts or transition periods often tie 20-30% of purchase price to post-close performance milestones in middle-market deals.

What Taxes Will I Pay?

You will pay capital gains tax in your country of tax residence. You may also pay tax where the shares are sold. Brazil charges 15-22.5%. Mexico charges 25% on gross or 35% on net for non-residents. Colombia charges 15% if shares are held two years or more. Chile charges 10% on listed shares under Article 107 rules. Tax treaty positions can reduce withholding.

When Is the Best Time to Sell?

The best time to sell is when revenue growth has accelerated for 3-4 quarters and EBITDA margins are improving. Distressed sales transact at 30-50% discounts to comparable healthy multiples. Time the market when buyers compete for your sector.

Ready to Sell Your Company in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder. We help founders across Latin America create, scale, and exit ventures. We have guided sell-side processes in 17 countries through Biz Latin Hub. Our investment focus targets cash-flow positive service businesses across the region.

Our portfolio companies reflect the same playbooks we apply to founder exits. Whether you are preparing for diligence or selecting an advisor, we bring the experience that closes deals at full value.

Contact us today to discuss your exit strategy.