Services companies in Latin America trade at 6.7x EV/EBITDA, with multi-country platforms commanding premium multiples.

Latin America recorded 2,650 M&A deals worth US$96 billion in 2025, up 13% from 2024. Services firms with recurring revenue, expanding margins, and multi-country scale trade at 8x to 12x EBITDA, above the 6.7x regional median.

The Startup VC is Craig Dempsey’s family office and company builder. Portfolio companies like Biz Latin Hub operate across 17 Latin American countries. Below, you will find the four value drivers buyers focus on, the preparation timeline, and the deal structures that protect founder upside.

What Drives the Valuation of a Services Company in Latin America?

The valuation of a services company in Latin America is driven by five factors. These are recurring revenue share, EBITDA margin, customer concentration, growth rate, and geographic scale. The median services multiple in LatAm sits at 6.7x EBITDA in 2025.

Strategic buyers ask five questions before pricing a deal:

- Recurring revenue mix. What share of revenue is contracted and predictable?

- EBITDA margin quality. Is the margin structural or driven by one-time cost cuts?

- Customer concentration. Does any single client represent more than 15% of revenue?

- Growth trajectory. Is annual growth above 20% and supported by repeatable channels?

- Geographic footprint. Does the company operate in two or more countries?

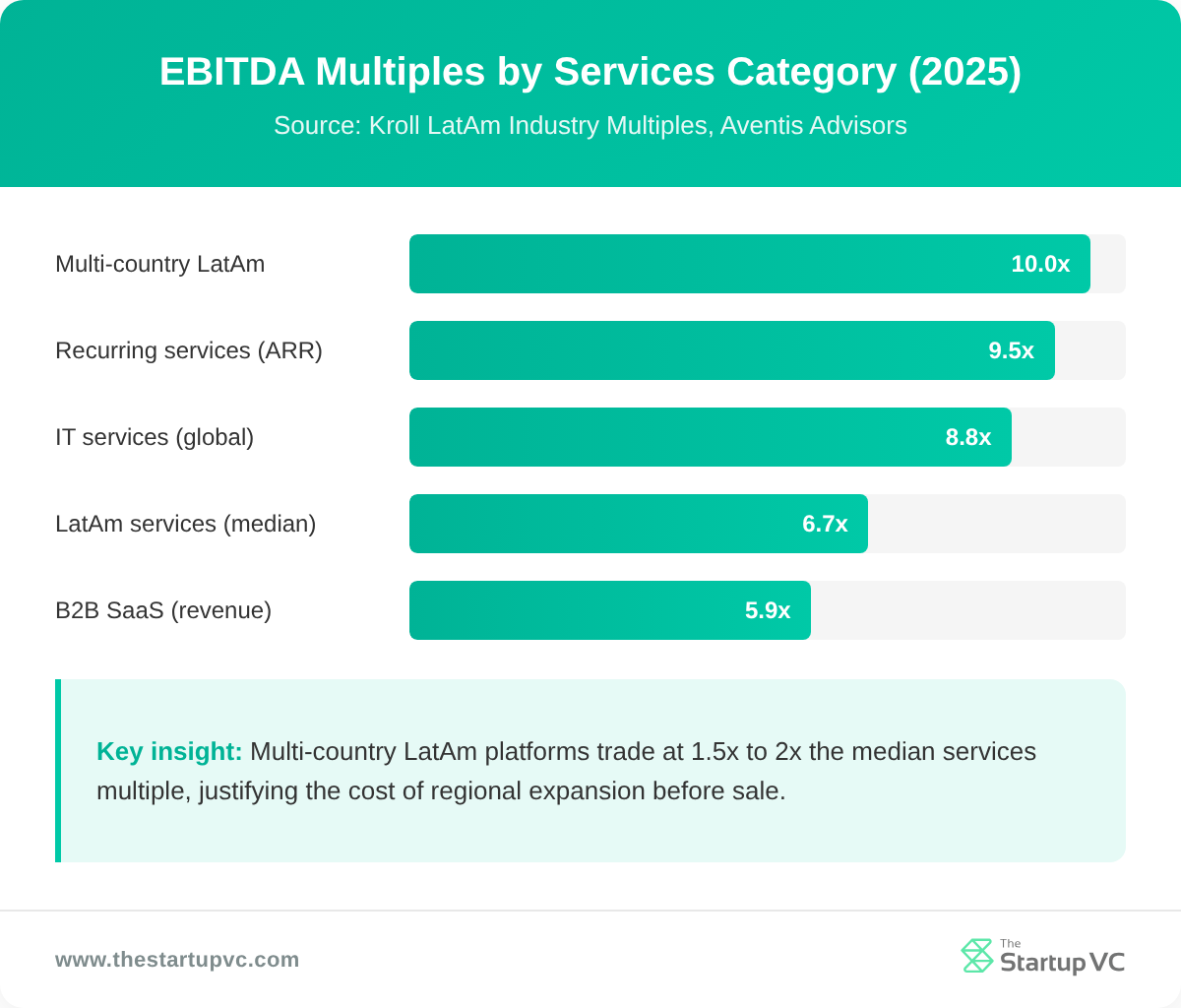

The table below shows how different services categories trade in 2025.

| Services Category | Median EV/EBITDA Multiple | Notes |

|---|---|---|

| Commercial and professional services (LatAm) | 6.7x | Down from 8.5x in late 2024 |

| IT services (global) | 8.8x | Q4 2025 median |

| B2B SaaS (revenue multiple) | 5.9x | 2025 settled level |

| Recurring revenue services with high ARR | 7x to 12x ARR | Mid-sized companies |

| Multi-country LatAm platforms | 8x to 12x EBITDA | Premium for regional scale |

Companies whose growth rate plus profit margin exceeds 40% command premium multiples. This is known as the Rule of 40. Vistra acquired Biz Latin Hub in December 2025. This deal shows strategic buyers paying for regional service platforms. For a deeper view on valuation methods, see how to value a company in Latin America.

How Can You Convert Project Revenue Into Recurring Revenue?

You can convert project revenue into recurring revenue by three moves. Productize repeatable engagements. Launch fixed-fee retainers. Add managed service modules. This shift typically lifts multiples from 4-7x EBITDA on project work to 7-12x ARR on recurring contracts.

The conversion path follows three stages. Each stage takes 4 to 6 months on average.

- Productize the repeatable parts. Identify which engagements you deliver more than five times per year. Document the scope, fix the pricing, and remove custom variations.

- Wrap deliverables into a monthly retainer. Convert the productized scope into a 12-month contract. Charge monthly. Include defined SLAs and quarterly business reviews.

- Add managed service modules. Layer ongoing support, monitoring, or reporting on top of the retainer base. These modules raise customer lifetime value and reduce churn.

Buyers reward recurring revenue because it is predictable and transferable. Annual Recurring Revenue (ARR) gives buyers a stable forecast for cash flow. Project-heavy firms force buyers to discount future revenue, dragging the multiple down.

Industry-specific service firms with deep domain expertise and high switching costs trade at premiums. A LatAm legal compliance firm with multi-year retainers in 5 countries will out-multiple a generalist project shop. Both can have the same EBITDA, but the recurring firm wins.

How Do You Expand Margins Before a Sale?

You expand margins before a sale by four levers. Raise prices on high-demand services. Phase out low-margin work. Productize delivery. Shift labor to lower-cost Latin American hubs. These moves typically lift EBITDA margins by 5 to 15 points within 12 to 18 months.

Four levers drive margin expansion in services businesses:

- Targeted price increases. Raise prices 5% to 15% on services with inelastic demand. Volume usually holds or drops only slightly, lifting margin directly.

- Service line pruning. Phase out services with margins below your blended target. Free up team capacity for high-margin work.

- Delivery productization. Replace custom delivery with standardized packages and fixed scopes. This cuts custom labor cost and reduces scope creep.

- LatAm labor arbitrage. Move delivery teams to Medellin, Bogota, Buenos Aires, or Lima. Maintain North American pricing while cutting labor cost by 40% to 60%.

Buyers prefer structural margin gains over one-time cost cuts. Structural gains include pricing power, product mix shifts, and offshore delivery. One-time gains include layoffs and vendor renegotiations, which buyers discount during due diligence.

Consider a LatAm marketing services firm. The firm moves senior delivery roles from Mexico City to Medellin. Blended cost per head drops by 35%. If the firm holds pricing flat, EBITDA margin can rise from 18% to 28% over 12 months. At an 8x multiple, that 10-point margin gain on US$5M revenue adds US$4M to enterprise value.

How Can You Reduce Customer Concentration Risk?

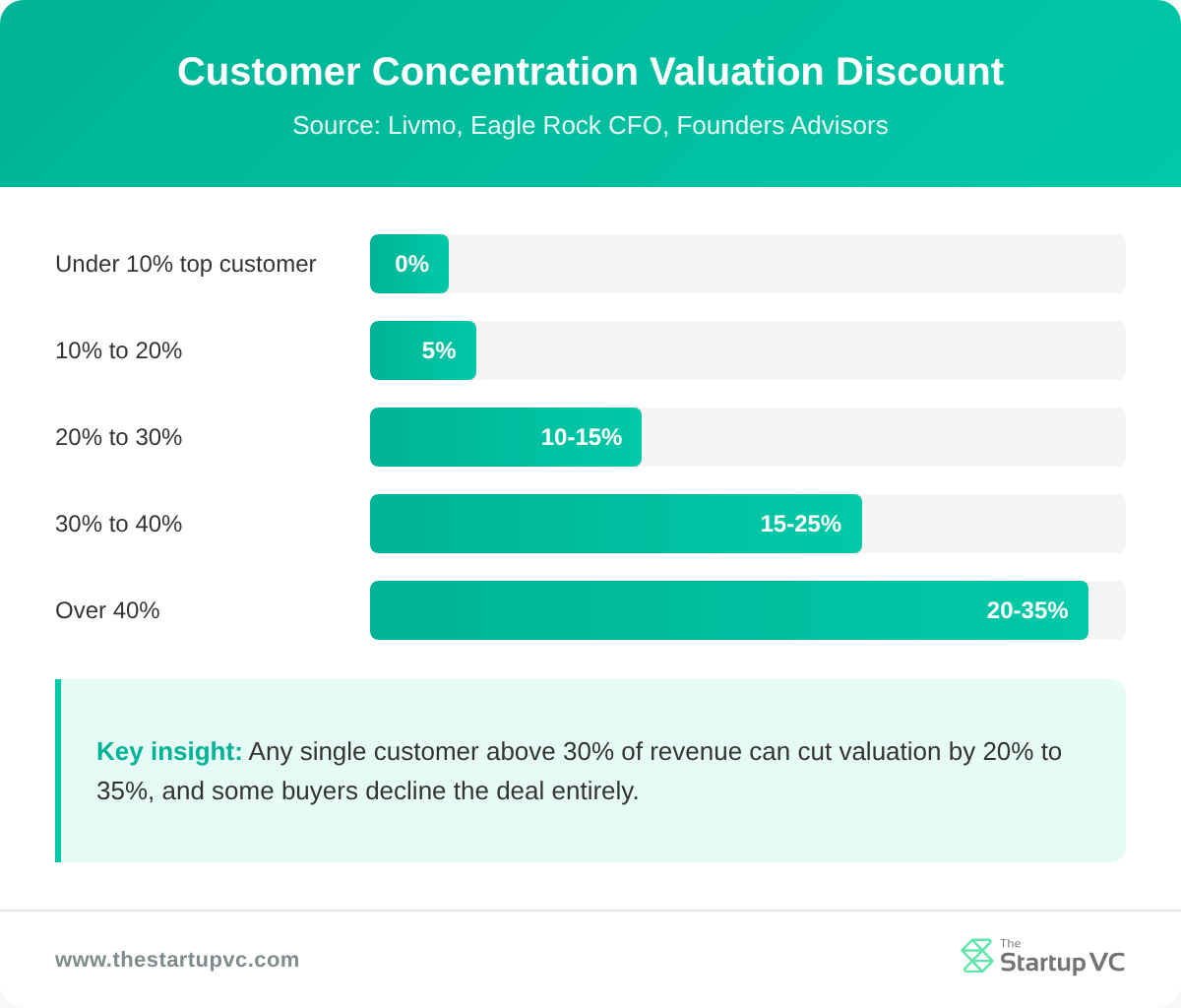

You can reduce customer concentration risk by three moves. Add multi-year contracts. Expand into adjacent customer segments. Cap top-customer revenue share at 15%. Starting this work 12 to 24 months before sale gives buyers a clean concentration profile.

Buyer thresholds for concentration risk are well established. The table below shows the typical valuation impact.

| Top Customer Share of Revenue | Buyer Reaction | Multiple Impact |

|---|---|---|

| Under 10% | No concern | Full multiple |

| 10% to 20% | Detailed review | Minor discount or none |

| 20% to 30% | Multiple discount | 0.5x to 1.0x reduction |

| 30% to 40% | Earnout proposed | 1x to 2x reduction |

| Over 40% | Deal often declined | 20% to 35% valuation cut |

Founders have four mitigation moves that work in 6 to 12 months:

- Lock in multi-year contracts. Convert open-ended concentration into a defined 2-3 year window with auto-renewal clauses.

- Diversify into adjacent verticals. Land 3 to 5 new logos in different industries to reduce single-vertical exposure.

- Cross-sell within existing accounts. Spread revenue across multiple departments inside large clients, reducing single-decision-maker risk.

- Price discipline on top accounts. Avoid discounting top customers further, which lowers their unit economics and signals dependency.

When concentration cannot be cleared by close, buyers often propose earnout structures. These shift performance risk to the seller and reduce upfront cash at close.

Why Does Multi-Country Scale Increase Your Valuation?

Multi-country scale increases your valuation because it signals durable demand, lowers single-market risk, and gives buyers a regional platform. LatAm service firms operating in 5 or more countries can command 1x to 3x higher EBITDA multiples. The premium reflects reduced country risk and broader buyer interest.

The premium comes from four sources:

- Reduced country risk. Buyers diversify exposure to currency swings, tax changes, and political risk across multiple markets.

- Cross-border revenue. Service firms with clients in Mexico, Colombia, Chile, and Argentina prove they can win business beyond their home market.

- Cost arbitrage. Multi-country footprints let firms source labor in Medellin, deliver to clients in Sao Paulo, and bill in US dollars.

- Strategic buyer fit. Multinationals expanding into LatAm pay premiums for platforms that already operate across the region.

Brazil and Mexico captured 78.5% of all venture capital in 2025. Service firms operating beyond these two markets reach a much larger buyer pool. Vistra’s December 2025 acquisition of Biz Latin Hub valued the firm’s 17-country footprint as a key asset.

Multi-country scale also unlocks Multilatina buyers. These are regional champions like Falabella, Cencosud, and Grupo Argos that look for service partners with matching footprints. Single-country firms cannot serve these buyers as primary vendors.

The Startup VC backs cross-border ventures with regional reach. Learn more about our criteria at the investment focus page.

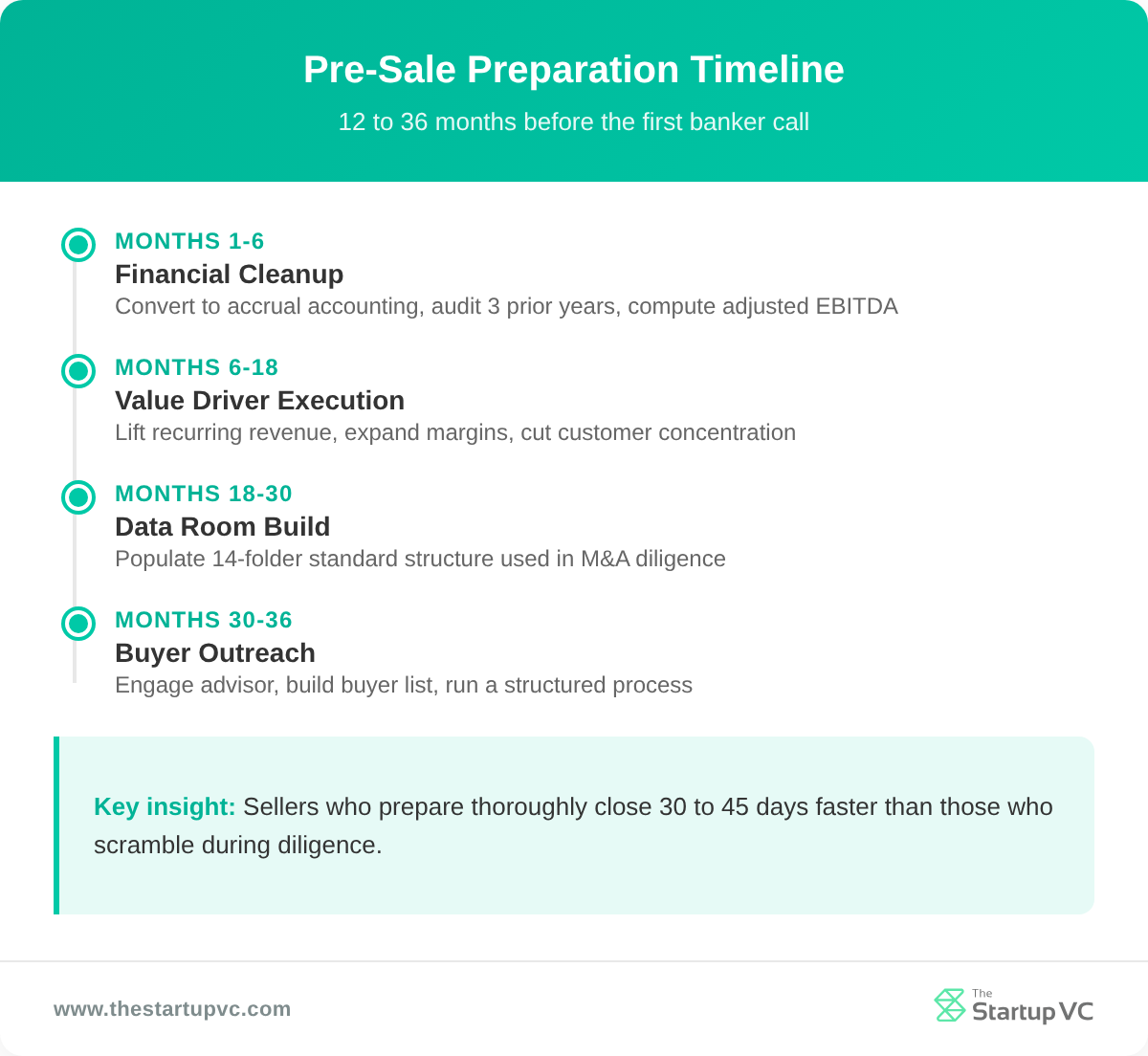

What Are the Main Steps to Prepare a Services Company for Sale in Latin America?

The main steps to prepare a services company for sale in Latin America are four. Financial cleanup. Value driver execution. Data room build. Buyer outreach. The full preparation runs 12 to 36 months before the first banker call.

The recommended timeline breaks into four phases:

- Months 1-6: Financial cleanup. Convert to accrual accounting. Audit the prior 3 years. Separate owner-discretionary expenses to compute adjusted EBITDA.

- Months 6-18: Value driver execution. Lift recurring revenue share, expand margins, and reduce customer concentration. This is where the multiple uplift comes from.

- Months 18-30: Data room build. Populate the virtual data room with the standard 14-folder structure used in M&A diligence.

- Months 30-36: Buyer outreach. Engage an advisor, build the buyer list, and run a structured process.

The standard data room covers 14 folder areas. These include corporate documents, financials and KPIs, tax, legal contracts, customers, HR, IP, security, regulatory compliance, litigation, insurance, real estate, and disclosure schedules.

Five documents are most commonly missing during diligence. These are IP assignment agreements for founders and contractors. Contracts with change-of-control provisions. Sales tax nexus analysis. Contractor classification documentation. Historical board consents. Fix these gaps before going to market.

Sellers who prepare thoroughly close 30 to 45 days faster than those who scramble during diligence. Deals with medium-length due diligence (around 139 days) achieve the highest completion rates and the best post-close performance. For a complete walkthrough, read our guide on how to sell a company in Latin America.

What Questions Do Founders Ask Most Often About Services Company Valuation in Latin America?

What multiple does a services company in Latin America trade at?

A services company in Latin America trades at a median 6.7x EV/EBITDA in 2025, down from 8.5x at end of 2024. IT services trade at 8.8x globally. Multi-country platforms with recurring revenue can reach 10x to 12x.

How much can recurring revenue lift my valuation?

Recurring revenue can lift your valuation by 1.5x to 3x EBITDA multiple. Project-heavy firms trade at 4x to 7x EBITDA. Firms with 70% or more recurring revenue trade at 7x to 12x ARR. The gap reflects buyer preference for predictable cash flow.

How long does it take to prepare a services company for sale?

It takes 12 to 36 months to prepare a services company for sale. The first 18 months are for value creation, including margin expansion and concentration cleanup. The final 12 to 18 months are for data room build and buyer outreach.

Which buyers acquire services companies in Latin America?

The buyers who acquire services companies in Latin America include four groups. Strategic acquirers like Vistra. Multinationals expanding into the region. Regional Multilatinas. Private equity funds with LatAm mandates. Latin America saw 174 tech M&A deals in Q1-Q3 2025 alone.

What is the customer concentration threshold buyers care about?

The customer concentration threshold buyers care about is 15% to 20% of revenue from a single client. Above 30%, buyers apply a 20% to 35% valuation discount or decline the deal. The “10% rule” used by lenders flags any customer above 10% of revenue.

How does multi-country scale change my multiple?

Multi-country scale changes your multiple by adding 1x to 3x EBITDA. Single-country firms in Mexico or Brazil sell to a smaller buyer pool. Firms operating across 3 or more LatAm countries attract strategic buyers paying premiums for regional platforms.

Ready to Increase Your Services Company Valuation Before a Sale?

The Startup VC is Craig Dempsey’s family office and company builder. We work with founders 12 to 36 months out from sale. We help build recurring revenue, expand margins, reduce concentration, and scale across Latin American markets. Our team has built and scaled service businesses across 17 countries. See our portfolio companies, including Biz Latin Hub. Contact us today to discuss your sell-side preparation roadmap.