EBITDA multiples in Latin American M&A run 4x to 12x in 2026, with a 6.7x services median.

EBITDA multiples in Latin America averaged 6.7x for services firms in 2025, down from 8.5x a year earlier. Chile prices near 9.7x, Brazil near 7.2x, and the region closed 2,650 deals worth about US$96 billion.

The Startup VC, Craig Dempsey’s family office and company builder, has helped value and structure deals across Latin America. This 2026 benchmark draws on Damodaran, Kroll, GF Data, and Bain figures. Below, you will find multiples by sector and country, the key drivers, and the US comparison.

What Are EBITDA Multiples and Why Do They Matter in Latin American M&A?

EBITDA multiples are valuation ratios that price a company against its yearly operating earnings. In Latin American M&A, the EV/EBITDA multiple sets the starting point for most deals. Private-company multiples here usually run from 4x to 12x. The regional services median was 6.7x in 2025, down from 8.5x in late 2024.

EV/EBITDA matters for three main reasons:

- It ignores capital structure, so firms with different debt compare cleanly.

- It links price directly to cash earnings, not accounting profit.

- It travels across borders, which helps buyers compare countries.

EBITDA works as a rough proxy for operating cash flow. That helps buyers compare firms with different tax and debt setups. Latin America stayed busy in 2025. The region recorded 2,650 M&A deals worth about US$96 billion, up 13% in volume from 2024.

How Is an EV/EBITDA Multiple Calculated?

An EV/EBITDA multiple is calculated by dividing enterprise value by EBITDA. EBITDA stands for earnings before interest, taxes, depreciation, and amortization. Enterprise value equals equity value plus debt minus cash. The result shows how many times yearly earnings a buyer pays. A “5x EBITDA” offer means five times annual EBITDA. Buyers prefer EBITDA over net income because it removes financing and tax noise.

Consider a Colombian software firm with US$4 million in EBITDA. At a 7x multiple, its enterprise value is US$28 million. Subtract US$3 million of net debt for US$25 million of equity value. The multiple turns one earnings figure into a full price.

When Do Buyers Use Revenue Multiples Instead?

Buyers use revenue multiples when a company has thin or negative EBITDA. High-growth and tech firms often fit this case. Public software firms that clear the Rule of 40 trade at about 4.8x revenue. Those that miss it trade at 2.7x. Private lower-middle-market SaaS commonly sells for 4.0x to 5.5x ARR. Once margins hold, buyers shift back to EBITDA multiples. For the full method behind these numbers, see how to value a company in Latin America.

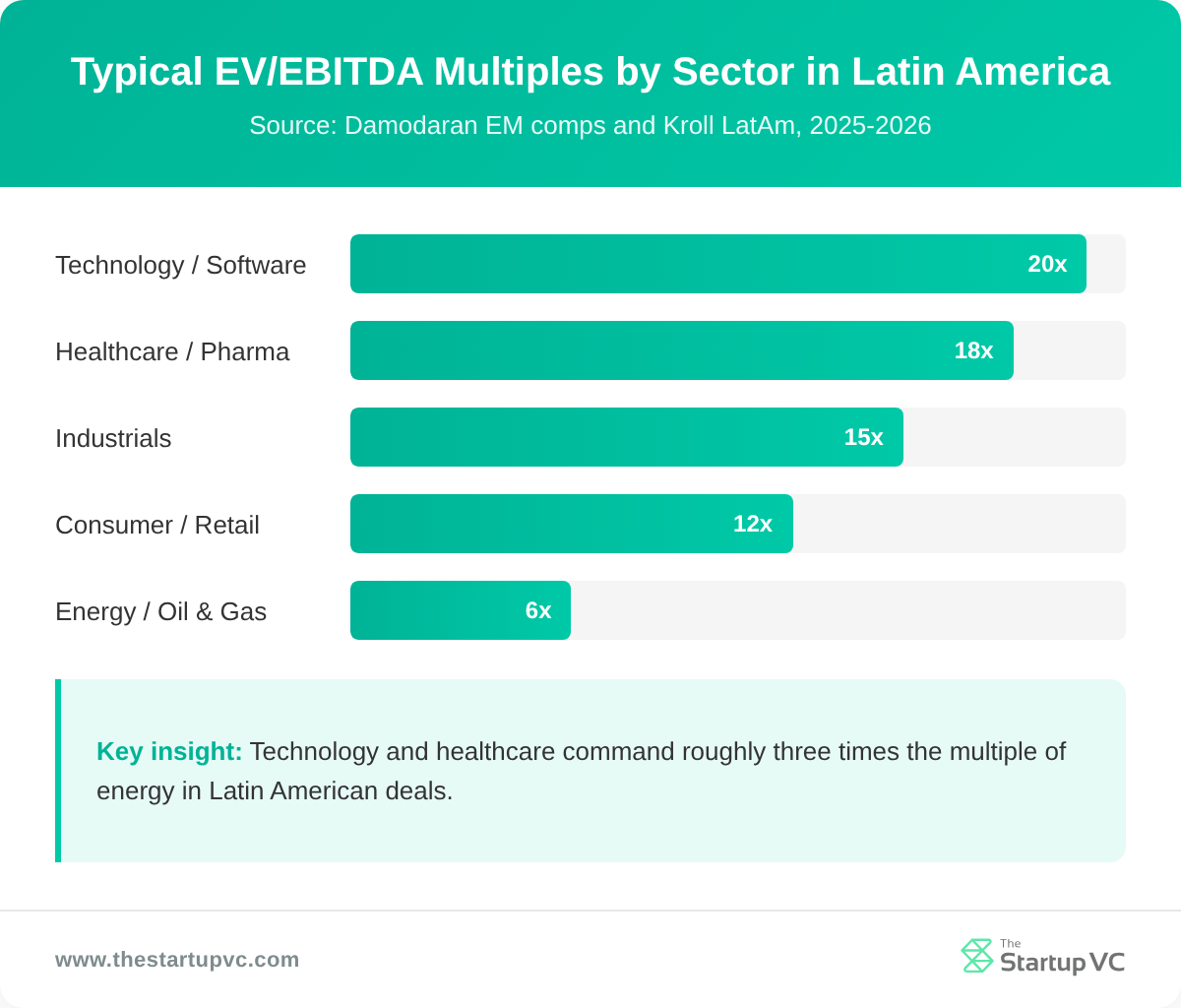

What Are the Average EBITDA Multiples by Sector in Latin America?

Average EBITDA multiples in Latin America range from about 5x to nearly 40x by sector. Technology and branded consumer staples sit at the top. Telecom and upstream energy sit at the bottom. The table below shows typical 2026 EV/EBITDA ranges by sector.

| Sector | EV/EBITDA range (2026) | Notes |

|---|---|---|

| Technology / software / SaaS | 17x-40x | IT services near 18x, software near 40x |

| Consumer staples & branded goods | 12x-22x | Household products top the band |

| Healthcare / pharma / medical | 11x-21x | Hospitals, pharma, and medtech |

| Real estate | 14x-19x | REITs and property development |

| Media / entertainment / advertising | 11x-25x | Advertising high, broadcasting low |

| Industrials / manufacturing | 11x-25x | Machinery high, construction low |

| Financial services / fintech (non-bank) | ~16x | Banks priced on book value, not EV/EBITDA |

| Food & beverage / agribusiness | 10x-16x | Branded drinks high, farming low |

| Utilities (power, water, renewables) | 9x-15x | Regulated and contracted cash flows |

| Energy / oil, gas & mining | 5x-12x | Mining near 12x, upstream oil near 5x |

| Telecom | ~7x | Lowest, very capital intensive |

| Business / professional services | 6.7x (LatAm median) | Project-heavy firms 4x-7x |

These figures blend Damodaran’s January 2026 emerging-market public comps with Kroll’s Latin America medians. Software and consumer staples earn the richest multiples. Telecom and upstream oil and gas earn the thinnest. Banks are the exception in the table. They trade on book value and earnings, not EV/EBITDA.

Growth, asset intensity, and revenue quality explain most of the spread. Software scales fast and needs little capital, so it leads at 17x to 40x. Machinery clears about 25x, while construction sits near 11x. Telecom and upstream oil and gas carry heavy assets and cyclical prices. That weight keeps their multiples near 5x to 7x.

Here is how to apply the sector table to a real deal:

- Start from the sector range, then move within it for size and growth.

- Discount toward the low end for private, local-currency, or single-country firms.

- Add a premium for recurring revenue, scale, and clean financials.

Sector multiples have also moved fast over the past year. Kroll data shows consumer-discretionary retail jumped from 6.3x to 9.3x. Commercial and professional services fell the other way, from 8.5x to 6.7x. The shifts show why a 2026 benchmark beats older comps. Always anchor a deal to current, sector-specific data.

Why Do Private Latin American Deals Price Below These Public Comps?

Private Latin American deals price below public comps because buyers apply liquidity and country-risk discounts. Region-wide private multiples run about 6x to 10x by industry. That sits roughly 2 to 4 turns below US and developed-market comps. Smaller deal sizes also weigh on private prices. A buyer pool is thinner for a $5 million firm than a listed peer. Thin competition pulls the final price down.

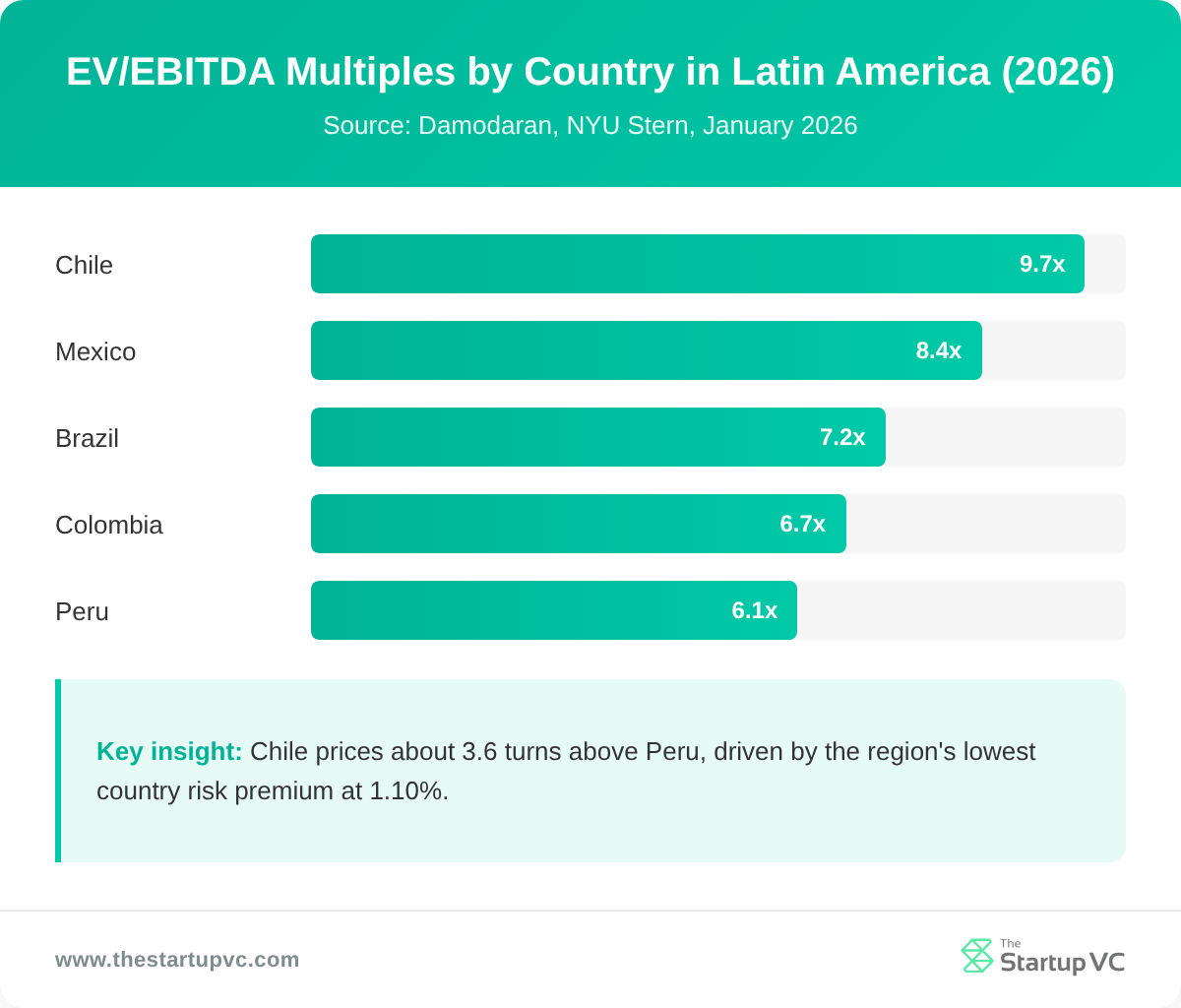

How Do EBITDA Multiples Vary by Country Across Latin America?

EBITDA multiples vary across Latin America, from about 6x in Peru to nearly 10x in Chile. Each market carries its own risk premium, and that gap drives most of the spread. The table below pairs each country’s market EV/EBITDA with its country risk premium.

| Country | Market EV/EBITDA (2026) | Country risk premium | Total equity risk premium |

|---|---|---|---|

| Chile | ~9.7x | 1.10% | 5.33% |

| Mexico | ~8.4x | 2.46% | 6.69% |

| Brazil | ~7.2x | 3.24% | 7.47% |

| Colombia | ~6.7x | 2.85% | 7.08% |

| Peru | ~6.1x | 2.07% | 6.30% |

| Argentina | ~10.4x* | 9.71% | 13.94% |

Argentina’s headline multiple is distorted by inflation, not a sign of cheap risk. These country gaps matter most when you plan to buy a company in Latin America.

Deal flow also shapes which multiples buyers trust. Brazil and Mexico lead Latin America by deal value and volume. TTR Data shows regional M&A value up 19% in 2025. Brazil led, followed by Mexico, Colombia, Argentina, Chile, and Peru. Equity markets confirm the same order on earnings. Forward P/E ratios run from about 13.4x in Brazil to 15.9x in Mexico. Smaller markets like Peru and Colombia trade at an illiquidity discount. Brazil alone closed 1,674 deals worth US$47.9 billion in 2024.

Why Does Chile Price Higher Than Brazil?

Chile prices higher than Brazil because it carries the lowest country risk in Latin America. Chile’s country risk premium is just 1.10%, against 3.24% for Brazil. That lower risk cuts the discount rate and lifts the multiple. Chile holds an investment-grade rating and the region’s cheapest cost of capital. Mexico sits just below Chile on the same logic. Its 2.46% premium keeps its market multiple near 8.4x. That risk spread feeds straight into the discount rate buyers use. The same business sells for more in Santiago than in Lima.

Why Isn’t Argentina’s High Multiple a Bargain?

Argentina’s high multiple is not a bargain because inflation distorts its reported EBITDA. The 10.4x figure reflects depressed earnings and few listed names. Argentina carries the region’s highest country risk premium at 9.71%. Its total equity risk premium reaches 13.94%. Its stocks also trade at a rich forward P/E near 19.8x after a market rally. Buyers there demand a steep return for currency and policy risk.

What Factors Drive EBITDA Multiples Up or Down in Latin American Deals?

Several factors drive EBITDA multiples up or down in Latin American deals. Size, growth, recurring revenue, buyer type, and risk move the number most. Buyers test each trait during due diligence. Sellers who fix weak spots early protect their price.

What Pushes a Latin American Multiple Higher?

Several traits push a Latin American multiple higher:

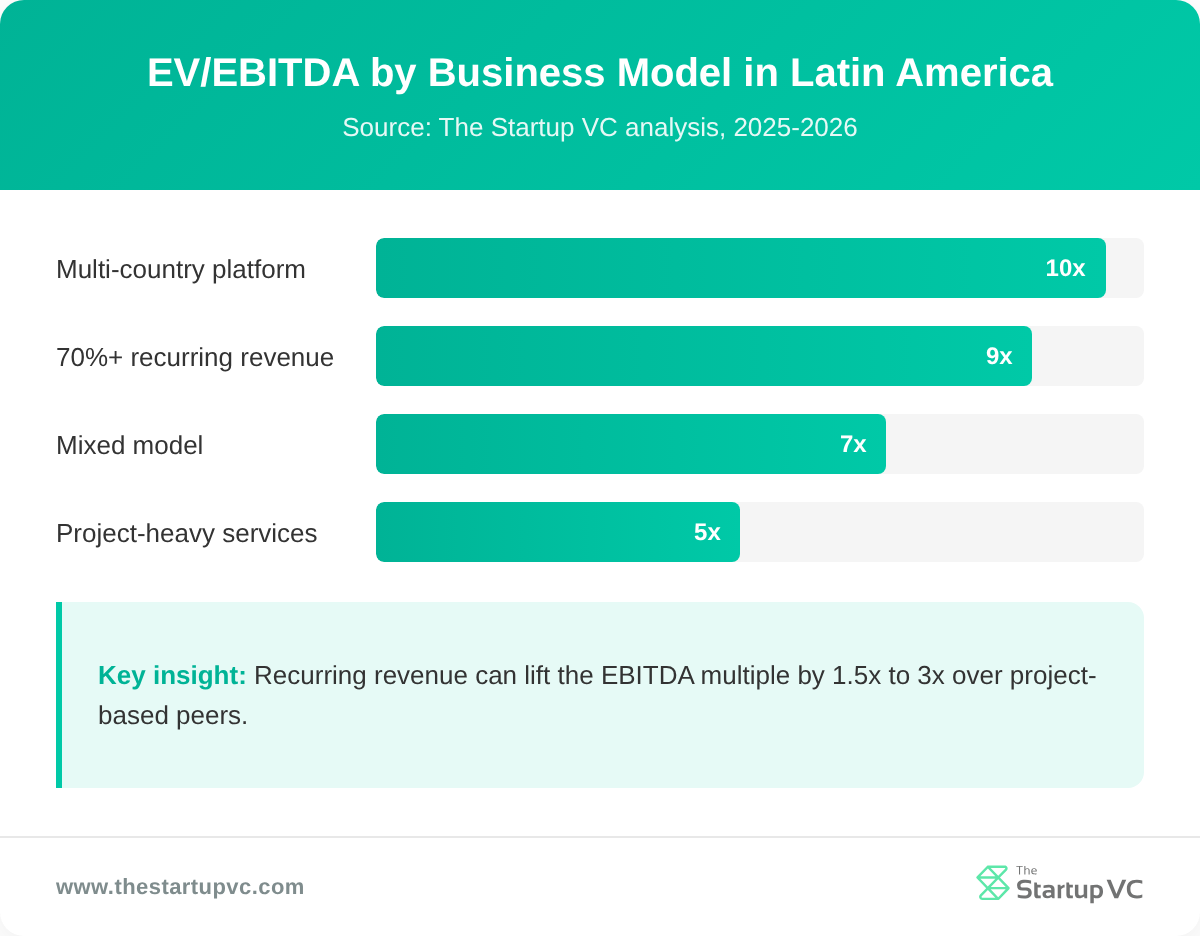

- Recurring revenue. It can lift the multiple 1.5x to 3x; firms above 70% recurring trade at 7x to 12x.

- Strong growth and margins. Clearing the Rule of 40 earns about 4.8x revenue versus 2.7x for laggards.

- Larger size. Firms near £10m EBITDA averaged 8.5x, against 3.1x for very small firms.

- Competitive buyers. Strategic buyers often pay 1 to 2 turns more for synergies.

- Clean financials. A sell-side quality-of-earnings report defends adjusted EBITDA and blocks price re-trades.

These same traits shape what backers like The Startup VC weigh in their investment focus.

What Drags a Latin American Multiple Lower?

Several risks drag a Latin American multiple lower:

- Country risk. It raises the discount rate, with premiums from 1.10% in Chile to 9.71% in Argentina.

- Currency and inflation. Local-currency earners get penalized, while dollar revenue softens the hit.

- Customer concentration. One client above 25% of sales can cut value 20% to 40%.

- Small size. Sub-$1M-EBITDA firms trade 1 to 2 turns below larger peers.

- Project-based revenue. One-off services clear just 4x to 7x without recurring contracts.

A formal valuation helps founders defend the multiple before talks begin. Each weak spot a seller fixes can add a full turn back to the price.

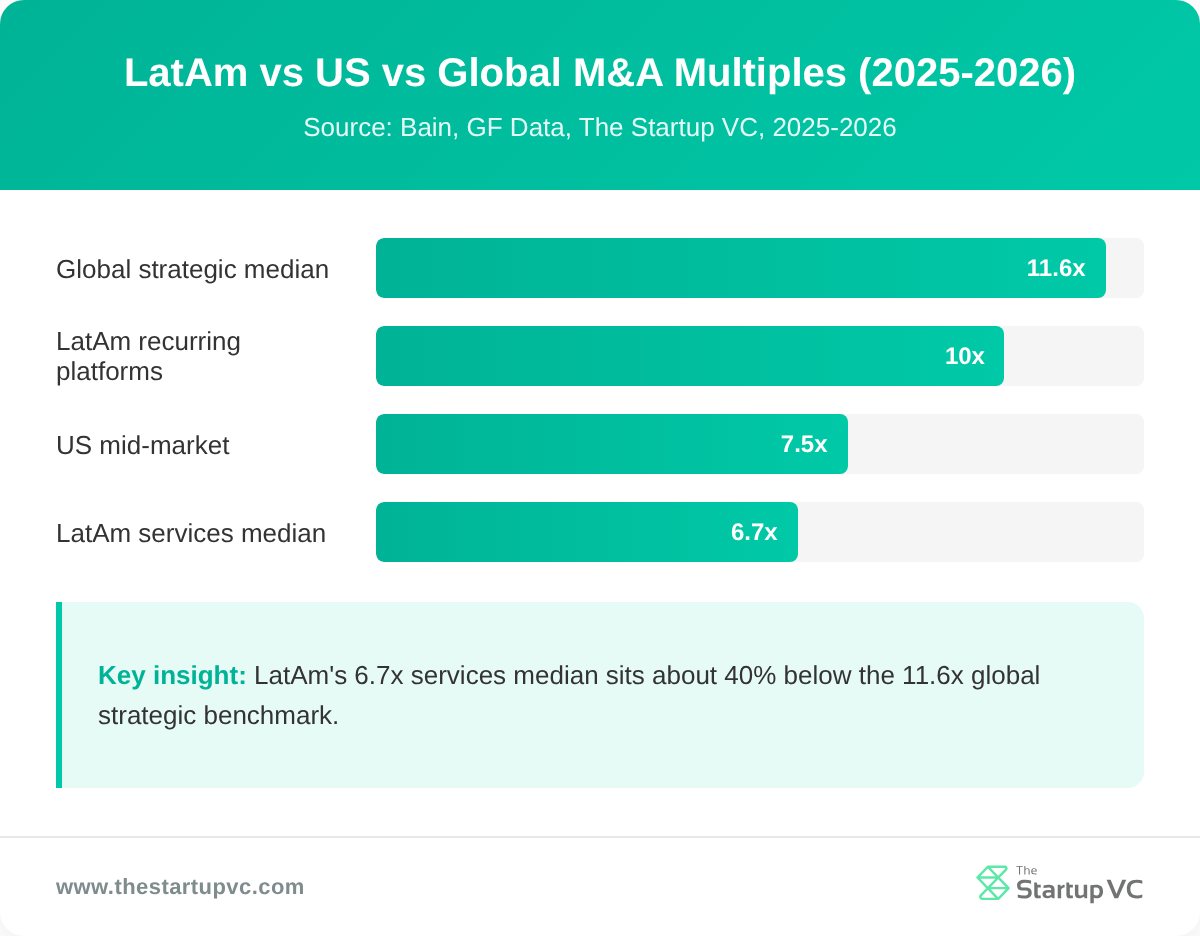

How Do Latin American EBITDA Multiples Compare to US and Global Benchmarks?

Latin American EBITDA multiples trade below US and global benchmarks. The regional services median of 6.7x sits about 40% under the global figure. The table below compares the main 2025 and 2026 benchmarks.

| Benchmark | Median EV/EBITDA | Source |

|---|---|---|

| Global strategic M&A | 11.6x | Bain |

| US private mid-market | 7.2x-7.5x | GF Data |

| Latin America services | 6.7x | Kroll |

| LatAm recurring-revenue firms | 8x-12x | Kroll / TSVC |

The gap is widest in high-multiple sectors like technology and healthcare. The discount also shapes what you can expect when you sell a company in Latin America.

US and European deals price higher across most sectors. PitchBook’s 2025 data shows IT at 13.2x and healthcare at 12.3x. Energy ran 7.9x and financial services 8.7x. The discount is even wider in public equities. US shares traded above 21x forward earnings in 2025, versus about 12x for emerging markets. Brazil alone traded more than 35% below the broad emerging-market index. Latin American multiples sit below these levels in nearly every sector.

Is the Latin American Discount Narrowing?

Yes, the Latin American discount is narrowing in several sectors. US tech multiples fell from 10.2x in 2023 to 8.1x in 2024. That move closed part of the gap with Latin American tech. Consumer retail multiples in the region rose to 9.3x in 2025, up from 6.3x. Nearshoring demand also re-rated Mexico off cheap levels. About 62% of regional leaders see strong M&A opportunities for 2026. Buyers expect the gap to keep closing as deal flow grows.

What Questions Do Dealmakers Ask Most Often About EBITDA Multiples in Latin America?

What Is a Good EBITDA Multiple for a Latin American Company?

A good EBITDA multiple for a Latin American company usually falls between 4x and 12x. Sector and business model set the level. Recurring revenue can add 1.5x to 3x. A services firm near 6x to 7x is typical for the region. Buyers also weigh size, growth, and country risk before settling on a number.

Do Smaller Companies Sell for Lower Multiples?

Yes, smaller companies sell for lower multiples. GF Data’s size premium widened to 2.8x in 2025. Deals worth $10 million to $25 million averaged about 5.9x to 6.7x. Larger platforms worth $100 million reached about 9.2x.

How Do You Normalize EBITDA Before Applying a Multiple?

You normalize EBITDA by adjusting owner-related and one-off costs. Add back owner pay above a market-rate salary. Include the related payroll taxes and benefits. Each added dollar flows straight into enterprise value.

Why Are Latin American Multiples Lower Than US Multiples?

Latin American multiples are lower than US multiples because of higher risk. A country risk premium near 3.5% raises the discount rate. Currency swings, inflation, and thin liquidity add more. This pushes the cost of equity to 10% to 15%.

Should You Use Revenue or EBITDA Multiples for a Tech Startup?

You should use revenue multiples when growth is high or EBITDA is negative. SaaS firms fetch about 3x to 6x ARR under $5 million ARR. That can reach 8x to 15x above $25 million ARR. Switch to EBITDA multiples once margins stabilize.

How Fast Are Latin American Multiples Changing in 2026?

Latin American multiples are changing quickly in 2026. Regional deal value rose 19% in 2025. US mid-market multiples jumped from 6.9x to 7.5x in one quarter. Global strategic multiples held flat at 11.6x even as deal value surged. Nearshoring and lower US rates point to firmer multiples ahead.

Ready to Value or Sell Your Latin American Company?

The Startup VC helps founders turn these benchmarks into real deal outcomes. It is Craig Dempsey’s family office and company builder. The team creates, backs, and guides scalable ventures across Latin America. Portfolio companies like Biz Latin Hub operate in 17 countries. You get hands-on help with valuation, deal structure, and buyer outreach. We also help buyers screen targets and run due diligence across the region. Our experience spans dozens of Latin American transactions. Contact us today to benchmark your company and plan your next move.