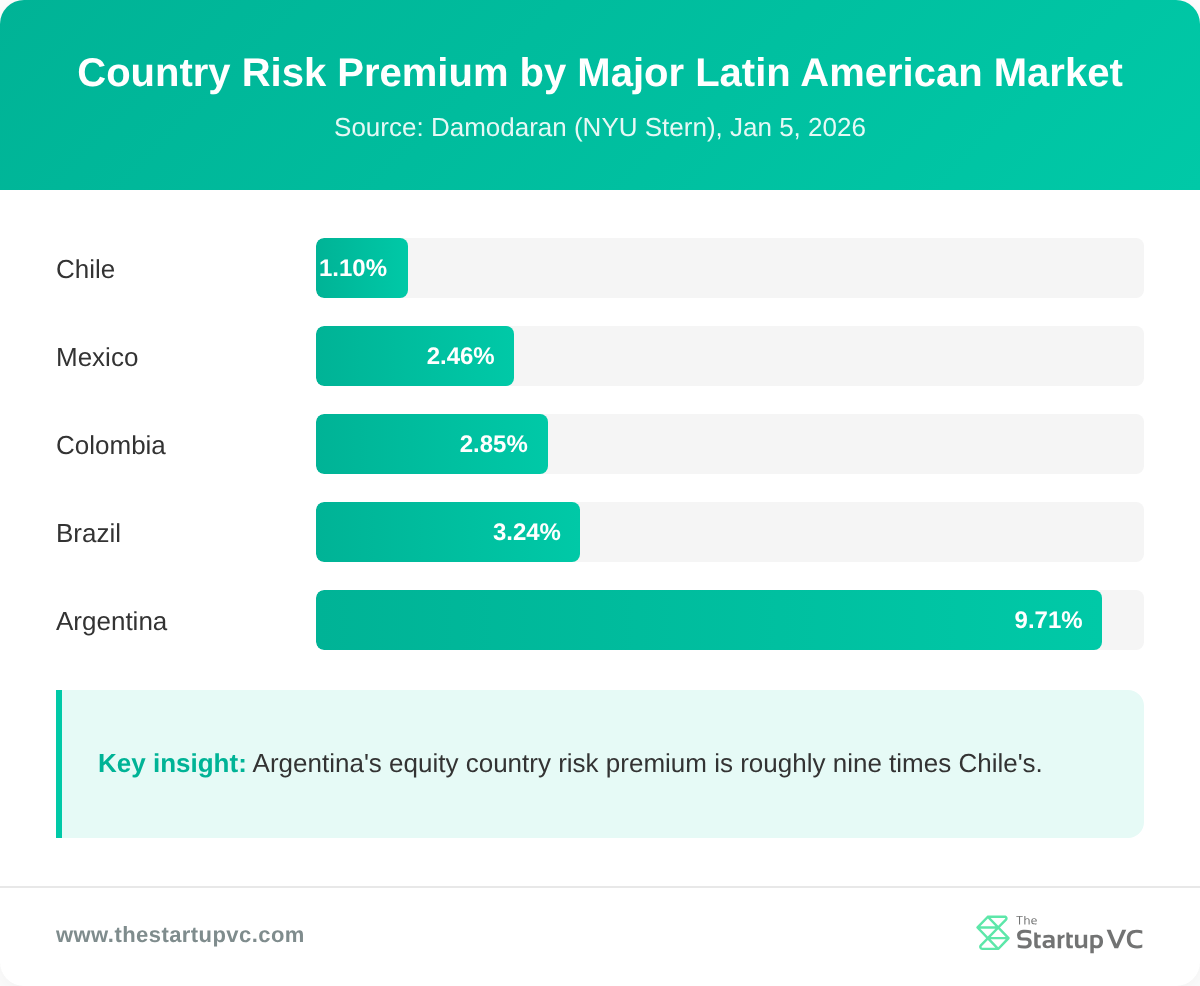

Country risk premiums add 1.1% to 9.7% to LatAm equity returns, above the US base of 4.23%.

Damodaran’s January 2026 data sets the US base equity risk premium at 4.23%. Country risk premiums then range from 1.10% in Chile to 9.71% in Argentina. Brazil adds 3.24%, Mexico 2.46%, and Colombia 2.85% to the cost of equity.

The Startup VC builds and backs ventures across Latin America, where small rate changes swing a valuation by millions. This guide explains the Damodaran method, per-country premiums, and how each one feeds a DCF discount rate. You will also see why Chile and Argentina sit at opposite ends of the risk scale.

What Is a Country Risk Premium and Why Does It Matter for Valuation?

A country risk premium is the extra equity return investors demand for a riskier market than the United States. It pays investors for risks beyond a single company’s results. These risks sit at the country level, not the company level.

The premium covers several country-level risks at once:

- Political risk. Elections, policy swings, and unrest can hit company cash flows.

- Currency risk. A falling local currency can erase dollar returns.

- Regulatory risk. New rules or taxes can break a business model.

- Macroeconomic risk. High inflation or slow growth raises broad uncertainty.

Analysts build an emerging market’s total equity risk premium from two parts:

- US base premium. Damodaran set this mature-market anchor at 4.23% in January 2026.

- Country risk premium. This is the extra slice added for a market like Brazil or Chile.

The premium matters because it raises the discount rate used in a valuation. A higher discount rate lowers the present value of future cash flows. So the same Latin American business is worth less than an identical US one. Damodaran’s 2025 base premium came from a 4.48% implied US premium minus a 0.27% US default spread.

How Do You Calculate the Country Risk Premium for Latin American Markets?

You can calculate the country risk premium by scaling a sovereign default spread up for equity risk. Damodaran’s method runs in three clear steps:

- Find the sovereign default spread. Start with the country’s Moody’s rating, then read its default spread. A Baa2 rating maps to about a 2.07% spread.

- Scale up for equity volatility. Multiply the default spread by the ratio of equity to bond volatility. This multiplier runs near 1.4 to 1.5.

- Add it to the base premium. Combine the country risk premium with the 4.23% US base premium.

The core formula is short: CRP = default spread x relative equity volatility. Relative volatility divides a market’s equity swings by its bond swings. Damodaran sets one global multiplier near 1.42 from emerging-market index data.

Sovereign ratings map directly to default spreads. Lower ratings carry much wider spreads:

| Moody’s rating | Example grade | Default spread |

|---|---|---|

| Baa2 | BBB | ~2.07% |

| Ba1 | BB+ | ~2.73% |

| B2 | B | ~5.99% |

Some analysts use a sovereign CDS spread instead of the rating-based spread. A CDS spread is the yearly cost to insure against a default, quoted in basis points. One basis point equals 0.01%.

CDS spreads move daily with the market. They can flag rising risk faster than a slow ratings change. Damodaran draws his volatility multiplier from the S&P emerging-market equity index. He compares it against an iShares emerging-market government bond ETF.

What Are the Country Risk Premiums for Major Latin American Markets?

The country risk premiums for major Latin American markets range from 1.10% in Chile to 9.71% in Argentina. These figures come from Damodaran’s dataset, updated on January 5, 2026. Each premium sits on top of the 4.23% US base. Investment-grade markets like Chile and Peru sit well below speculative Brazil and distressed Argentina.

The table below shows the Moody’s rating, country risk premium, and total equity risk premium for each market:

| Country | Moody’s rating | Country risk premium | Total equity risk premium |

|---|---|---|---|

| Chile | A2 | 1.10% | 5.33% |

| Peru | Baa1 | 2.07% | 6.30% |

| Mexico | Baa2 | 2.46% | 6.69% |

| Colombia | Baa3 | 2.85% | 7.08% |

| Brazil | Ba1 | 3.24% | 7.47% |

| Argentina | Caa1 | 9.71% | 13.94% |

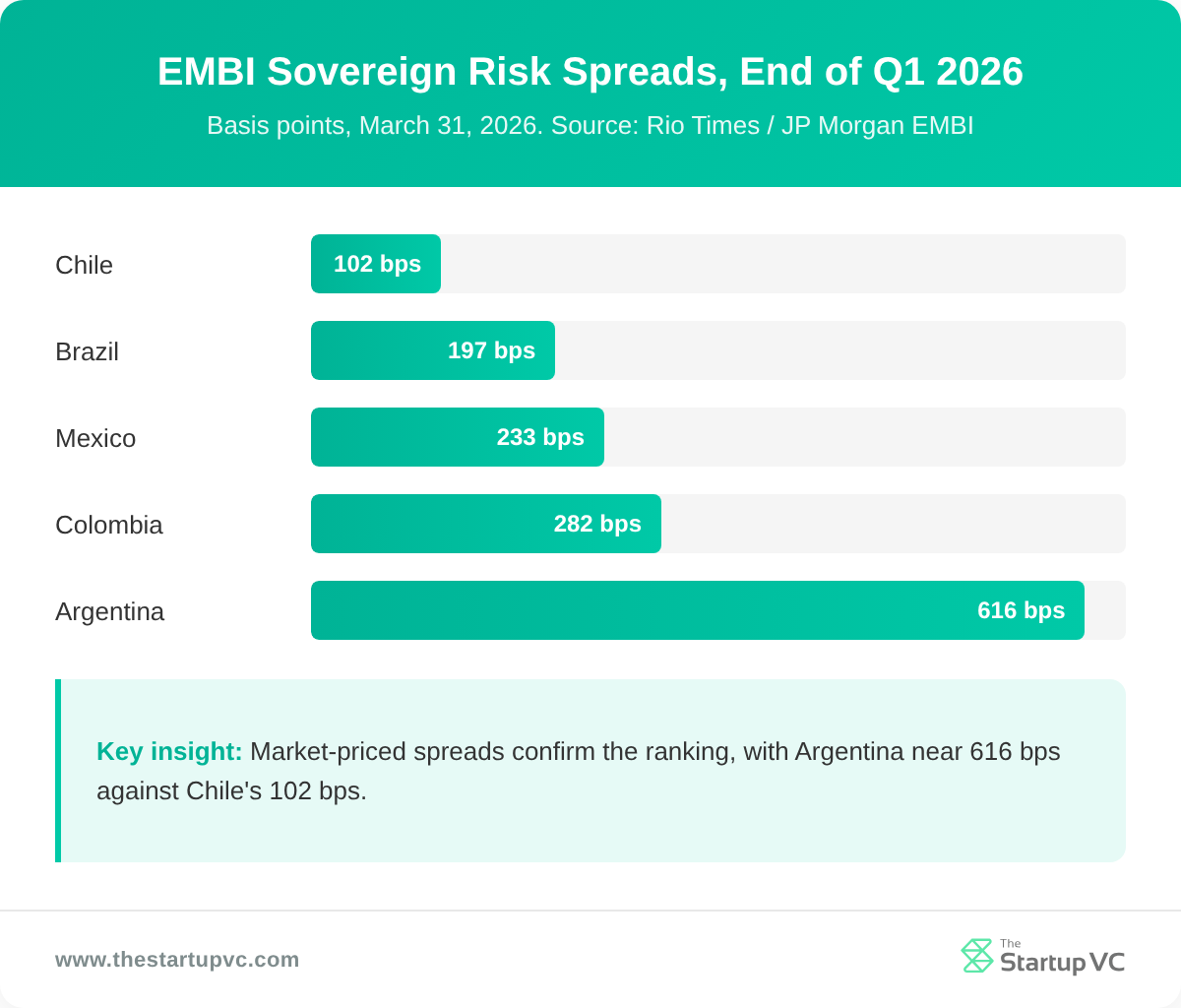

Chile holds the lowest premium and the only single-A rating in the group. Argentina sits far above the rest after years of default and high inflation. Moody’s upgraded Argentina to Caa1 from Caa3 on July 17, 2025. Market spreads tell the same story. End-Q1 2026 EMBI spreads ran from 102 basis points for Chile to 616 for Argentina. These same markets also set EBITDA multiples in Latin American M&A.

S&P’s foreign-currency ratings track the same order. It marks Chile at A, Mexico at BBB, Colombia at BB-, and Argentina at B-. Uruguay and Panama round out the region’s investment-grade names, with premiums near 2.07% and 2.85%.

How Does the Country Risk Premium Feed Into the Discount Rate and DCF?

The country risk premium feeds into the discount rate by raising a company’s cost of equity. A higher cost of equity lifts the WACC and lowers the DCF value. Most LatAm valuations use US-dollar cash flows and a US Treasury risk-free rate. The country premium then captures the extra market risk. This is the core LatAm discount rate adjustment. Learn more about how to value a company in Latin America at The Startup VC.

How Does the Premium Raise the Cost of Equity?

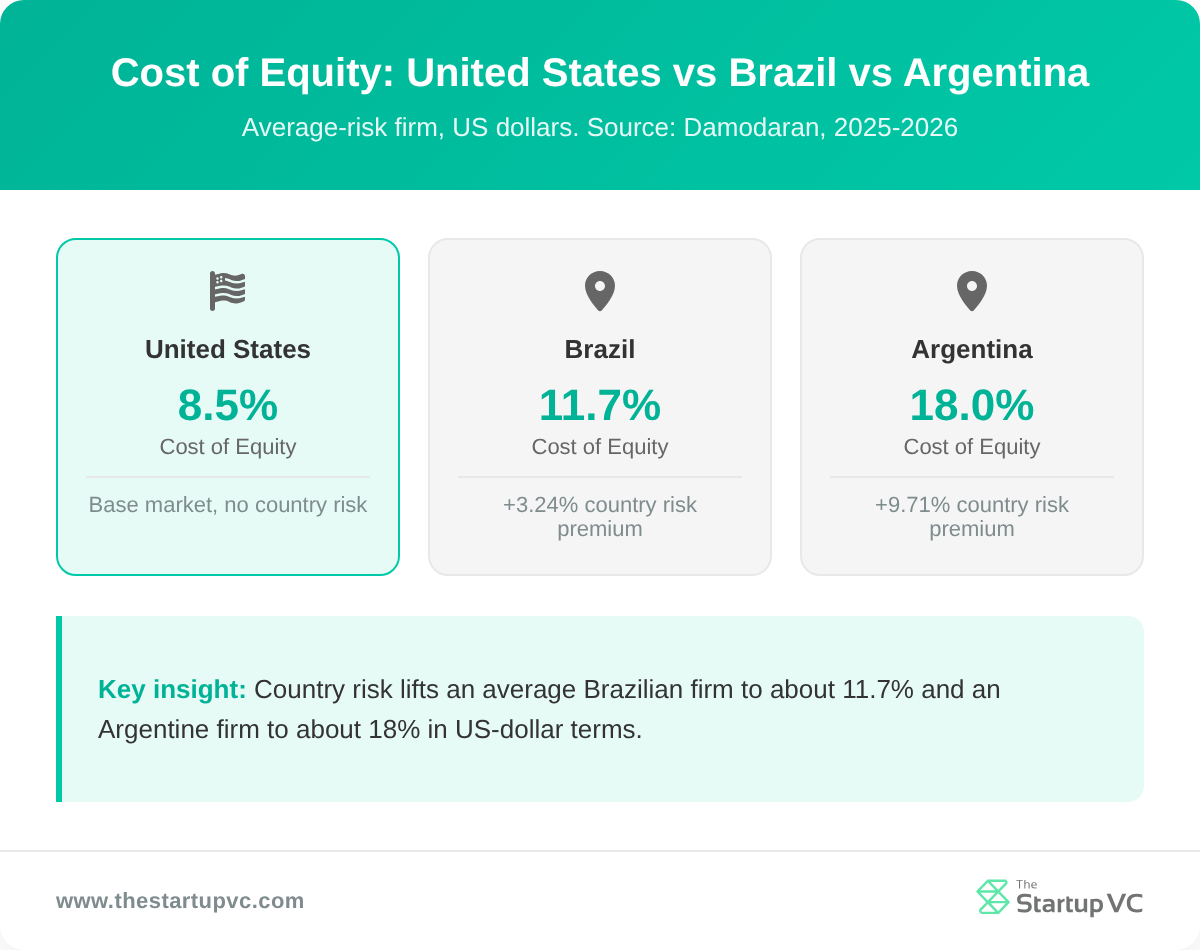

The premium raises the cost of equity by adding a country term to the CAPM. The formula reads: Cost of Equity = Risk-Free Rate + Beta x Mature ERP + Country Risk Premium. A same-beta Brazilian firm pays about 3.24 points more than its US peer.

The table below shows the cost of equity for an average-risk firm by market:

| Market | Total equity risk premium | Approx. cost of equity (USD) |

|---|---|---|

| United States | 4.23% | ~8.5% |

| Brazil | 7.47% | ~11.7% |

| Argentina | 13.94% | ~18% |

These US-dollar figures use Damodaran’s mid-2025 base of 8.45% for an average US firm.

The cost of equity also flows into the WACC. A firm funded mostly by equity feels the full premium. The same forecast then discounts at a higher rate, so the present value drops.

What Are the Three Ways to Add Country Risk to the Discount Rate?

The three ways to add country risk are the equal, beta, and lambda approaches. Damodaran lays out each one:

- Equal approach. Add the full premium to every company in the country. Formula: Rf + CRP + Beta x Mature ERP.

- Beta approach. Scale the premium through beta. Formula: Rf + Beta x (Mature ERP + CRP).

- Lambda approach. Weight the premium by a company’s local exposure. Formula: Rf + Beta x Mature ERP + Lambda x CRP.

Lambda sharpens the DCF country adjustment for exporters. A Brazilian firm earning most revenue in the US gets a smaller premium. A purely domestic firm carries the full load. Damodaran estimates lambda from a firm’s share of local revenue. A lambda of 1 means average exposure to country risk.

Why Do Country Risk Premiums Vary So Much Across Latin America?

Country risk premiums vary across Latin America because sovereign ratings, inflation, and default history differ sharply. Four main drivers set each market apart:

- Sovereign ratings. Chile is single-A, while Argentina sits deep in junk near default.

- Market spreads. End-Q1 2026 EMBI spreads ran from 102 bps in Chile to 616 in Argentina.

- Inflation. Argentina averaged about 219.9% in 2024, against 4.3% in Chile and 2.4% in Peru.

- Default history. Argentina has defaulted nine times since 1816. Chile has avoided modern default.

Raw sovereign default spreads fan out the same way. They run from 0.72% for Chile and 1.36% for Peru to 6.37% for Argentina.

Policy shifts move these premiums in real time. S&P raised Argentina to CCC+ in December 2025 under President Milei’s adjustment plan. Brazil and Colombia stay pressured by high fiscal deficits and rising debt. So the regional gap can widen or narrow within a single year. These shifts keep the country risk premium in constant motion. See how The Startup VC sets its investment focus across the region.

What Questions Do Analysts Ask Most Often About Latin American Country Risk Premiums?

Where Does the Country Risk Premium Data Come From?

Most analysts use Aswath Damodaran’s free dataset at NYU Stern. He updates the country risk premiums each January and July. The January 2026 version uses a 4.23% US base premium.

Should You Use CDS Spreads or Credit Ratings?

You should pick the source that fits your data. Ratings give a stable, rating-based default spread. CDS spreads react faster but partly reflect liquidity, not pure default risk.

Does the Country Risk Premium Apply to Private Companies?

Yes, the premium applies to private companies too. You add it to the cost of equity in any DCF. A purely domestic firm carries the full country load.

How Does Currency Affect the Country Risk Premium?

Currency affects the valuation by setting the risk-free rate base. A US-dollar valuation uses a US Treasury rate. The country risk premium then sits on top in dollar terms.

Which Latin American Market Has the Lowest Country Risk Premium?

Chile has the lowest country risk premium in the region. It sits at 1.10% in the January 2026 data. Its A2 rating and low inflation drive that result.

How Often Should You Update the Premium?

You should update the premium at least twice a year. Damodaran refreshes his data each January and July. A ratings change or a crisis can force an earlier update.

Ready to Value Your Latin American Business?

A precise country risk premium can change your valuation by millions. The Startup VC is Craig Dempsey’s family office and company builder in Latin America. We create, back, and guide scalable ventures across the region. Our team pairs real operating experience with disciplined valuation work. We help founders and investors price risk in Brazil, Mexico, Chile, and beyond. Contact us today to value your next Latin American venture.