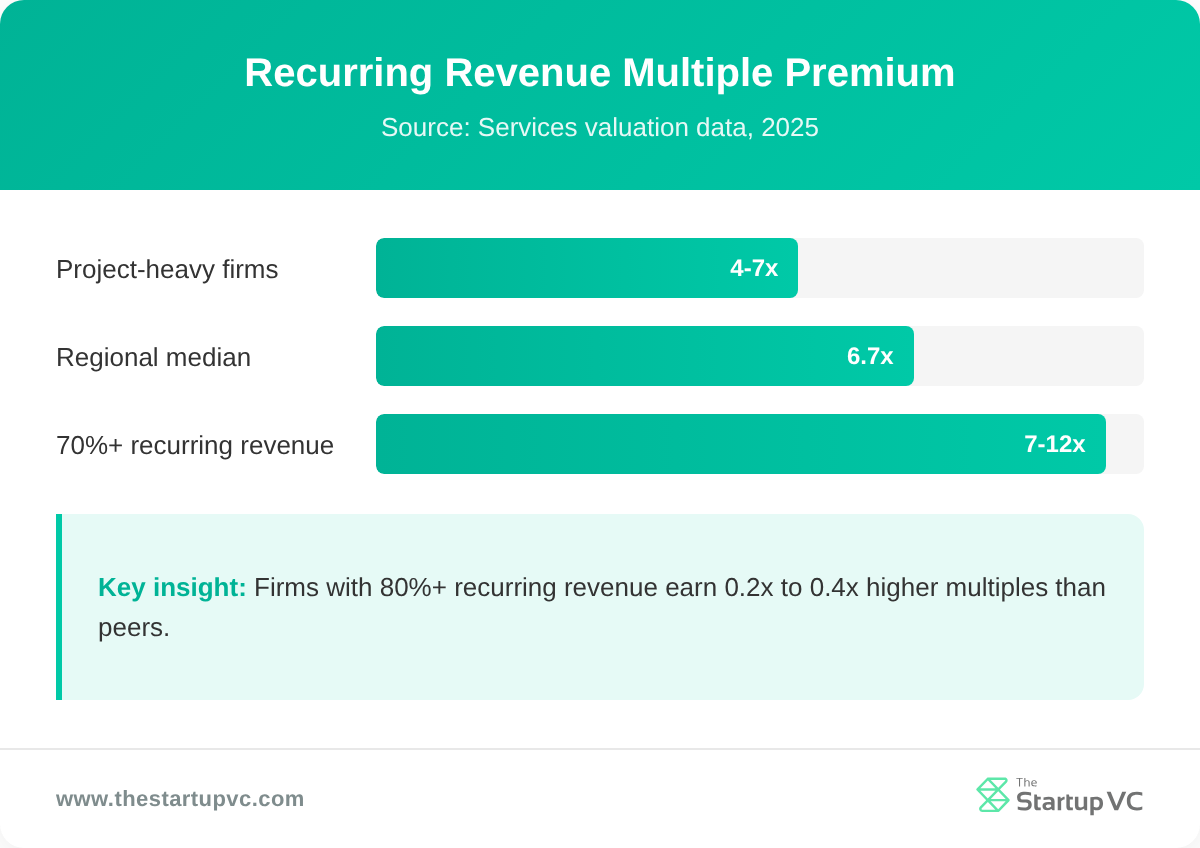

Tax advisory firms in Latin America trade at 8x to 12x EBITDA when recurring revenue tops 70%, above the 6.7x regional median.

Buyers acquire a tax advisory firm in Latin America by valuing recurring compliance revenue, structuring partner rollover equity of 5% to 20%, and managing client concentration below 15%. Latin America recorded 2,650 M&A deals worth US$96 billion in 2025.

The Startup VC builds and backs B2B service ventures across Latin America, drawing on Biz Latin Hub’s accounting and tax footprint in 17 countries. Biz Latin Hub exited to Vistra in December 2025. Below, you will find valuation methods, partner economics, ownership rules, concentration risk, and cross-border integration steps for a tax practice roll-up.

Why Are Tax Advisory Firms Strong Roll-Up Targets in Latin America?

Tax advisory firms are strong roll-up targets because they produce recurring, predictable revenue with margins above industrial sectors. Compliance work repeats every month and every tax season. This makes cash flows easy to forecast and finance.

Roll-up buyers favor tax practices for four reasons:

- Recurring revenue. Monthly filings and annual returns renew without new sales effort.

- High retention. Top firms keep 95% or more of clients each year.

- Margin strength. Service margins beat industrial sectors across Latin America.

- Scale premium. Multi-country platforms trade at 8x to 12x EBITDA, above the 6.7x median.

Latin America recorded 2,650 M&A deals worth US$96 billion in 2025. That total rose 13% over 2024. Tax and accounting practices sit inside a busy professional services deal market. For a wider view of the sector, see our overview of the B2B services sector in Latin America.

Biz Latin Hub shows the model. It built accounting and tax advisory offices across 17 countries, then exited to Vistra in December 2025. A roll-up turns many small books into one regional platform.

How Do You Value a Tax Advisory Firm in Latin America?

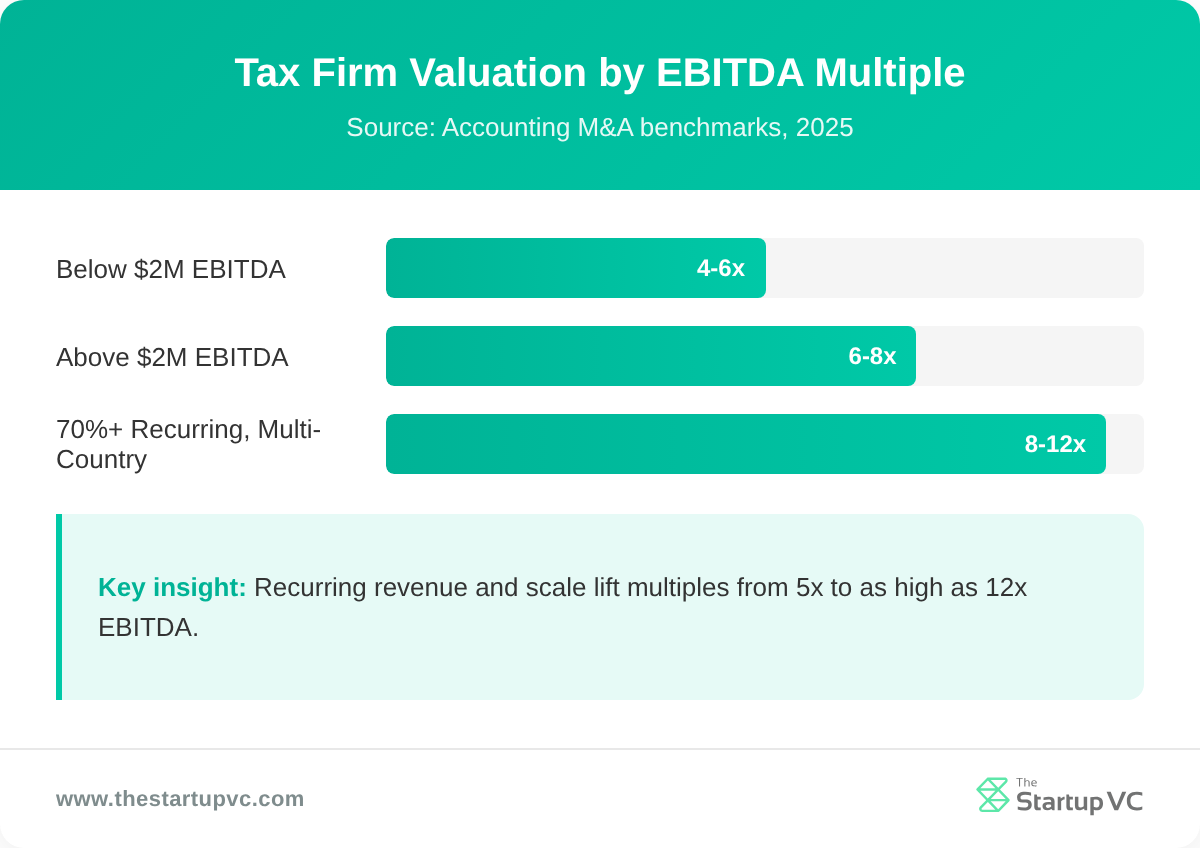

You value a tax advisory firm by applying an EBITDA multiple to normalized earnings. Most firms with $2M to $10M in revenue value at 3.0x to 5.5x adjusted EBITDA in 2025. Recurring revenue and low client concentration push the multiple higher.

First, you must normalize EBITDA. Replace the owner’s pay with a market-rate salary before you apply any multiple. This shows the true profit a buyer inherits.

A simple rule of thumb guides the EBITDA multiple by firm size:

| Firm EBITDA | Typical EBITDA Multiple |

|---|---|

| Below $2M | 4x to 6x |

| Above $2M | 6x to 8x |

| 70%+ recurring, multi-country | 8x to 12x |

Revenue multiples offer a quick cross-check. They range from 0.7x to 1.1x of annual revenue. Sticky compliance books reach 1.2x to 1.3x. Firms with 80% or more recurring revenue earn 0.2x to 0.4x higher multiples than project-based peers.

For deeper valuation methods, see our guide on how to increase the valuation of a services company in Latin America.

How Do Partner Economics Work When You Buy a Tax Practice?

Partner economics work by combining upfront cash, rollover equity, and earnouts that keep senior advisors aligned. Rollover equity typically runs 5% to 20% of the purchase price. This makes departing partners co-owners of the new platform.

Rollover equity matters most in a people business. Clients follow trusted advisors, not logos. Keeping partners invested protects the revenue you just bought.

Earnouts add a second retention layer. Most earnout agreements span one to three years and tie payments to performance metrics. They bridge price gaps and reduce key person risk.

Buyers structure partner vesting in three common ways:

- Cliff vesting. No equity vests until a set date, then it vests in full.

- Graded vesting. Equity vests in steps over several years.

- Milestone vesting. Vesting tracks revenue or retention targets.

Each structure rewards partners for staying and for protecting client relationships. The goal is a smooth handoff, not a quick exit.

What Regulated Ownership Rules Apply to Tax Practices in Latin America?

Regulated ownership rules vary by country, and most require licensed local professionals to sign regulated work. You can own the firm as an investor. A registered local accountant must still hold the professional credential for audits and tax filings.

Mexico and Brazil show how the rules differ:

| Country | Key Ownership Rule |

|---|---|

| Mexico | CPC credential needed; only IMCP members audit public interest firms |

| Mexico | Tax auditors register with the Federal General Administration of Tax Audit |

| Brazil | Non-resident partners appoint a resident administrator and legal representative |

| Brazil | Strict ultimate beneficial ownership rules apply to foreign owners |

In Mexico, the Contador Publico Certificado, or CPC, is the local CPA equivalent. Only registered members can sign regulated audits. In Brazil, foreign owners must name local representatives and disclose ultimate ownership.

Biz Latin Hub built wholly-owned offices across 17 countries using local entity formation and legal representation. You should map each country’s license rules before you sign. A clean ownership structure avoids regulatory delays after closing.

How Do You Manage Client Concentration Risk in a Tax Services M&A Deal?

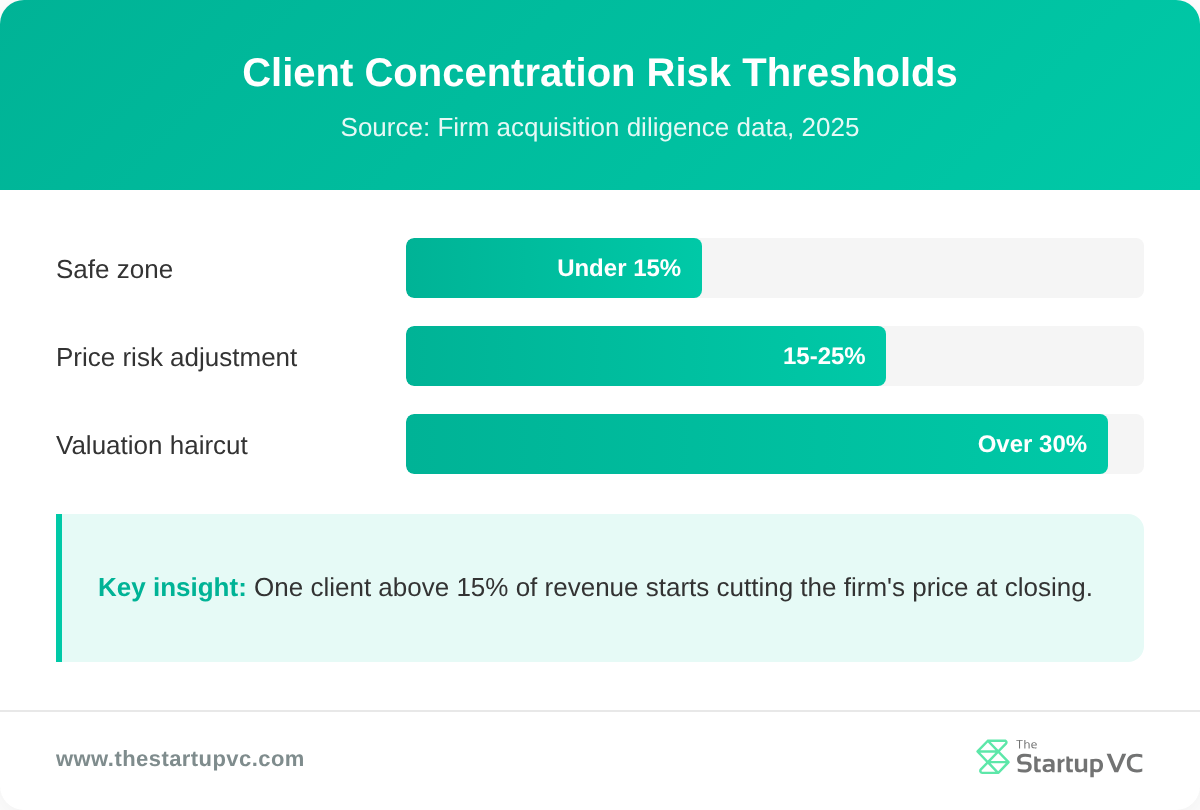

You manage client concentration risk by checking the revenue share of top clients and structuring the deal to protect against loss. No single client should exceed 15% of revenue. The top 10 clients combined should stay under 40%.

Concentration is the single biggest reason buyers cut a firm’s valuation. One dominant client makes future cash flows harder to trust. Diligence must surface this early.

Use clear thresholds to flag risk during due diligence:

- Above 15% from one client. Risk adjustment begins on price.

- Above 25% to 30% from one client. Expect a valuation haircut or deal restructure.

- Top 5 clients above 25% of revenue. A red flag needing investigation.

The cost is real. A $2M firm with a clean book gets $400K to $600K more cash at closing than an identical firm with concentration risk. You can lower this risk with earnouts tied to client retention. The buy-side steps mirror those in our acquirer’s M&A playbook for buying a company in Latin America.

How Do You Integrate a Cross-Border Tax Practice After Acquisition?

You integrate a cross-border tax practice by sequencing systems, staff, and branding in stages rather than all at once. A “crawl-walk-run” rollout starts with data integration. Then come calculation engines, then reporting dashboards.

Systems integration carries the most risk. Disjointed ERP and accounting tools delay consolidation and cause statement errors. You must harmonize accounting policies and align transfer pricing documents across countries.

Plan integration across four work streams:

- Technology. Roll out modules in order, starting with shared data.

- Staff. Use pilot programs, short training, and “tax tech champions” to drive adoption.

- Compliance. Align transfer pricing and manage intercompany financing.

- Branding. Phase the name change so clients keep their trusted contacts.

Biz Latin Hub coordinates multi-jurisdictional support with bilingual teams across 17 countries. That regional bench shows how a platform serves clients in many tax systems at once. Steady integration protects the recurring revenue that justified the deal.

What Questions Do Buyers Ask Most Often About Acquiring a Tax Advisory Firm in Latin America?

How Much Does It Cost to Buy a Tax Advisory Firm in Latin America?

Tax advisory firms cost 3x to 8x EBITDA, depending on size and recurring revenue. Firms with 70% or more recurring revenue reach 8x to 12x EBITDA. Revenue multiples run 0.7x to 1.3x of annual sales.

How Long Does a Tax Firm Acquisition Take?

A tax firm acquisition usually takes three to six months from offer to close. Diligence, regulatory checks, and partner negotiations drive the timeline. Earnout periods then run one to three years after closing.

What Advisor Fees Apply to a LatAm Tax Practice Deal?

Advisor fees apply at 3% to 8% of transaction value on mid-market Latin American deals. Smaller deals carry higher percentage fees. You can review more pricing detail in our guide on how to increase the valuation of a services company.

How Do You Finance a Tax Firm Acquisition?

You finance a tax firm acquisition by mixing cash, seller rollover equity, and debt. Rollover equity covers 5% to 20% of the price. Lenders favor the predictable cash flows of recurring compliance work.

What Is the Biggest Risk When Buying a Tax Practice?

The biggest risk is client concentration, which buyers treat as a valuation cut. One client above 15% of revenue starts a price adjustment. Earnouts tied to retention reduce this risk.

How Do You Keep Partners After the Deal?

You keep partners by giving rollover equity and earnouts tied to performance. Most earnouts last one to three years. This aligns senior advisors with the new platform’s growth.

Ready to Acquire a Tax Advisory Firm in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder. We create, back, and guide scalable ventures across Latin America. Our team brings hands-on operating experience from Biz Latin Hub, which served clients in 17 countries before its 2025 exit.

We help buyers source targets, value recurring revenue, and integrate tax practices into a regional platform. See where we invest on our investment focus page. Contact us today to plan your tax advisory roll-up.