Latin America’s legal services market is consolidating fast, with the regional ALSP sector worth USD 81.4 billion in 2024 and growing toward USD 131 billion by 2033.

Buyers acquire legal services companies in Latin America through ALSP purchases or MSO structures, not direct law firm ownership. Lawyer-only rules in Brazil, Mexico, and Chile block non-lawyer equity, so investors buy the business layer while licensed lawyers keep the practice.

The Startup VC builds and backs B2B service companies across Latin America, including Biz Latin Hub in 17 countries. This guide covers the ownership rules, ALSP and MSO structures, licensing portability, and the steps to close a legal services deal in the region.

What Does It Mean to Acquire a Legal Services Company in Latin America?

Acquiring a legal services company in Latin America means buying a business that delivers legal work without owning the regulated law practice. You can buy an alternative legal service provider (ALSP) outright. You cannot directly own a bar-licensed law firm.

The regional ALSP market generated USD 81.4 billion in revenue in 2024. It is projected to grow at a 5.4% yearly rate through 2033. By 2033, it should reach USD 131.3 billion. Latin America held about 7.7% of the global ALSP market in 2024.

An ALSP handles work like compliance, contract review, and document services. It is not a traditional bar-licensed law firm. That difference matters for buyers. A law firm gains legal status only after it registers with the local bar. The regulated practice and the acquirable service business are separate things.

This makes legal services part of the broader B2B roll-up trend. Buyers consolidating professional services often start here. For the wider picture, see our overview of the B2B services sector in Latin America.

Why Is Legal Services Consolidation Active in Latin America?

Legal services consolidation is active in Latin America because the market is large, fragmented, and attracting fresh capital. Brazil leads the trend. Its ALSP market is projected to grow from USD 836 million in 2024 toward USD 16.7 billion by 2032.

Brazil M&A deal volume rose 40% in the first half of 2025 versus 2024. Brazil made up the majority of all Latin American deals. Recent activity is led by domestic consolidations. Large players in retail, healthcare, and energy set the pattern. That pattern now reaches professional services.

Several signals point to an active legal roll-up market:

- Firm-level mergers. Madrona Advogados partnered with Coelho & Dalle across Recife, Fortaleza, and Sao Paulo.

- Capital inflows. US investment firm Accel-KKR backed Chilean legaltech LemonTech.

- Repeatable deal structures. About a dozen MSO legal deals closed in 2025, moving from experimental to financeable platforms.

These buyers follow the same playbook used in other sectors. The approach mirrors any acquisition of a company in Latin America, with legal-specific rules layered on top.

What Regulatory Constraints Limit Law Firm Ownership in Latin America?

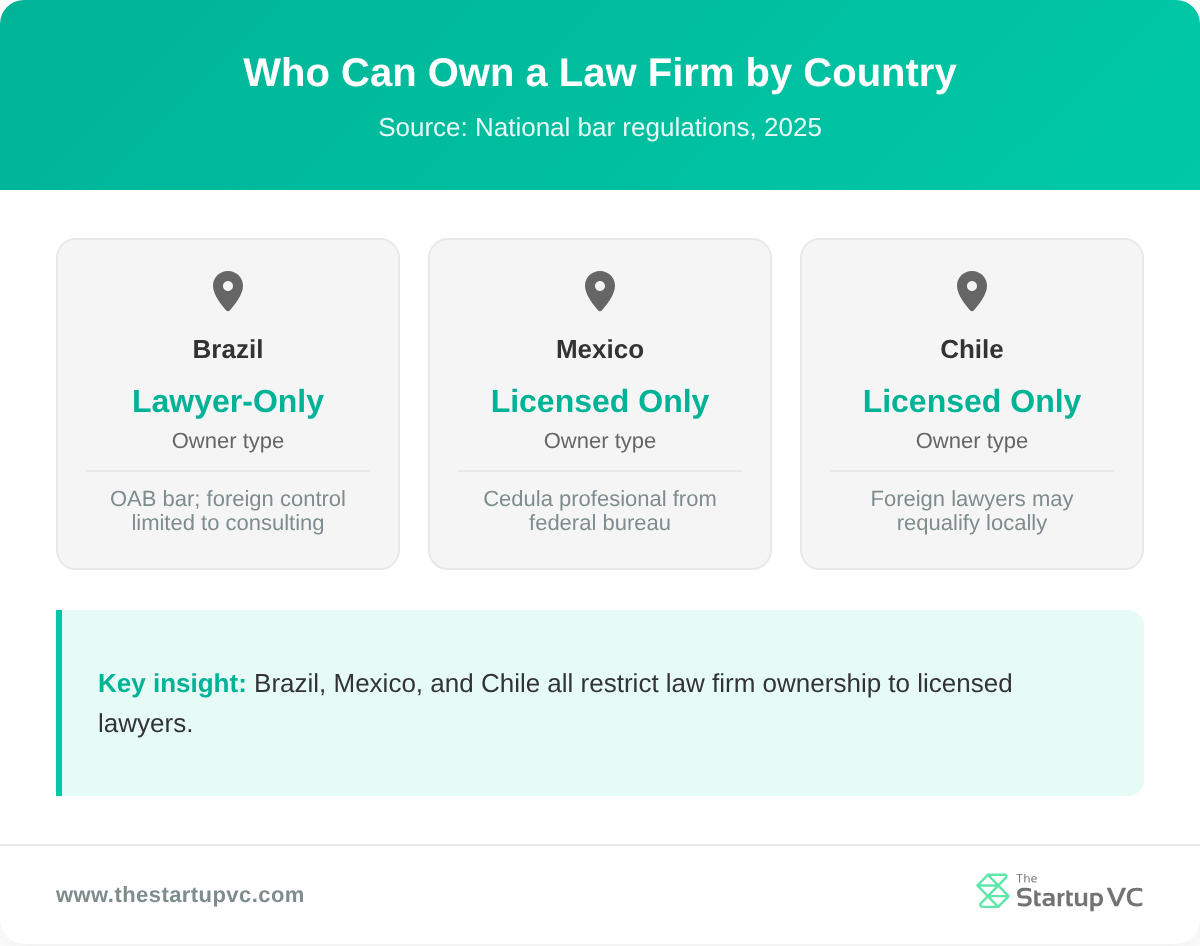

Regulatory constraints limit law firm ownership in Latin America by requiring that only licensed lawyers own the practice. Non-lawyer equity in a law firm is generally banned. This shapes every deal structure in the region.

In Brazil, Law 8.906/94 lets lawyers form only a partnership or a sole proprietorship. The firm must register with the local bar, the OAB. A law firm registers with the bar, not a corporate board. So ownership transfers follow professional rules, not standard company law.

Brazil also restricts foreign control directly. OAB Provimento 91/2000 treats a firm with shares controlled by non-Brazilians as a foreign firm. Its lawyers may act only as legal consultants. They cannot litigate or practice Brazilian law. This pushes foreign buyers toward cooperation agreements instead of mergers.

Ownership rules vary by country, but the lawyer-only principle is consistent:

| Country | Ownership rule | License authority |

|---|---|---|

| Brazil | Lawyer-only; foreign control limited to consulting | OAB (local bar) |

| Mexico | Licensed professionals only; no bar exam | General Professions Bureau |

| Chile | Licensed lawyers; requalification possible | Ministry of Foreign Affairs |

| Colombia | Local admission; foreign requalification allowed | National judicial authority |

The US default rule, ABA Model Rule 5.4, bars non-lawyers from owning law firms. Most of Latin America follows the same lawyer-only ownership principle.

How Do You Structure the Acquisition of a Legal Services Company?

You can structure the acquisition of a legal services company by buying an ALSP directly or by using a management services organization (MSO). Both let investors capture value without owning the regulated practice.

The simplest path is an ALSP purchase. An ALSP that does not practice law can be bought outright by non-lawyer investors. There is no bar restriction to work around. This is the cleanest structure for a legal services acquisition in Latin America.

The MSO model handles cases where a licensed practice is involved. It splits the firm into two entities:

- Core law firm. Lawyer-owned, practices law, and receives legal fees.

- MSO. Investor-owned, holds the business infrastructure.

The MSO absorbs technology, marketing, finance, real estate, HR, and staffing. It often holds the intellectual property and the firm name. It licenses these back to the law firm under a long-term management services agreement. The MSO earns a management fee. Professional rules prohibit setting that fee as a percentage of legal revenue or profit.

Alternative business structures (ABS) allow direct equity in a firm. They work only in limited jurisdictions. MSOs keep the two layers separate and work across the region. For buyers comparing deal models, the MSO route fits Latin America’s lawyer-only rules best.

How Does Licensing Portability Affect a Legal Services Acquisition?

Licensing portability affects a legal services acquisition by setting where lawyers can work and how revenue moves across borders. Bar admission is country-specific. A license held in one Latin American market does not automatically transfer to another.

Some markets make internal expansion easy. In Mexico, the cedula profesional from the federal General Professions Bureau lets a lawyer practice across the entire country. That single license supports multi-state growth without extra admissions.

Cross-border portability is harder, but several paths exist:

- Mexico. A federal cedula profesional covers the whole country.

- Colombia. Foreign lawyers can requalify as local lawyers and act as counsel or arbitrators in international arbitration.

- Chile. Foreign lawyers can requalify with a recognized degree, local residence, and a six-month internship at Corporacion de Asistencia Judicial.

- Brazil. OAB registration is mandatory before any lawyer can practice or litigate.

Foreign lawyers can usually advise on international arbitration or home-country law without full local admission. This portable revenue line is something buyers can value directly. Portability shapes both deal price and post-deal integration.

What Are the Main Steps to Buy a Legal Services Company in Latin America?

You can buy a legal services company in Latin America by following five core steps: target screening, due diligence, valuation, regulatory structuring, and closing. Each step carries legal-specific risks that buyers must check.

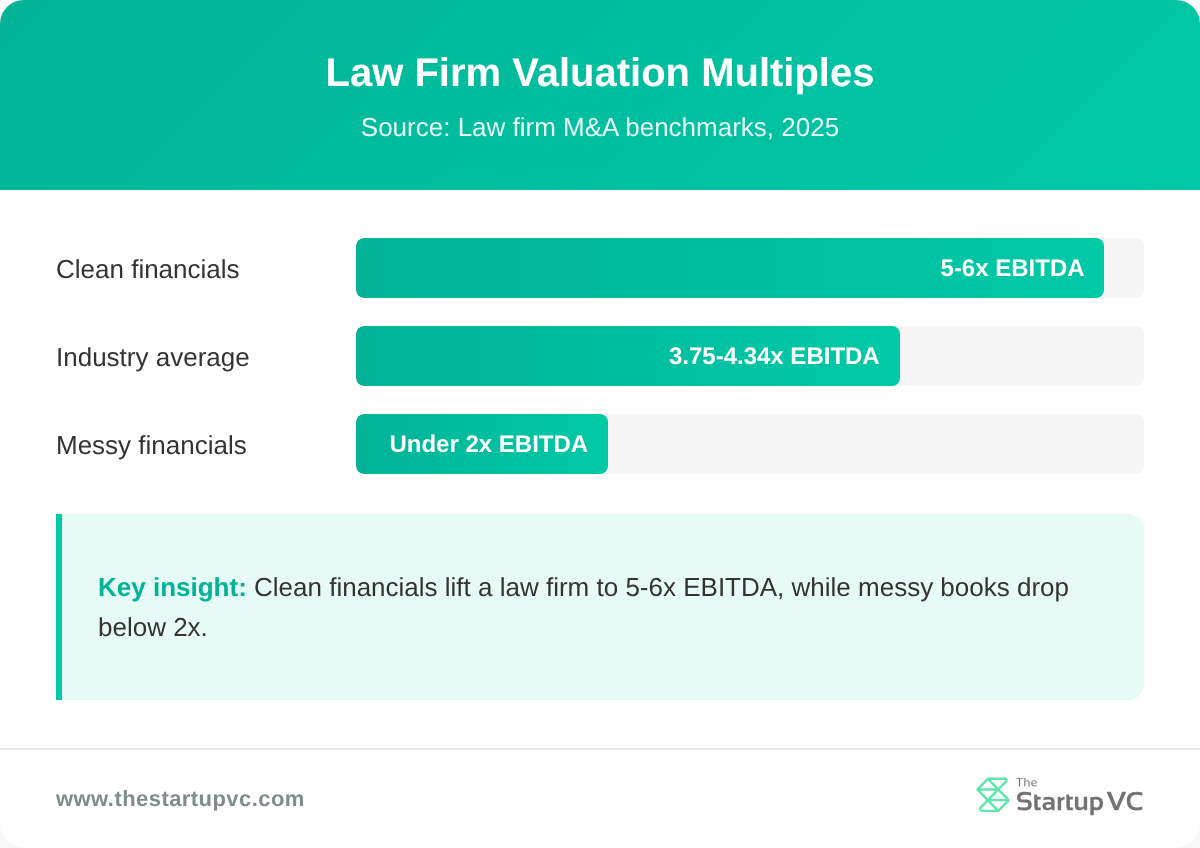

Valuation comes first in the financial work. Law firms transact at a revenue multiple of about 0.87x to 1.21x. The EBITDA multiple averages 3.75x to 4.34x. Firms with clean books command 5x to 6x EBITDA. Messy financials struggle to reach 2x EBITDA. To benchmark a target, see how to increase the valuation of a services company in Latin America.

Due diligence then protects the price. Poor financial documentation kills nearly 50% of law firm acquisitions. Buyers review realization rates, which average 88%. They check collection rates, which average 91%. They examine three to five years of trends. Client concentration is a red flag when one client tops 10% of revenue. It is also a flag when the top five clients exceed 25%.

The five main steps for a legal services acquisition are:

- Screen targets. Identify ALSPs or firms that fit your roll-up thesis.

- Run due diligence. Audit financials, realization, collections, and client concentration.

- Value the business. Apply revenue and EBITDA multiples, adjusting for owner dependency.

- Structure for compliance. Choose an ALSP purchase or an MSO to respect lawyer-only rules.

- Close and integrate. Transfer the business layer, retain key lawyers, and align licensing.

Value drivers include profitability, growth rate, client concentration, and owner dependency. These set where a firm lands in the valuation range.

What Questions Do Buyers Ask Most Often About Acquiring a Legal Services Company in Latin America?

Can a non-lawyer own a law firm in Latin America?

No. A non-lawyer cannot own a bar-licensed law firm in most of Latin America. Lawyer-only ownership rules apply in Brazil, Mexico, and Chile. Non-lawyer investors must buy an ALSP or use an MSO structure instead.

What is an ALSP and why is it acquirable?

An ALSP is an alternative legal service provider. It delivers legal work like compliance, contract review, and document services. It does not practice law as a bar-licensed firm. That status lets non-lawyer investors buy it outright.

How much does a legal services company cost to buy?

A legal services company costs about 0.87x to 1.21x revenue or 3.75x to 4.34x EBITDA on average. Firms with clean financials reach 5x to 6x EBITDA. Weak documentation can drop the multiple below 2x EBITDA.

How does the MSO structure work?

The MSO structure splits a firm into two parts. Lawyers own the core firm and practice law. Investors own the MSO, which holds technology, marketing, and back-office functions. The MSO earns a fixed management fee, not a share of legal profits.

Does a lawyer’s license transfer across Latin American countries?

No. A lawyer’s license does not automatically transfer across countries. Bar admission is country-specific. Mexico’s cedula profesional covers one nation. Colombia and Chile allow foreign requalification under set conditions.

How long does a legal services acquisition take?

A legal services acquisition usually takes several months. Due diligence on realization, collections, and client concentration drives most of the timeline. Regulatory structuring around lawyer-only rules can add further time before closing.

Ready to Acquire a Legal Services Company in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder. We create, back, and guide scalable ventures across Latin America. Our team has built and run B2B service companies in the region, including Biz Latin Hub across 17 countries. We bring operational playbooks, regional networks, and compliance expertise to every legal services roll-up. If you are planning an acquisition in the sector, explore our investment focus or Contact us today.