A Panama subsidiary lets a Colombian business invoice in USD and access deeper banking without exchange rate risk.

Colombian companies form a Panama Sociedad Anónima in 3 to 5 business days for USD 1,200 to USD 2,000. A Panama-licensed resident agent files the documents. Panama applies 2026 substance rules with a 15% penalty for shells.

The Startup VC backs B2B service companies across Latin America. Our portfolio company Biz Latin Hub runs teams in both Bogotá and Panama City. This guide covers entity selection, registration from Colombia, operational setup, tax rules, and when a Panama expansion stops making sense.

Why Do Colombian Companies Expand to Panama?

Colombian companies expand to Panama because the dollar economy, deeper banking, and free zone access solve specific pain points. The move also opens Central America and the Caribbean as service markets.

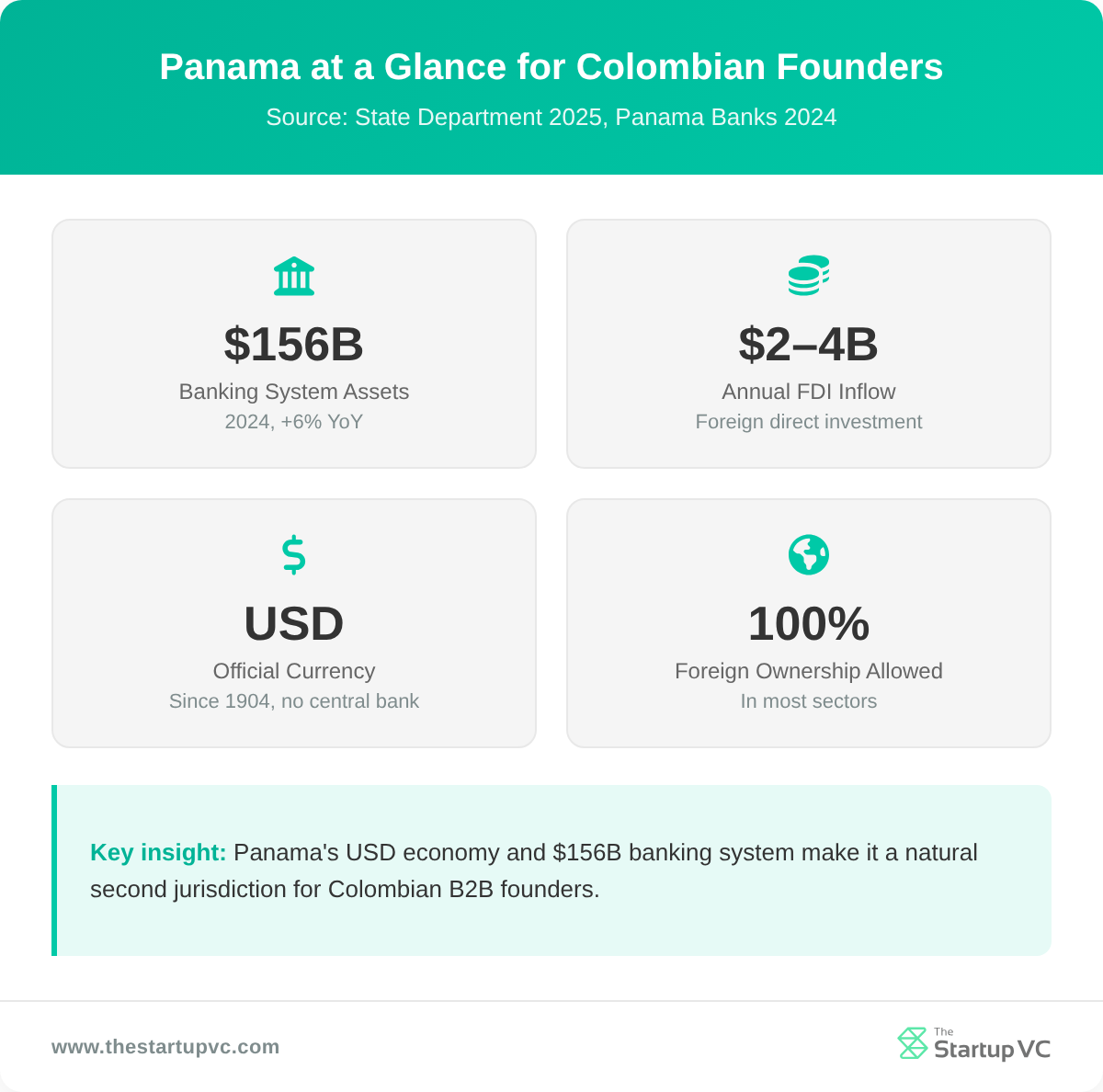

Panama has used the US dollar as its official currency since 1904. There is no central bank issuing local notes. Colombian founders billing US clients can hold revenue in USD without converting through Colombian pesos. This removes exchange rate risk and simplifies cash flow planning.

Panama’s banking system held USD 156 billion in total assets in 2024. Total assets grew 6% year-over-year. This is a much deeper financial hub than what Colombian founders typically access at home. Bancolombia operates branches directly in Panama, so Colombian founders who already bank with Bancolombia can extend that relationship across borders.

Panama also hosts the Colon Free Zone, the second largest free trade zone in the world. Many founders see Panama as a launch pad for serving Central America. Panama attracts USD 2 to 4 billion in foreign direct investment each year. A Colombian construction firm even won Panama’s first public-private partnership contract in January 2024. This is a clear sign that Colombian businesses are already active in Panama’s infrastructure pipeline.

The strategic case rests on three pillars:

- USD economy. Bills, invoices, and payroll all flow in dollars. No currency conversion risk.

- Banking depth. Panama banks regularly handle multi-currency and offshore flows that Colombian banks do not match.

- Hub geography. Easy access to Central America, the Caribbean, and US East Coast time zones.

Our overview of the entrepreneurship landscape in Colombia explains why a Colombia base often leads to Panama next.

What Legal Structures Can Your Colombia Business Use in Panama?

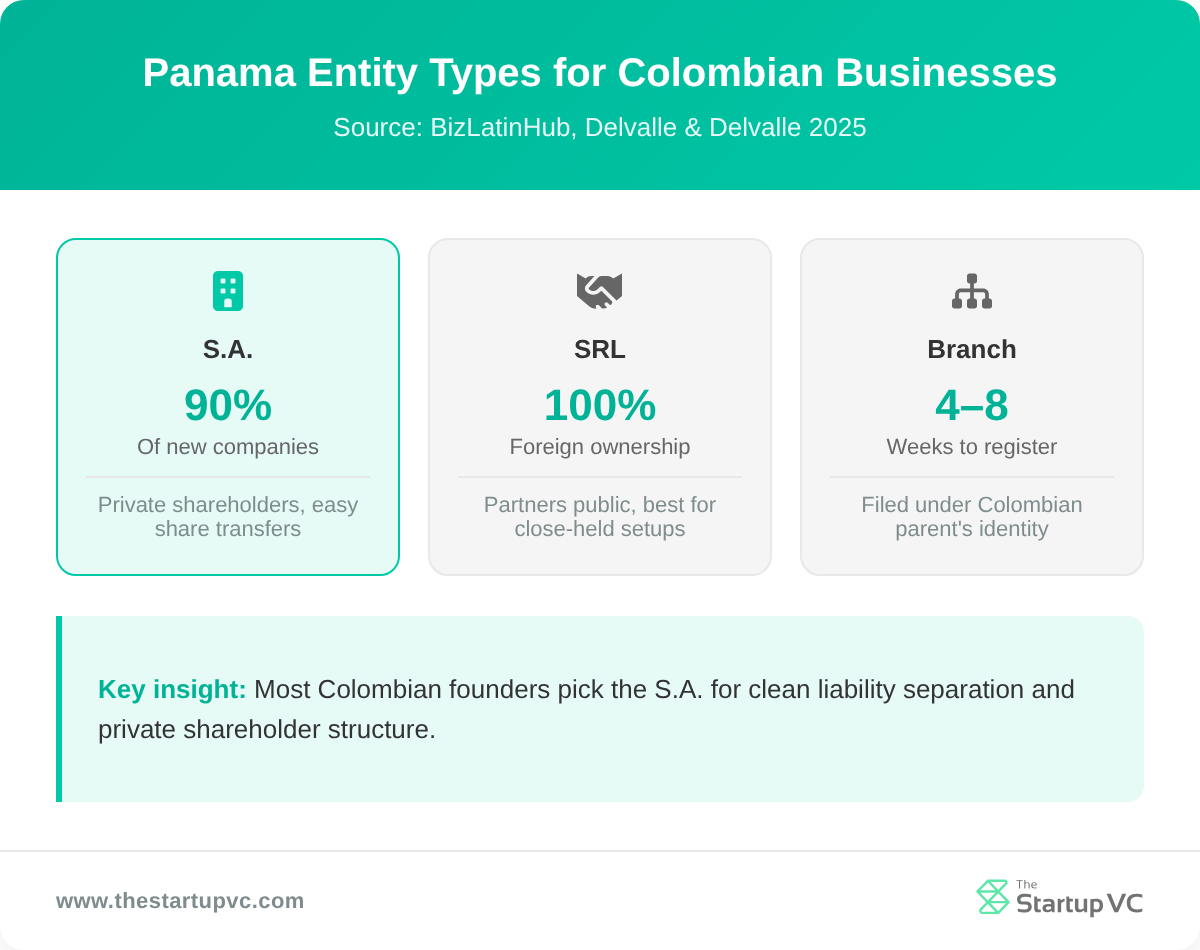

The main legal structures your Colombia business can use in Panama are three. The choices are the Sociedad Anónima (S.A.), the Sociedad de Responsabilidad Limitada (SRL), and a branch of your Colombian parent. Most foreign-owned subsidiaries are S.A.s.

More than 90% of new companies formed in Panama are S.A.s. The S.A. is Panama’s version of a corporation. It requires three directors and between 3 and 50 shareholders. Foreign nationals can hold 100% of the shares.

Privacy is one big reason founders pick the S.A. Only directors are listed in the Public Registry. Shareholders sit on a private internal register. The SRL works differently. Partner names go into the public deed at registration, and selling a quota requires partner consent plus a formal amendment.

The third option is a branch of your Colombian company. This requires filing the Colombian parent’s full corporate documents with Panama’s Public Registry. Most founders skip the branch and form a subsidiary S.A. instead. A subsidiary gives cleaner liability separation between your Colombian company and the new Panama operation.

The table below summarizes the three options for Colombian founders.

| Structure | Best For | Foreign Ownership | Setup Time |

|---|---|---|---|

| Sociedad Anónima (S.A.) | Most B2B service businesses | 100% allowed | 3 to 5 days |

| Sociedad de Responsabilidad Limitada (SRL) | Closely held partnerships | 100% allowed | 5 to 10 days |

| Branch of Colombian company | Project-based or short-term work | 100% allowed | 4 to 8 weeks |

Panama does not require a minimum paid-in capital for an S.A. But banks typically expect a USD 5,000 to USD 20,000 opening deposit. This applies when you set up the corporate account.

How Do You Register a Panama Entity From Colombia?

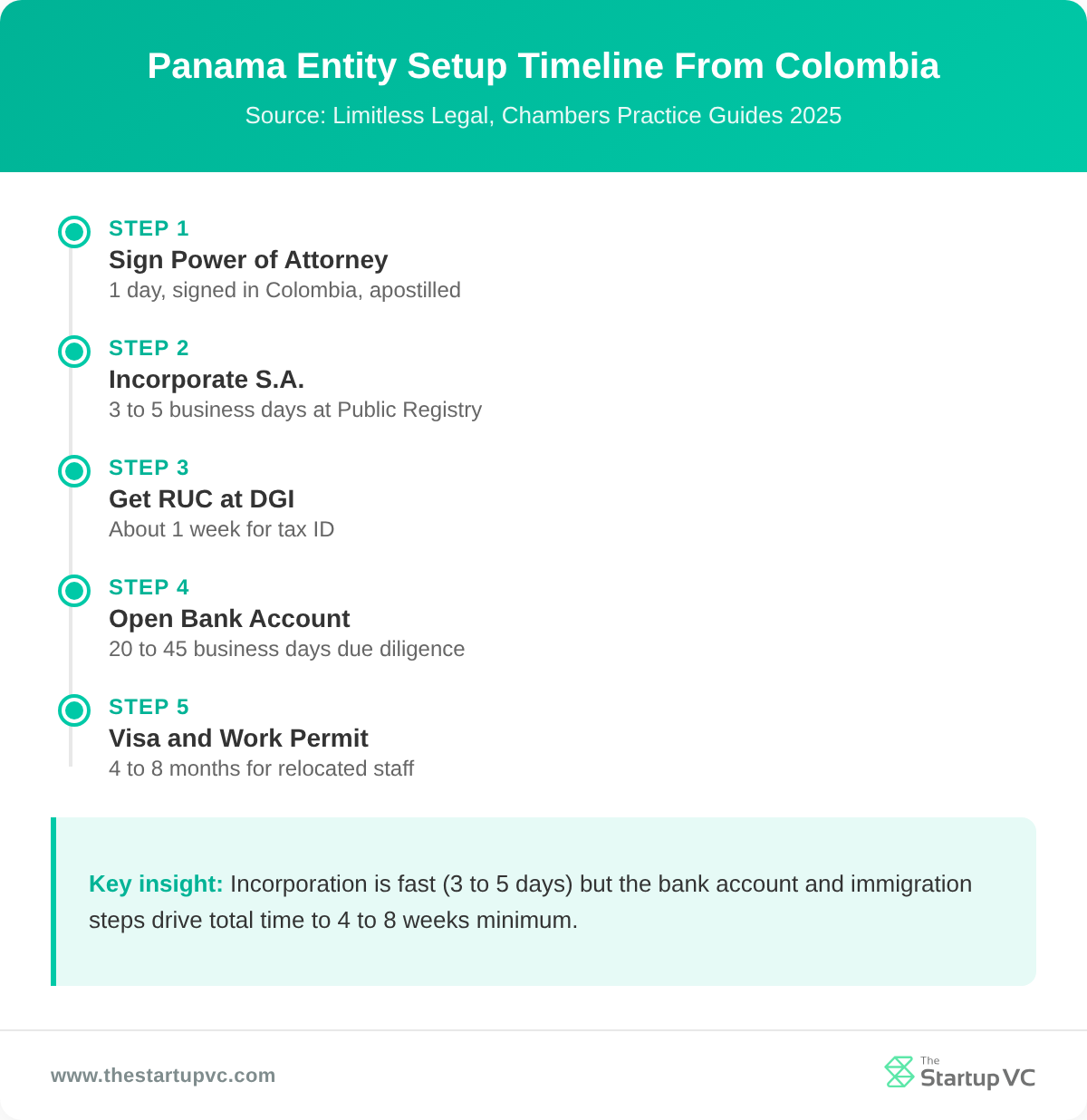

You can register a Panama entity from Colombia by giving power of attorney to a Panamanian resident agent. The agent files all documents locally. Incorporation usually takes 3 to 5 business days after signing.

Every Panama company must appoint a resident agent. The agent must be a Panamanian lawyer or law firm licensed locally. Annual resident agent fees start at USD 300. This is a legal requirement and not optional.

Colombian founders do not need to travel to Panama. The resident agent prepares the public deed. The founders sign it remotely with apostille and notarial steps from Colombia. The agent then files it with the Public Registry. Total formation costs typically range from USD 1,200 to USD 2,000. This includes the legal fee, the registry fee, and the first year of resident agent service.

After incorporation, two more steps follow:

- Register with the DGI. The Dirección General de Ingresos issues the RUC, Panama’s tax ID. You cannot open a bank account or issue invoices without it.

- Obtain the operations notice. This is the Aviso de Operación, which registers your activity with the Ministry of Commerce. Most service businesses can apply online in a few days.

New 2025 regulations expanded the resident agent’s compliance duties. Agents now must verify ultimate beneficial owners and file additional reports. If your agent does not comply, the company faces economic sanctions, registry suspension, or even dissolution in extreme cases. Pick a resident agent who handles many international clients, not the cheapest one you can find.

What Are the Operational Steps After You Register in Panama?

The operational steps after you register in Panama are clear. You must open a bank account, hire local staff, handle immigration for relocated leadership, and contract a local accountant. None of these can be fully skipped, even if your activity is offshore.

Opening a Panama corporate bank account takes 20 to 45 business days. Banks ask for many documents at submission:

- Company social pact and RUC

- Passports and second IDs for directors and signatories

- Proof of address for each signatory

- An international bank reference letter

- Proof of the source of funds

Minimum opening deposits sit between USD 5,000 and USD 20,000 at most local banks.

Hiring is governed by a clear rule. Panama law requires that at least 90% of your workforce be Panamanian nationals. Foreign employees can fill no more than 10% of regular positions. There is a separate quota for trusted technical or specialist roles.

Several professions are also reserved by law for Panamanians only:

- Accounting

- Law

- Architecture

- Engineering

- Medicine, dentistry, nursing, and veterinary work

- Retail commerce

This means you cannot relocate a Colombian-licensed accountant to keep your books in Panama. You will contract a local Panamanian accountant. Plan that into your fixed-cost budget.

For relocating Colombian executives, the Friendly Nations Visa is the most common path. It grants two-year temporary residency. Colombians qualify because Colombia is on the friendly nations list. You must show one of three things:

- A USD 200,000 real estate investment in Panama

- A USD 200,000 fixed-term bank deposit at a Panama bank

- A local Panama employment contract paying market wages

Residency must come before a work permit. The full process for one relocated executive typically takes 4 to 8 months. Founders who view Panama as a startup hub for LatAm usually start immigration filings the same week they incorporate.

What Tax and Compliance Rules Apply Between Your Colombia and Panama Entities?

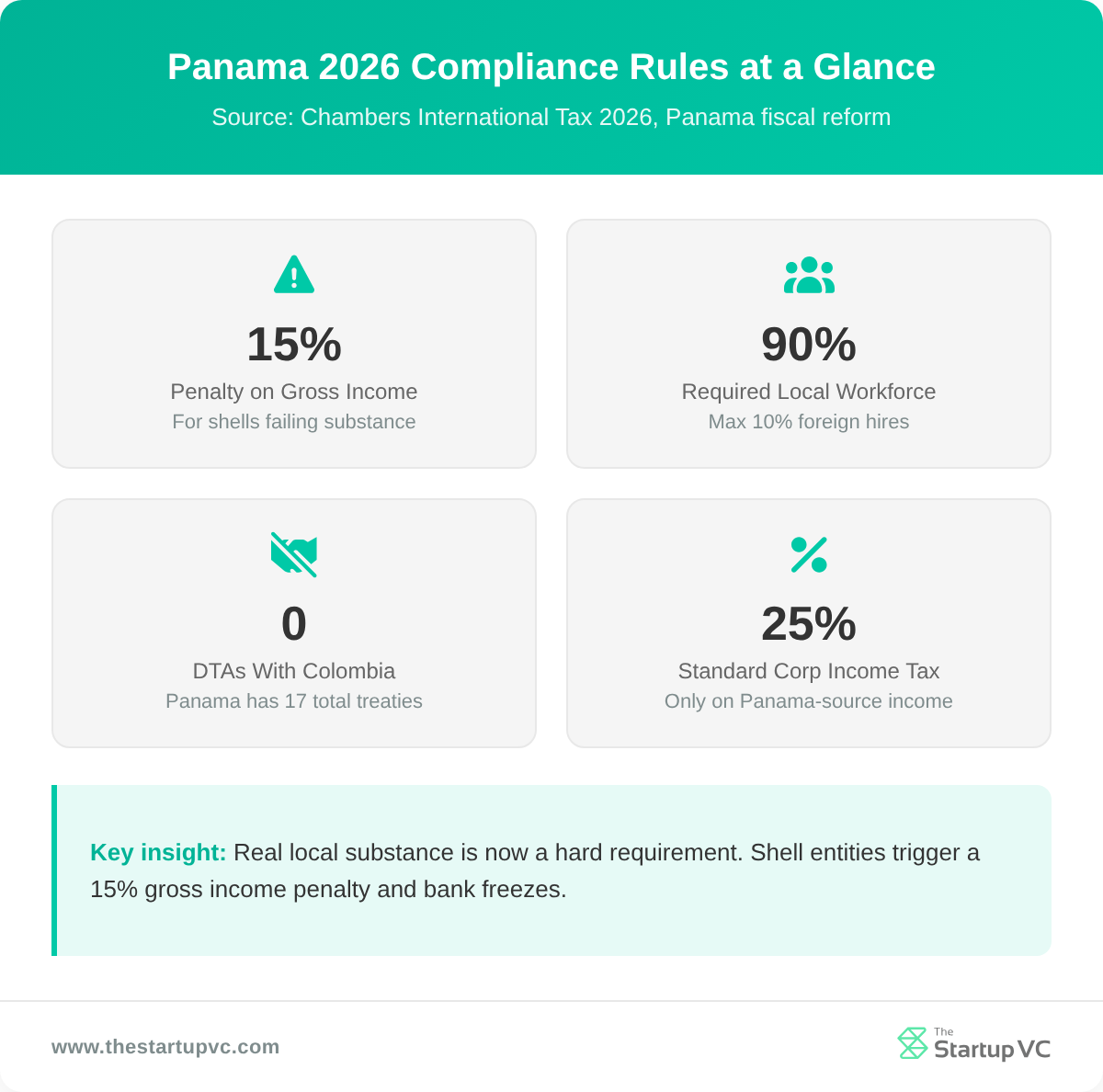

Tax and compliance rules between your Colombia and Panama entities cover four big areas. These are Panama’s territorial tax system, Colombia’s tax-haven treatment of Panama, mandatory transfer pricing, and the 2026 economic substance regime. There is no Colombia-Panama double tax treaty.

Panama applies a territorial tax system. Only income earned inside Panama is taxed by Panama. Foreign-source income earned by a Panama entity is generally exempt from Panamanian corporate income tax. The standard corporate income tax rate is 25% on Panama-source income.

The bigger issue is the Colombia side. Colombia has historically classified Panama as a tax haven. This triggers two things. First, payments your Colombian entity sends to your Panama entity face deduction limits and withholding tax. Second, any transaction between the two related entities must follow Colombia’s transfer pricing rules. That means an arm’s-length study, contemporaneous documentation, and annual filings.

There is no double tax treaty between Colombia and Panama. As of April 2026, Panama has 17 active treaties (Spain, Mexico, France, the UK, Singapore, and others). Colombia is not among them. Without a treaty, withholding taxes between the two countries follow each country’s domestic law with no relief.

The third piece is Panama’s 2026 fiscal reform. The reform introduced economic substance requirements. Entities seeking tax benefits must show:

| Substance Element | Requirement |

|---|---|

| Qualified employees | Full-time staff in Panama performing the core activity |

| Operating expenses | Real expenses in Panama (rent, payroll, utilities) |

| Decision-making | Board meetings and key decisions taken in Panama |

| Activity location | Core revenue activity not outsourced outside Panama |

Entities that fail the substance test can be charged 15% tax on their gross income. Panama also implemented the BEPS Multilateral Instrument and a Principal Purpose Test. The PPT lets tax authorities deny treaty benefits if tax avoidance was a main purpose of the structure.

Our investment focus page explains how we evaluate cross-border B2B service companies in Latin America.

When Should You Not Expand to Panama?

You should not expand to Panama in four cases. The first is when your business cannot meet substance requirements. The second is when your revenue does not justify fixed costs. The third is when your activity is reserved for Panamanian nationals. The fourth is when Colombia tax-haven friction outweighs gains. Each of these is a hard stop.

The first hard stop is substance. Shell entities no longer work. Panama’s 2026 economic substance reform requires real employees and real operating expenses in Panama. Without them, you risk a 15% gross income tax penalty and potentially frozen bank funds when payments cannot be justified.

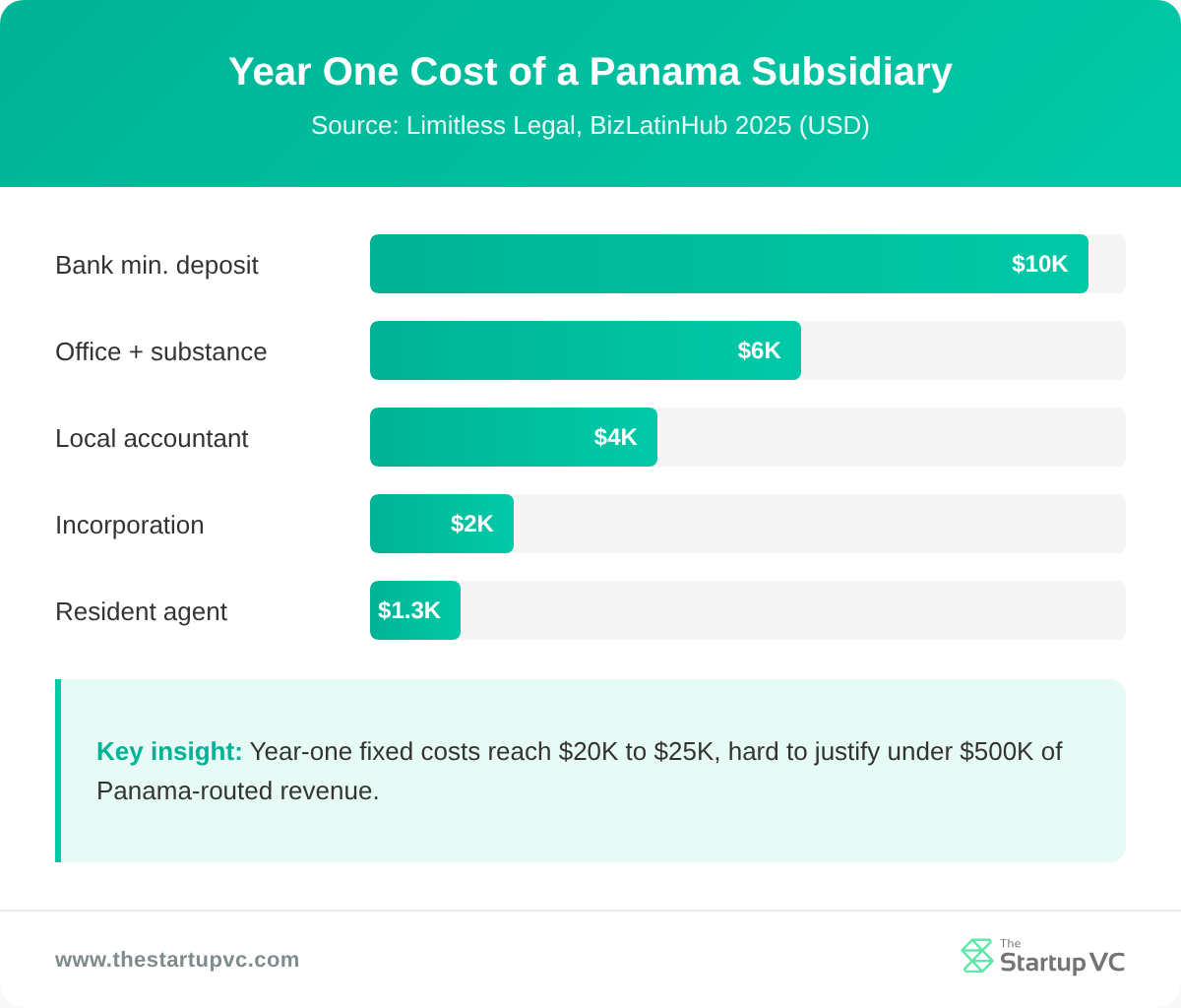

The second hard stop is cost. Annual fixed costs for a compliant Panama entity often exceed USD 25,000. This includes resident agent, accountant, office, bank fees, and reporting. Below roughly USD 500,000 in Panama-routed revenue, the math rarely works.

The third hard stop is profession. Many service activities are closed to foreign operators:

- Accounting and bookkeeping practices

- Law firms

- Architecture and engineering services

- Medical, dental, and veterinary practices

- Retail commerce open to the public

If your Colombian business is in one of these fields, you cannot replicate the operating model in Panama. You can only own passive equity or contract Panamanian professionals.

The fourth hard stop is Colombian tax-haven friction. Colombia’s classification of Panama as a tax haven means:

- Payments to your Panama entity may not be fully deductible at the Colombian level

- Mandatory transfer pricing studies for every related-party transaction

- Higher Colombian withholding on dividends, royalties, and service fees

- Extra DIAN reporting burden each year

Run the numbers before you incorporate. Hold off if any of the following are true:

- Revenue under USD 500,000 will flow through Panama

- Your customer base is mostly inside Colombia

- Your activity is reserved or regulated for Panamanians

A Panama entity that does not pay for itself is a compliance liability, not an asset.

What Questions Do Colombian Founders Ask Most Often About Expanding to Panama?

How Long Does It Take to Set Up a Panama Entity From Colombia?

Setting up a Panama entity takes about 4 to 8 weeks end to end. Incorporation itself takes 3 to 5 business days. RUC registration takes another week. The bank account is the slow step, often 20 to 45 business days from full document submission.

How Much Does a Panama Subsidiary Cost in Year One?

A Panama subsidiary costs roughly USD 8,000 to USD 25,000 in year one. Incorporation runs USD 1,200 to USD 2,000. Accounting, resident agent, office, and basic compliance add USD 6,000 to USD 23,000 depending on activity. Ongoing years are slightly cheaper, around USD 6,000 to USD 20,000.

Is There a Double Tax Treaty Between Colombia and Panama?

No, there is no double tax treaty between Colombia and Panama. Panama has 17 active treaties as of April 2026, but Colombia is not among them. Cross-border payments follow each country’s domestic withholding rules with no treaty relief.

Can a Colombian Founder Live in Panama While Running the Business?

Yes, a Colombian founder can live in Panama by applying for the Friendly Nations Visa. It grants two-year temporary residency. Colombians qualify under the friendly nations list. You need either a USD 200,000 investment or a local employment contract to apply.

Do I Need a Colombian Lawyer or a Panamanian Lawyer?

You need a Panamanian lawyer for the Panama setup. Only Panama-licensed lawyers can act as resident agents and file with the Public Registry. Your Colombian lawyer should review the cross-border structure and handle the Colombian tax and transfer pricing side.

What Happens If I Cannot Meet Panama’s Economic Substance Rules?

If you cannot meet economic substance rules, your Panama entity can face a 15% tax on gross income. Tax authorities can also reclassify your tax position. Banks can freeze incoming payments. You may lose any tax benefits the structure was designed to capture.

Ready to Expand Your Colombia Business to Panama?

Building a Panama presence on top of a Colombian operation works best with hands-on support. The Startup VC is Craig Dempsey’s family office and company builder. We back and operate B2B service ventures across Latin America. Our portfolio company Biz Latin Hub runs teams in 17 Latin American countries, including Bogotá and Panama City. We help Colombian founders structure the second entity, manage substance and transfer pricing, and recruit local Panamanian leadership. Contact us today to map your Colombia-Panama expansion.