Latin America recorded 2,650 M&A deals worth nearly US$96 billion in the first 11 months of 2025. Inbound investment rose 45% year over year.

Sell-side due diligence preparation in Latin America takes 12 to 18 months. It requires audited financials, a Quality of Earnings report, and a virtual data room. Buyers expect 200 to 500 documents across Brazil, Mexico, and Colombia.

The Startup VC supports founders preparing for exit across Latin America. We bring hands-on experience from Biz Latin Hub operating in 17 countries. Below, you will find the sell-side readiness checklist, data room structure, and the LatAm-specific risks that derail deals.

What Is Sell-Side M&A Due Diligence in Latin America?

Sell-side M&A due diligence is a seller-led review that prepares your company for buyer scrutiny before the deal process begins. You commission the same checks a buyer would run, fix problems early, and control the narrative.

Sellers in Latin America benefit from a 12 to 18 month preparation window. A faster 3 to 6 month sprint works only when audited financials are already in place. The full sale process, from preparation to close, takes 6 to 12 months across four stages.

The four sell-side stages are:

- Prepare. Assemble advisors, run reverse due diligence, build the data room, fix red flags.

- Market. Send teasers, sign NDAs, share the CIM, and run management meetings with qualified buyers.

- Diligence. Buyers conduct 8 to 12 weeks of financial, legal, tax, and commercial diligence.

- Close. Sign purchase agreement, satisfy closing conditions, transfer ownership.

Latin America’s M&A market is active right now. Deal volume reached 2,650 transactions worth US$96 billion in the first 11 months of 2025. US inbound investment alone grew 407% year over year, with Brazil capturing more than 55% of regional deal volume.

How Do You Build a Data Room for a Latin American M&A Deal?

You build a data room by setting up a secure virtual platform and organizing documents into eight top-level folders. Populate each folder before buyers arrive. Control access with tiered permissions.

The virtual data room (VDR) is the central document hub for the entire diligence process. Buyer diligence requests typically include 200 to 500 documents, depending on company size and complexity.

What Top-Level Folders Should Your Data Room Have?

Your data room should have eight top-level folders organized by document type:

| Folder | Contents |

|---|---|

| 1. Corporate | Bylaws, shareholder register, board minutes, subsidiaries list |

| 2. Financial | Audited statements, management accounts, QoE report, budgets |

| 3. Legal | Material contracts, litigation, leases, regulatory licenses |

| 4. Tax | Income tax returns, VAT/IVA filings, transfer pricing studies |

| 5. HR | Employee census, contracts, benefits, labor disputes |

| 6. IP | Trademarks, patents, software registrations, domain names |

| 7. Commercial | Customer contracts, supplier agreements, pricing schedules |

| 8. Bidder Pack | NDA, teaser, CIM, management presentation |

The bidder pack folder holds files all qualified bidders need at the start. The other seven folders open in tiers based on the bidder’s diligence stage.

How Do You Control Access in a Data Room?

You control access by setting tiered permissions, watermarking sensitive files, restricting downloads, and tracking activity logs.

VDR platforms support staged disclosure. Tier 1 access opens basic financial and corporate documents to all qualified bidders. Tier 2 access opens sensitive items like customer contracts and IP only to finalists. Audit logs track every document opened by every user.

What Financial Documents Must You Prepare for Due Diligence?

You must prepare audited financial statements, a Quality of Earnings report, working capital schedules, tax filings, and supporting management accounts. These are the non-negotiables for any serious buyer.

Buyers in middle-market M&A deals rely on QoE reports rather than audits alone. Even companies with clean audit opinions go through a QoE during the sale process.

What Audited Financials Do Buyers Require?

Buyers require three to five years of audited financial statements. Local books in Latin America often follow national accounting standards. You must convert to IFRS or US GAAP for cross-border buyers.

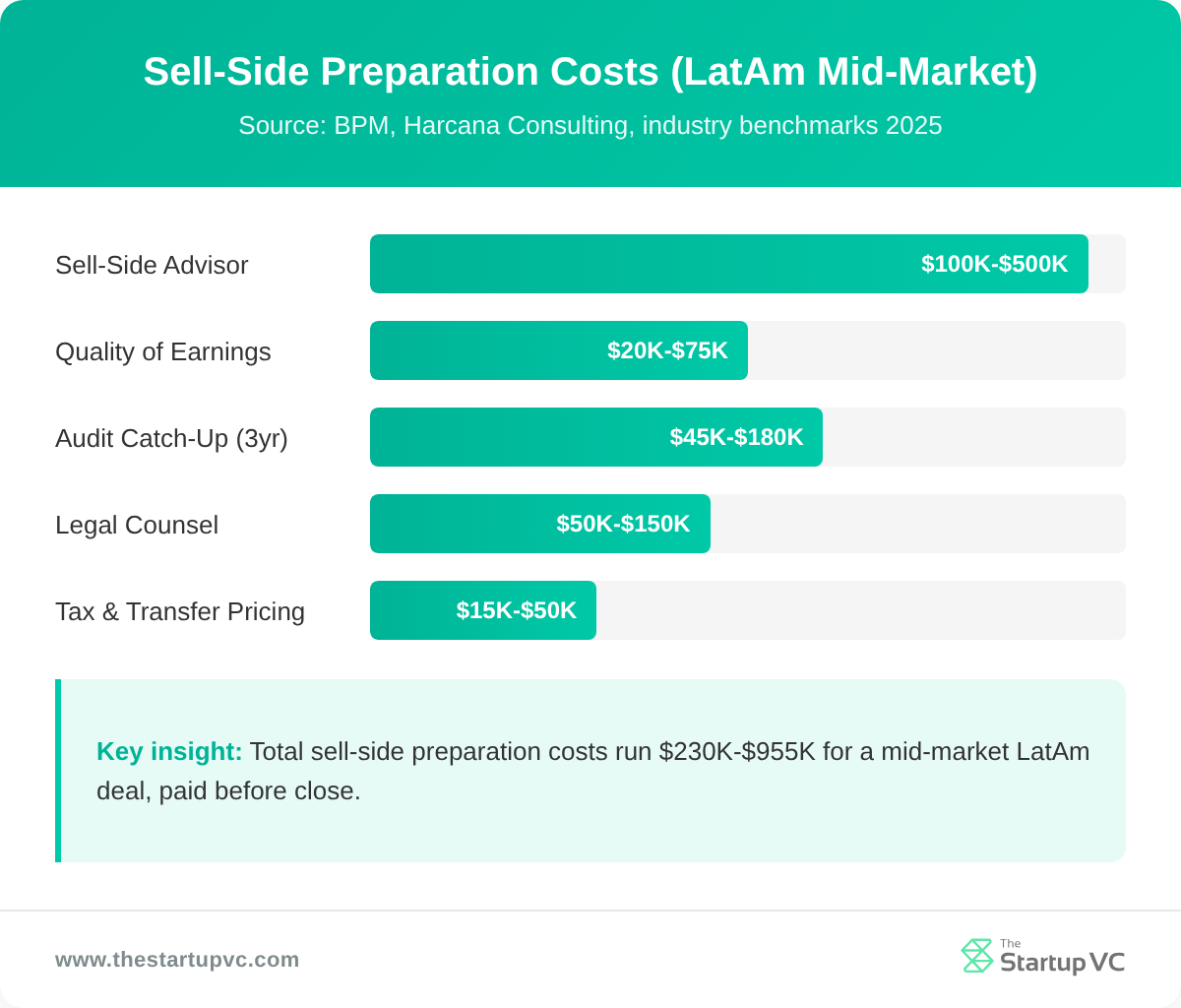

Audit conversion typically costs US$15,000 to US$60,000 per year, depending on company size. Plan for 8 to 12 weeks of audit work per year if starting from unaudited records.

Why Is a Quality of Earnings Report Essential?

A QoE report is essential because it strips out one-time items from EBITDA to show normalized, recurring earnings. Buyers anchor their valuation on QoE EBITDA, not reported EBITDA.

Mid-market QoE engagements take 3 to 6 weeks and cost US$20,000 to US$75,000. The report covers revenue recognition, customer concentration, working capital trends, and adjustments for owner perks or related-party transactions.

What Tax Documents Do You Need?

The tax documents you need include several core filings:

- Income tax returns for the last 5 years

- VAT or IVA filings

- Transfer pricing studies

- Any pending audits or assessments

Latin American tax authorities are aggressive. Pending audits in Brazil, Mexico, or Colombia can stall deals or trigger purchase price reductions. Disclose every open audit and assessment in the data room.

How Should You Handle Legal and Regulatory Disclosures in LatAm?

You handle legal and regulatory disclosures by hiring local counsel in each jurisdiction. Catalog contracts and IP filings country by country. Disclose all pending litigation and regulatory matters in the data room.

Local counsel is essential because rules vary across jurisdictions. Corporate governance, foreign investment restrictions, and labor codes differ in Brazil, Mexico, Colombia, and Chile.

What Corporate Records Must You Disclose?

You must disclose every key corporate record:

- Bylaws and constitutional documents

- Shareholder register with complete transfer history

- Board and shareholder meeting minutes

- Capital increases and share transfers

- Corporate structure for all subsidiaries and affiliates

Family-owned LatAm businesses often have informal records. Buyers expect complete, signed, and registered corporate books. Reconstruct missing minutes and register all transfers before going to market.

How Do You Manage IP Filings Across LatAm?

You manage IP filings by cataloging every trademark, patent, and software registration in each country where the company operates. Latin America has no regional IP harmonization.

| Country | IP Registry | Common Issues |

|---|---|---|

| Brazil | INPI | Long pendency, mandatory local agent |

| Mexico | IMPI | Class-specific filings, renewal gaps |

| Colombia | SIC | Cancellation actions, opposition risk |

| Chile | INAPI | Annual renewals, local representation |

| Argentina | INPI Argentina | Slow examination, currency controls |

What Regulatory Disclosures Apply in 2026?

The key regulatory disclosures in 2026 cover four areas: ESG reporting, data protection, anti-corruption diligence, and foreign investment rules.

Brazil’s CVM Resolution 193 mandates ISSB-aligned sustainability disclosures for public companies starting January 2026. Colombia, Costa Rica, and Mexico have implemented similar rules. Brazil’s LGPD and similar laws in Mexico, Colombia, and Chile require data protection compliance disclosures.

Anti-corruption due diligence must cover FCPA risk analysis, review of agents and intermediaries, and audit of high-risk transactions. Pre-acquisition violations transfer to the buyer at close.

What LatAm-Specific Risks Trip Up Sellers During Due Diligence?

The LatAm-specific risks that trip up sellers are five recurring issues:

- Informal employment exposure

- Parallel or shadow entities

- Transfer pricing gaps

- Successor liability claims

- Labor reclassification disputes

Each can reduce purchase price or kill the deal.

More than half of the working population in Latin America is engaged in informal employment. Buyers price labor reclassification risk heavily into deals.

How Do You Address Informal Employment?

You address informal employment by auditing your workforce first. Reclassify contractors who function as employees. Pay back wages and benefits. Formalize every working relationship before going to market.

Common red flags include long-term contractors with fixed schedules, employees paid partly off the books, and consultants receiving company benefits. Buyers run their own labor audits during diligence and demand indemnities for any gaps found.

Why Are Parallel Entities a Problem?

Parallel entities are a problem because buyers cannot value or acquire what they cannot see clearly. Family-owned LatAm businesses often hold assets, revenue, or liabilities in unused or related companies.

Buyers require consolidation of all parallel entities, write-off of intercompany loans, and formal liquidation of shell companies before close. Plan 6 to 9 months for entity cleanup if your structure is complex.

What Transfer Pricing Documentation Is Required?

The transfer pricing documentation required includes a master file, local file, country-by-country report, and an annual transfer pricing study. These are mandatory in Mexico, Brazil, Colombia, and Argentina.

Missing or outdated transfer pricing studies trigger BEPS-aligned assessments. Tax authorities can adjust historical EBITDA, which directly reduces purchase price. Commission updated studies for the three most recent years before opening the data room.

How Does Successor Liability Work in Brazil?

Successor liability in Brazil works by transferring labor, tax, and environmental claims to the buyer, even in asset purchase deals. Brazilian courts apply expansive successor liability doctrines that prioritize worker and tax authority protection.

This means asset deals do not insulate buyers from legacy claims. Sellers must disclose every labor lawsuit, tax assessment, and environmental matter. Specific risks are typically covered by tailored indemnities outside general liability caps. General caps range from 10% to 30% of purchase price.

Our guide on what acquirers look for in LatAm B2B companies covers the buyer-side perspective on these same risks.

What Questions Do Founders Ask Most Often About M&A Due Diligence Preparation?

How Long Does Sell-Side Due Diligence Preparation Take?

Sell-side due diligence preparation takes 12 to 18 months for a full readiness program. A faster 3 to 6 month sprint works only if audited financials and a QoE report are already in place. The full sale process from preparation to close runs 6 to 12 months.

How Much Does Sell-Side Due Diligence Cost?

Sell-side due diligence costs US$100,000 to US$500,000 for a mid-market deal. QoE reports run US$20,000 to US$75,000. Audit catch-up runs US$15,000 to US$60,000 per year. Sell-side advisory fees range from 1% to 5% of deal value.

What Advisors Do You Need for Sell-Side Preparation?

The advisors you need are M&A counsel, an investment banker, QoE accountants, and tax counsel. Hire local counsel in every country where the company has material operations.

What Documents Do Buyers Request First?

Buyers request audited financials, the QoE report, working capital schedules, tax returns, corporate bylaws, shareholder register, and material contracts first. These open the data room. Expect 200 to 500 supporting documents across all folders.

What Are the Biggest Red Flags in LatAm Deals?

The biggest red flags in LatAm deals are unaudited financials, missing transfer pricing studies, and informal employment. Other common issues include parallel entities, pending tax audits, IP filing gaps, and unresolved labor lawsuits. Fix each before going to market.

Which Country Has the Most LatAm M&A Activity?

Brazil has the most LatAm M&A activity, capturing over 55% of regional deal volume in 2024. Chile, Mexico, Colombia, Argentina, and Peru follow by volume. Mexico, Colombia, Argentina, Chile, and Peru follow by deal value.

Ready to Prepare Your Company for M&A Due Diligence?

The Startup VC works with founders across Latin America to prepare companies for sale. We are Craig Dempsey’s family office and company builder. We bring hands-on experience from running Biz Latin Hub across 17 countries. We help sellers structure financials, build data rooms, fix red flags, and navigate regional risks. Contact us today to start your sell-side readiness review. You can also explore our work on selling a company in Latin America.