Selling a founder-led business in Latin America takes 9-12 months and trades at 6-8x EBITDA, with ~31% of price deferred through earnouts.

Latin America saw 2,904 M&A deals worth US$87.7 billion in 2024, up 16% year over year. Founder-led companies typically trade at a 20-30% discount to public multiples. Rolling equity of 15-35% bridges the valuation gap for owner-operator sales.

The Startup VC is Craig Dempsey’s family office and company builder. Craig built and sold Biz Latin Hub to Vistra in December 2025 after scaling the firm across 17 countries. This guide draws on that lived experience to cover valuation, key-person risk, deal structure, buyer types, and the practical steps every founder should take 2-3 years before sale.

What Is a Founder-Led Business and Why Does It Need a Special Sale Process?

A founder-led business is a company where the founder still runs daily operations. The founder also holds the key customer, supplier, and team relationships. Buyers call this concentration “key-person risk.” It changes the entire sale process compared to a professionally managed company.

In owner-operator companies, the “hit by a bus” test usually points to one name: the founder. That single point of failure becomes a valuation discount during due diligence. Buyers ask how dependent the business is on the owner’s personal guarantees, client trust, and operating playbook.

Latin America adds another layer. In LatAm B2B service companies, client relationships often run through the founder personally. Local custom places significant weight on the owner’s word with clients and regulators. Selling means transferring not just contracts but trust.

This shows up in deal data. Seasoned founders captured 42% of LatAm startup dollars in 2023-24, up from 23% in 2021. Investors and buyers prefer experienced founder-CEOs but also know how much deal value sits on the founder’s shoulders. A founder-led sale must address that head-on.

The typical founder exit pattern in Latin America looks like this:

- Key-person concentration. Customer, supplier, and team relationships sit with the founder.

- Informal documentation. Processes live in the founder’s head, not in a CRM or SOP.

- Trust-driven contracts. Many deals close on the founder’s reputation, not paperwork.

- Cross-border complexity. Buyers from the US or Europe need local counsel to navigate FDI, labor, and tax rules.

The fix is not to sell faster. The fix is to design a sale process that priced and transferred founder dependence carefully. That is what the rest of this guide covers.

How Much Is Your Founder-Led Business Worth in Latin America?

Your founder-led business is worth a multiple of its EBITDA, adjusted for size, sector, and key-person risk. Latin America’s M&A market is active. In 2024, LatAm saw 2,904 deals worth US$87.7 billion, with deal value up 16% year over year. Real buyers are paying real prices for quality founder-led targets.

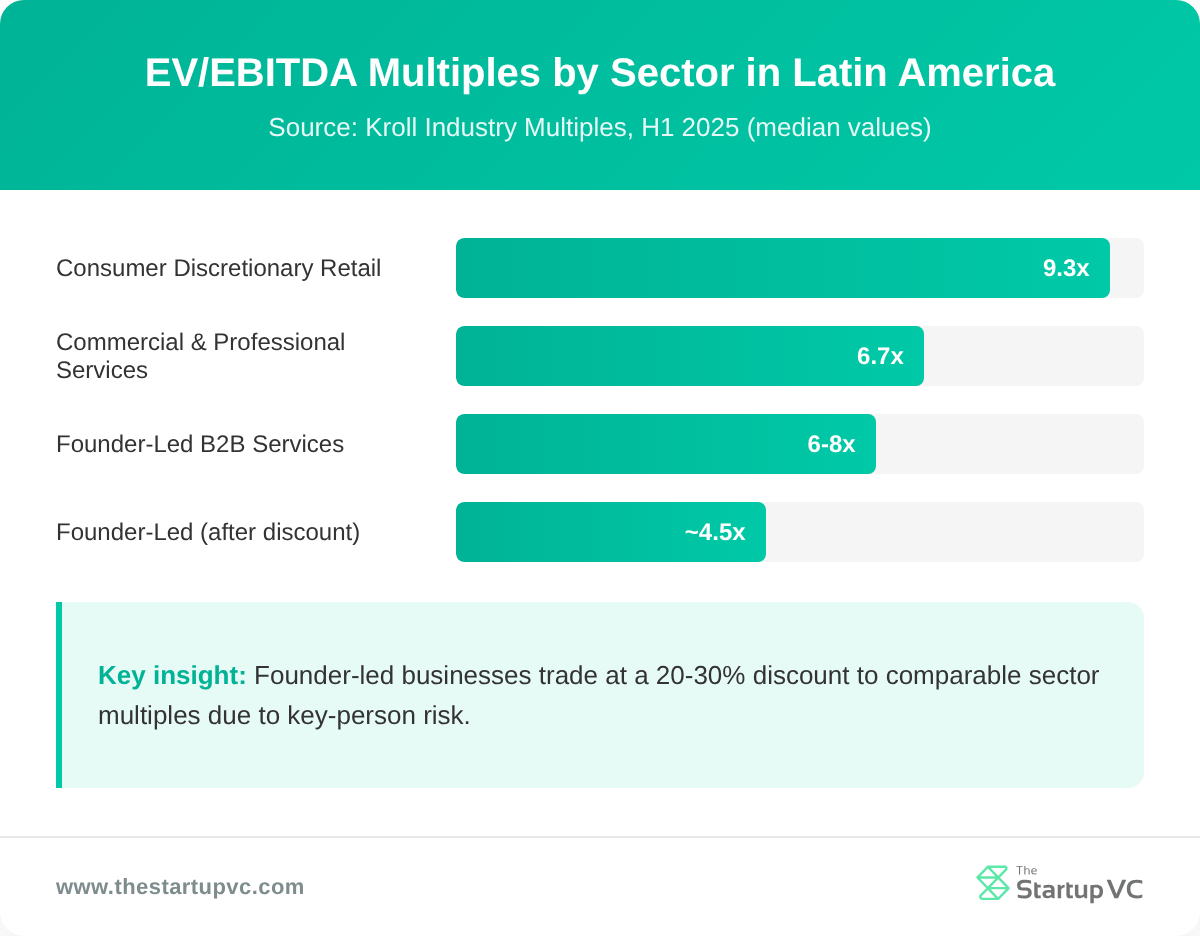

Multiples vary sharply by sector. Kroll’s Q1-Q2 2025 data shows consumer discretionary distribution and retail at a median 9.3x EV/EBITDA. Commercial and professional services dropped to 6.7x. Founder-led B2B service companies usually fall in the 6-8x range before adjustments.

Here is how multiples have shifted in Latin America:

| Sector | End-2024 Median | H1-2025 Median |

|---|---|---|

| Consumer discretionary retail | 6.3x | 9.3x |

| Commercial and professional services | 8.5x | 6.7x |

| Capital goods | Stable | Stable |

| Real estate | Declined | Stable |

| Healthcare | Declined | Stable |

The IMF projects 2.2% LatAm growth in 2025, down from 2.4% in 2024. Buyers price this slower growth into the country-risk premium. That premium narrows the multiple by 1-2 turns for LatAm targets compared to US peers.

Founder-led businesses typically trade at a 20-30% discount to comparable public multiples. The discount reflects key-person risk, customer concentration, and informal documentation. Buyers do not always argue down the headline price. They use earnouts and rolling equity to bridge the gap. The next section covers that structure.

Aggregate private equity deal value in LatAm was US$4.1 billion in Q4 2024 and US$4.6 billion in Q1 2025. Capital is steady for businesses in the $10M-$100M EBITDA range. The buyer side is not the problem. The seller side, with poor documentation or single-founder dependence, is where deals stall.

What Are the Main Steps to Sell a Founder-Led Business in Latin America?

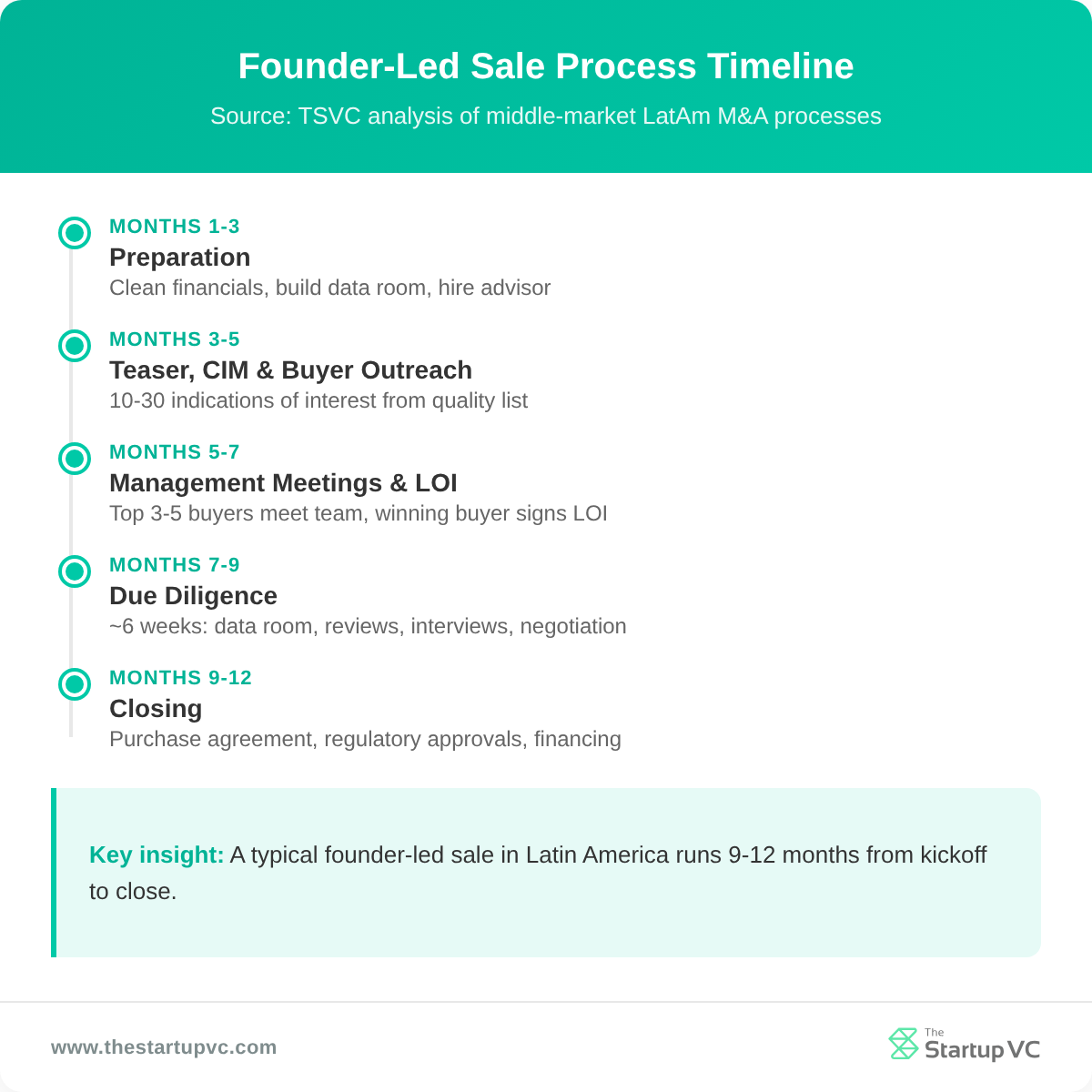

You can sell a founder-led business in Latin America by running a seven-phase process. The phases are preparation, teaser and CIM, buyer outreach, management meetings, letter of intent, due diligence, and closing. Each phase has its own timeline and risk points.

The full process usually takes 9-12 months from kickoff to closing. Here are the main steps:

- Preparation (months 1-3). Clean financials, build a data room, hire an advisor, document succession plans. The cleaner your prep, the higher your final price.

- Teaser and CIM (month 3-4). Your advisor creates a one-page teaser and a 30-50 page confidential information memorandum. Both go to qualified buyers under NDA.

- Buyer outreach (months 4-5). Outreach to a curated list of strategic buyers, private equity firms, search funds, and family offices. Expect 10-30 indications of interest from a quality list.

- Management meetings (month 5-6). Top 3-5 buyers meet the founder and management team. This is where buyers test for key-person risk and culture fit.

- Letter of intent (month 6-7). The winning buyer signs an LOI that fixes price, structure, earnout terms, and rolling equity. The LOI also opens the data room.

- Due diligence (months 7-9). A standard middle-market diligence runs about 6 weeks. Days 1-7 cover data room launch. Days 8-21 cover functional reviews. Days 22-28 cover management interviews. Days 29-42 cover synthesis and negotiation.

- Closing (months 9-12). Finalize the purchase agreement and get regulatory approvals. The approval bodies are CADE in Brazil, COFECE in Mexico, and FNE in Chile. Then arrange financing, announce the deal, and start integration.

Foreign bidders face extra complexity in Latin America. FDI policies, foreign exchange controls, corporate securities law, and labor law all vary by country. Cultural and language differences make diligence slower. Local counsel is not optional. It is the difference between a clean close and a deal that stalls.

Brazil and Mexico carry the most complex tax and labor regimes in the region. Sellers should expect tax and labor contingencies to dominate the indemnity package and escrow holdback. A clean labor file in Brazil or Mexico can be worth 10% of headline price by the end of negotiations. For a deeper look at what buyers actually pay for, see our guide to what acquirers look for in LatAm B2B service companies.

How Do Earnouts and Rolling Equity Work in a Founder Exit?

Earnouts and rolling equity work by deferring part of the purchase price until the business hits agreed targets after closing. An earnout is contingent additional payment tied to post-closing performance. Rolling equity is an ownership stake the founder keeps in the post-closing company.

Both tools share the same purpose. They bridge the valuation gap between what the founder thinks the business is worth today and what the buyer is willing to pay for tomorrow’s results. They also address key-person risk by keeping the founder engaged after close.

Here is how the two tools compare:

| Tool | Typical Size | Trigger | Time Horizon |

|---|---|---|---|

| Earnout | 31% of closing payment (2024 median) | Revenue or EBITDA targets | 1-3 years |

| Rolling equity | 15-25% (main street), 20-35% (lower mid-market) | Buyer exit or recap | 3-7 years |

| Escrow holdback | 8-15% of purchase price | Rep and warranty claims | 12-24 months |

Most earnouts use revenue as the trigger. EBITDA is second. Sellers should push hard for revenue earnouts when buyers control cost decisions after close. A buyer who invests heavily in growth can suppress EBITDA and kill the earnout. That happens even when revenue grows fast.

Rolling equity gives the founder upside if the buyer scales the business. In a typical private equity deal, the founder rolls 20-30% of the proceeds back into the new entity. When the buyer sells in 5-7 years, the founder gets a second payout on the bigger company.

Escrow holdbacks of 8-15% of purchase price fund indemnity claims for 12-24 months after close. In LatAm deals, tax and labor reps drive the holdback because contingencies often surface late. Sellers should negotiate a cap on indemnity exposure equal to the escrow amount. That cap should not be a percentage of headline price.

Earnouts and rolling equity convert “key-person risk” into “key-person alignment.” Done right, they keep the founder motivated through the transition and protect the buyer’s downside. Done wrong, they create years of fights over how the business should be run.

How Do You Reduce Key-Person Risk Before Selling Your Family Business?

You reduce key-person risk by building a deal-ready management team, transferring relationships off the founder, and documenting processes 2-3 years before sale. Buyers discount price when they see a single point of failure at the top of the org chart.

Apply the “hit by a bus” test to every key role. Who is the business least prepared to lose? Document the answer for every name on the org chart and build a backup plan for each. The exercise looks simple. The fixes take years.

A deal-ready management team usually includes a CFO, head of sales, and head of operations. The CFO matters most. Buyers will not accept founder-led financial reporting. Without a CFO, your data room looks weak and your multiple drops.

Here are five steps to reduce key-person risk before going to market:

- Hire a CFO. Move financial reporting off the founder 18-24 months before sale. Clean monthly statements close the diligence trust gap fast.

- Document customer relationships. Introduce a second contact for top 10 accounts 12-18 months before sale. Buyers want to see customer loyalty to the business, not to the founder.

- Codify the operating playbook. Write SOPs for sales, delivery, and back office. Internal wiki, runbooks, or a learning system all work.

- Build a leadership bench. Buyers want named succession for every C-level role. If the founder is the only one who can do a job, that job is at risk.

- Buy key person insurance. Key person insurance and well-funded buy-sell agreements protect deal value. They cover the gap if a key executive leaves unexpectedly during the sale.

The pattern in successful LatAm founder exits is consistent. The founder spends the final 24 months before sale making the business less dependent on the founder. That is counterintuitive. It is also exactly what buyers pay a premium for.

Which Buyers Acquire Founder-Led Businesses in Latin America?

The buyers who acquire founder-led businesses in Latin America are strategic acquirers, private equity firms, search funds, and family offices. Each group offers a different deal structure, time horizon, and post-sale role for the founder.

Strategic buyers are operating companies that buy targets to add capability, geography, or revenue. Vistra is a clear example. Vistra acquired Biz Latin Hub on December 4, 2025, after a long-running partnership that started around 2018. Vistra operates with 9,000+ experts across 50+ markets. The deal formalized a relationship that had grown over seven years. Craig Dempsey, BLH’s co-founder, redirected his energy to The Startup VC, his family office and company builder. For a closer look at how that founder exit was structured, see the Vistra acquisition of Biz Latin Hub.

Private equity firms come in two flavors. Global firms include General Atlantic and L Catterton. General Atlantic manages US$100B+ AUM with a dedicated LatAm team. L Catterton manages US$37B AUM and targets consumer roll-ups and founder-led transitions in Mexico, Brazil, and the Southern Cone. Regional specialists include Vinci Partners and Aqua Capital. Vinci Partners (Brazil) acquired MAV Capital in 2024. Aqua Capital manages $1.1B+ AUM focused on agribusiness across Brazil, the Southern Cone, and Mexico.

Here are the main buyer types for LatAm founder-led businesses:

| Buyer Type | Typical Deal Size | Founder Role Post-Sale |

|---|---|---|

| Strategic acquirer | $20M-$500M+ | 1-3 year transition, often executive role |

| Global private equity | $50M-$300M | CEO continuity with rolling equity |

| Regional private equity | $10M-$100M | CEO or board role, larger rolling equity |

| Search fund | $5M-$30M | Hand-off to operator-buyer over 6-12 months |

| Family office | $5M-$50M | Flexible, often long-term partnership |

Search funds are a growing buyer class. A search fund is an investor who raises capital to buy and run one company. Search funds work well for founders who want their company to continue under a hands-on operator-buyer rather than a financial sponsor. The trade-off is smaller deal size and slower closing.

Family offices, such as The Startup VC, acquire and back founder-led service businesses across Latin America. Family offices typically allow founders to retain control through rolling equity. They offer operational playbooks, regional team networks, and compliance expertise. The model fits founders who want to stay involved and benefit from a long-term partner. Learn more about The Startup VC’s investment focus and our portfolio of venture companies across the region.

What Questions Do Founder-CEOs Ask Most Often About Selling Their Business?

How Long Does It Take to Sell a Founder-Led Business in Latin America?

Selling a founder-led business in Latin America takes 9-12 months from kickoff to close. Due diligence alone runs about 6 weeks for a middle-market deal. Add 3-6 months for prep and 1-2 months for regulatory approval. Clean financials and a strong management team cut weeks off the timeline.

How Much Tax Will You Pay on the Sale?

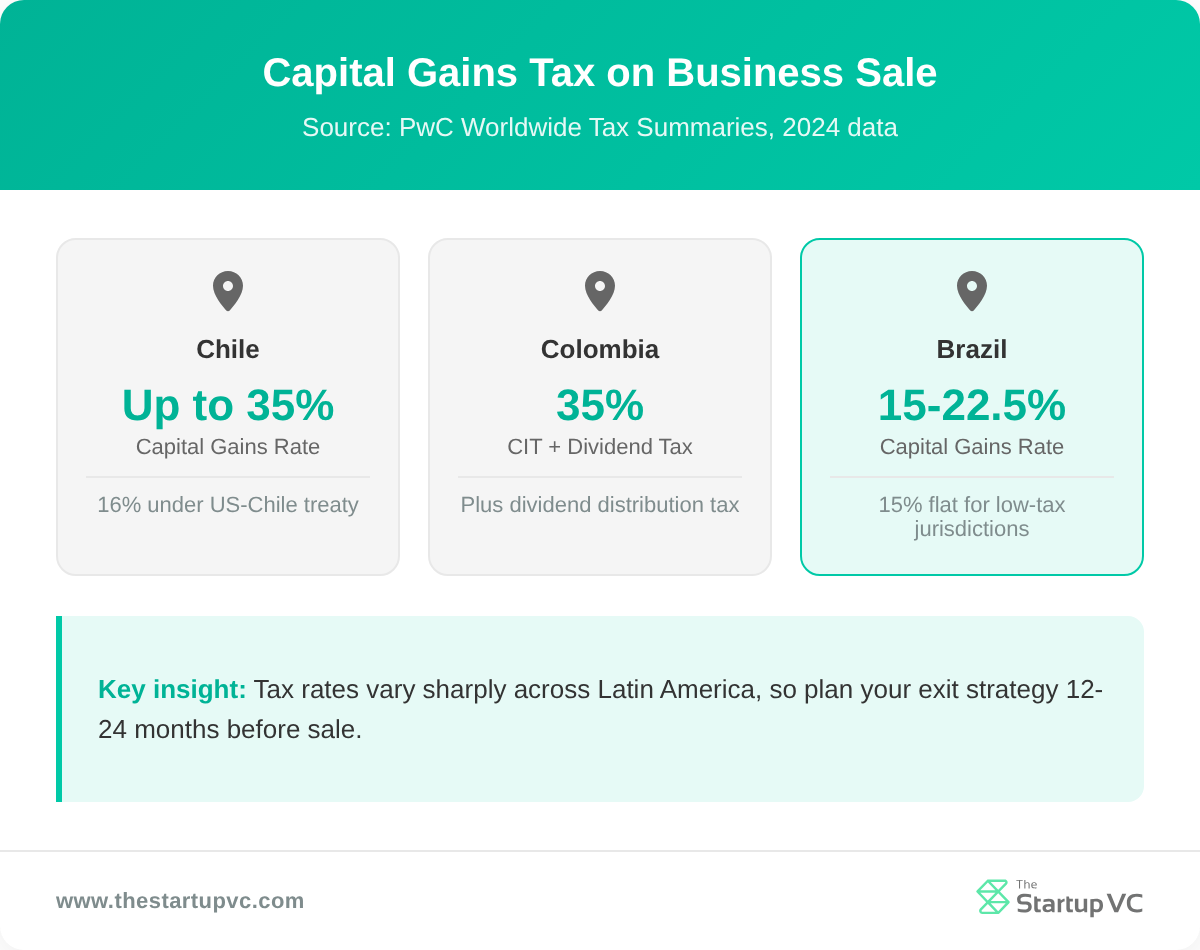

Capital gains tax rates vary across Latin America. Chile applies up to 35%, reduced to 16% in some cases under the US-Chile tax treaty implemented in 2024. Colombia’s general CIT is 35% plus a dividend distribution tax. Brazil applies 15-22.5% on capital gains, with a flat 15% rate for residents of low-tax jurisdictions. Plan your tax strategy 12-24 months before sale.

Should You Stay On After the Sale?

Yes, most founders stay on for 1-3 years after the sale. The transition agreement and earnout typically require it. Rolling equity gives the founder upside if the buyer scales the business. The handover protects deal value by keeping customer trust and operating knowledge in the business.

How Do You Pick an M&A Advisor?

Pick an M&A advisor with LatAm deal experience and a track record in your size range. The typical succession team includes a CPA, business attorney, valuation professional, and investment banker or business broker. Ask for references from completed founder-led deals in your sector and country.

How Do You Keep the Sale Confidential?

You keep the sale confidential through NDAs, code-named processes, and staged information release. The data room opens to qualified buyers only after a signed LOI and confidentiality agreement. Only the leadership team and outside advisors should know about the process until close approaches.

What Earnout Terms Should You Push For?

Push for revenue earnouts, not EBITDA earnouts, when the buyer controls costs after close. The median earnout outside life sciences is 31% of closing payment. Negotiate a clear formula, a cap on adjustments, and audit rights. Revenue triggers are easier to defend than EBITDA triggers since buyers can suppress EBITDA through reinvestment.

Ready to Plan Your Founder Exit?

The Startup VC is Craig Dempsey’s family office and company builder. Craig built and sold Biz Latin Hub to Vistra in December 2025 after growing the firm across 17 countries. That lived experience drives how we work with founders today. We invest in, partner with, and guide founder-led companies across Latin America. Our goal is exits that protect value and reward the operators who built the business.

If you are thinking about a sale in the next 1-3 years, we can help you prepare. Our team has walked the road, from clean-up to close. Contact us today to discuss your exit. Read more about Craig’s background on the Meet Craig Dempsey page.