Sellers who prepare 12-18 months ahead capture 20-50% higher valuations than unprepared founders in Latin American M&A processes.

Sell side preparation Latin America runs across four tracks: audited financials, normalized working capital, KPI documentation, and legal cleanup. A mid-market Quality of Earnings report takes 3-6 weeks and costs $20,000-$75,000. Brazil accounts for over 60% of regional deal value.

Exit readiness latam is a structured discipline. The Startup VC operates as Craig Dempsey’s family office and company builder across the region. Portfolio company Biz Latin Hub serves 17 Latin American countries. Below, you’ll find the financial cleanup steps, working capital playbook, legal checklist, and sell-side process timeline.

Why Should Founders Prepare a Company for Sale 12-18 Months Before a Transaction?

Founders should prepare a company for sale 12-18 months before a transaction. Early prep drives higher valuations and faster closings. Leading private equity sponsors start sell-side readiness 12 to 18 months before engaging bankers. Unprepared businesses sell for 20-50% lower prices. Buyers price in risk and have less room to negotiate.

The 12-18 month window covers four sequenced workstreams. Each one needs time to mature before buyers see the company.

- Financial cleanup. Moving from tax-basis accounting to GAAP or IFRS takes 12-24 months.

- Management depth. Building a team that can run the business without the founder takes 2-3 years.

- Risk mitigation. Mapping risks and assigning owners requires a clear roadmap with timelines.

- Buyer story. Multi-year contracts and clean KPIs need at least 12 months to stack on the books.

In competitive processes, buyers offer 0.5-1.0x higher revenue multiples for Day 1 integration-ready targets. That single turn of revenue can move enterprise value by millions in a mid-market deal.

What Does Exit Readiness Mean for a Latin American Business?

Exit readiness for a Latin American business means the company can pass institutional buyer diligence cleanly. Buyers complete review without valuation cuts or deal collapse. The Auxo Capital framework groups readiness into four buckets: Finance, Planning, Profit and Revenue, and Operations. A LatAm business adds a fifth bucket. That bucket is cross-border legal and tax compliance.

The regional M&A market shapes what readiness looks like. Brazil drove over 60% of deal value and more than 55% of deal volume in Latin America in 2024. Mexico recorded 268 transactions worth USD 28.1 billion through November 2025. Latin America deal volume rose 1% and value jumped 19% in 2025 versus 2024.

Buyers expect different things by sector and country. The table below shows what regional acquirers want most.

| Buyer Type | Top Priority | Common Deal Killer |

|---|---|---|

| US strategic | Audited financials, IFRS or US GAAP | Tax contingencies, unaudited periods |

| LatAm strategic | Local market share, government contracts | Labor lawsuits, regulatory permits |

| Private equity | Recurring revenue, EBITDA stability | Customer concentration, owner dependence |

| Family office | Predictable cash flow, low capex | Compliance gaps, IP ownership issues |

Brazilian targets with foreign buyers face a specific rule. Share deals of USD 100,000 or more must register with the Central Bank of Brazil (BACEN). Fintech leads sector activity at 24% of all LatAm M&A in early 2025. AI, data, and automation follow at 17%. IT services come in at 13%. For more on regional buyer priorities, see what acquirers look for in Latin American B2B service companies.

How Do You Clean Up Financials Before Selling a Company in Latin America?

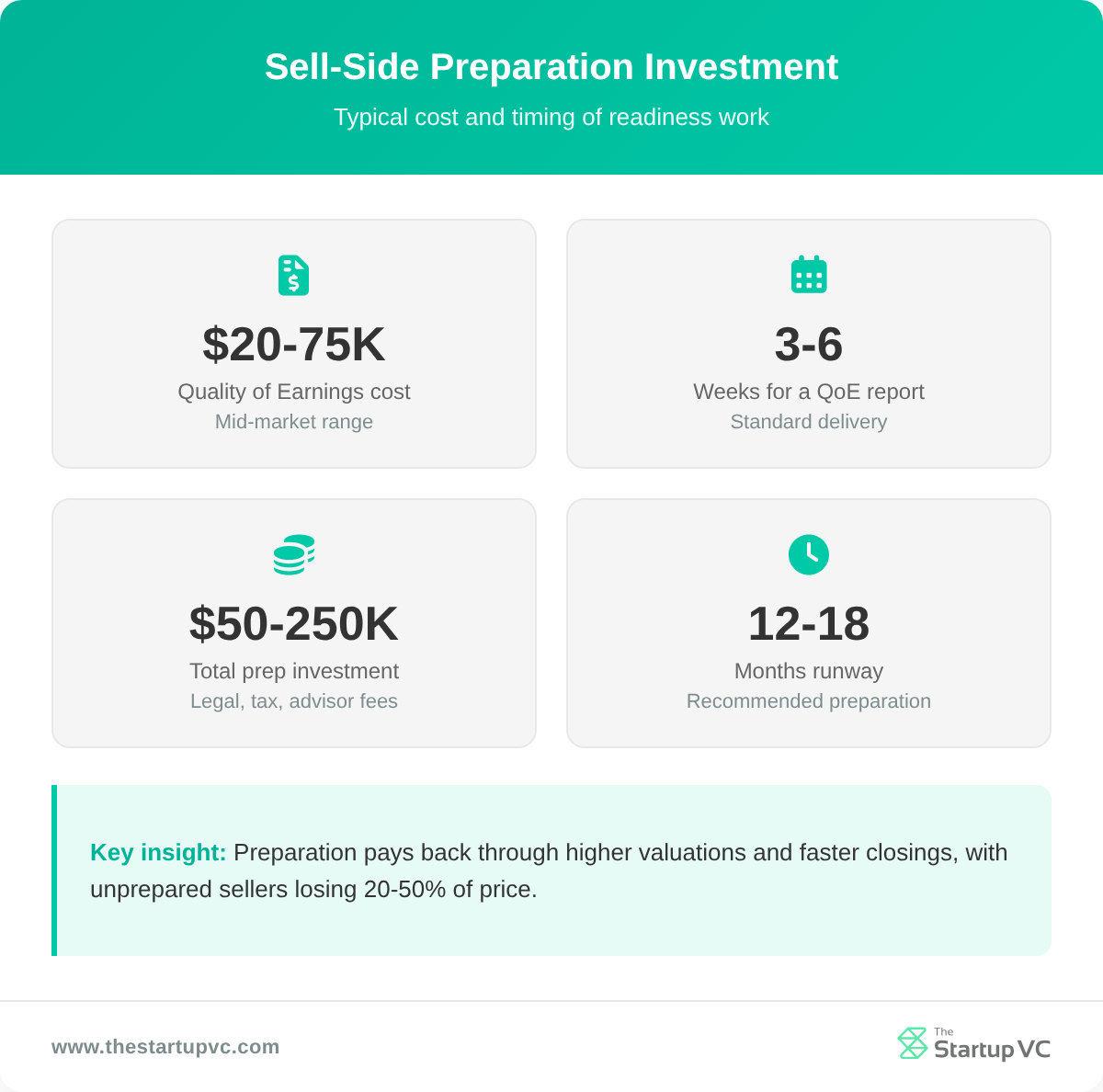

You can clean up financials by commissioning a Quality of Earnings report and converting books to IFRS or US GAAP. You also fix revenue recognition gaps before going to market. A mid-market QoE report takes 3 to 6 weeks. It costs between $20,000 and $75,000. Lower middle market and larger deals run from $60,000 into six figures.

What Is a Quality of Earnings Report and Why Does It Matter?

A Quality of Earnings report is an analysis of EBITDA drivers that strips out one-time items to show normalized earnings. Auditors confirm that statements are accurate. A QoE goes further by adjusting for non-recurring revenue, owner addbacks, and accounting policy changes.

Sell-side QoE reports shorten deal timelines. Buyers often use the seller’s report as the starting point for their own diligence. That reduces the chance of a late-stage valuation reset.

How Do You Convert Books to IFRS or US GAAP?

You can convert books to IFRS or US GAAP by hiring a regional Big Four or boutique accounting firm. The remap of accounts takes 12-24 months. Latin American adoption of IFRS has improved reporting quality. It has reduced earnings management across listed firms.

Country-specific accounting practices still matter. Brazilian and Mexican companies often keep tax-basis books that diverge from IFRS. The conversion process surfaces hidden issues like deferred tax assets, lease accounting, and revenue cut-offs.

LatAm multinationals with international operations produce higher-quality reports than purely local firms. International exposure forces tighter controls and documentation.

What Financial Records Do Buyers Demand?

Buyers demand three years of audited financial statements, monthly management accounts, and a trial balance reconciled to tax filings. They also want bank statements, accounts receivable agings, and inventory listings. Missing any of these triggers extended diligence or a valuation cut.

How Should You Normalize Working Capital and Document KPIs for Buyers?

You should normalize working capital by building a 24-month rolling baseline and defining a working capital peg. You then package operating metrics into a buyer-ready KPI cohort. Normalized working capital strips out one-time events, seasonal swings, and accounting anomalies. The result becomes the basis for purchase price adjustments at close.

How Do You Set a Working Capital Peg?

You can set a working capital peg by averaging 12 to 24 months of net working capital. You then adjust for seasonality. Most M&A deals include a closing adjustment. That adjustment compares delivered working capital against the agreed target. If you deliver less, the price drops dollar-for-dollar.

The most dispute-resistant approach is a three-document package. It contains a one-page NWC bridge and a policy memo tied to the QoE. The package also includes a worked example mirroring the buyer’s closing statement template.

Which KPIs Should You Track and Document?

You should track and document the KPIs that buyers will ask for in diligence. The list below covers the metrics that move valuation in LatAm B2B deals.

- Monthly recurring revenue and growth rate. Show 24 months of MRR by cohort.

- Customer concentration. Report top 10 customers as percent of revenue.

- Gross retention and net revenue retention. Track both annually and by cohort.

- Customer acquisition cost and payback period. Tie to channel and region.

- EBITDA margin by segment. Split by country, product, or customer type.

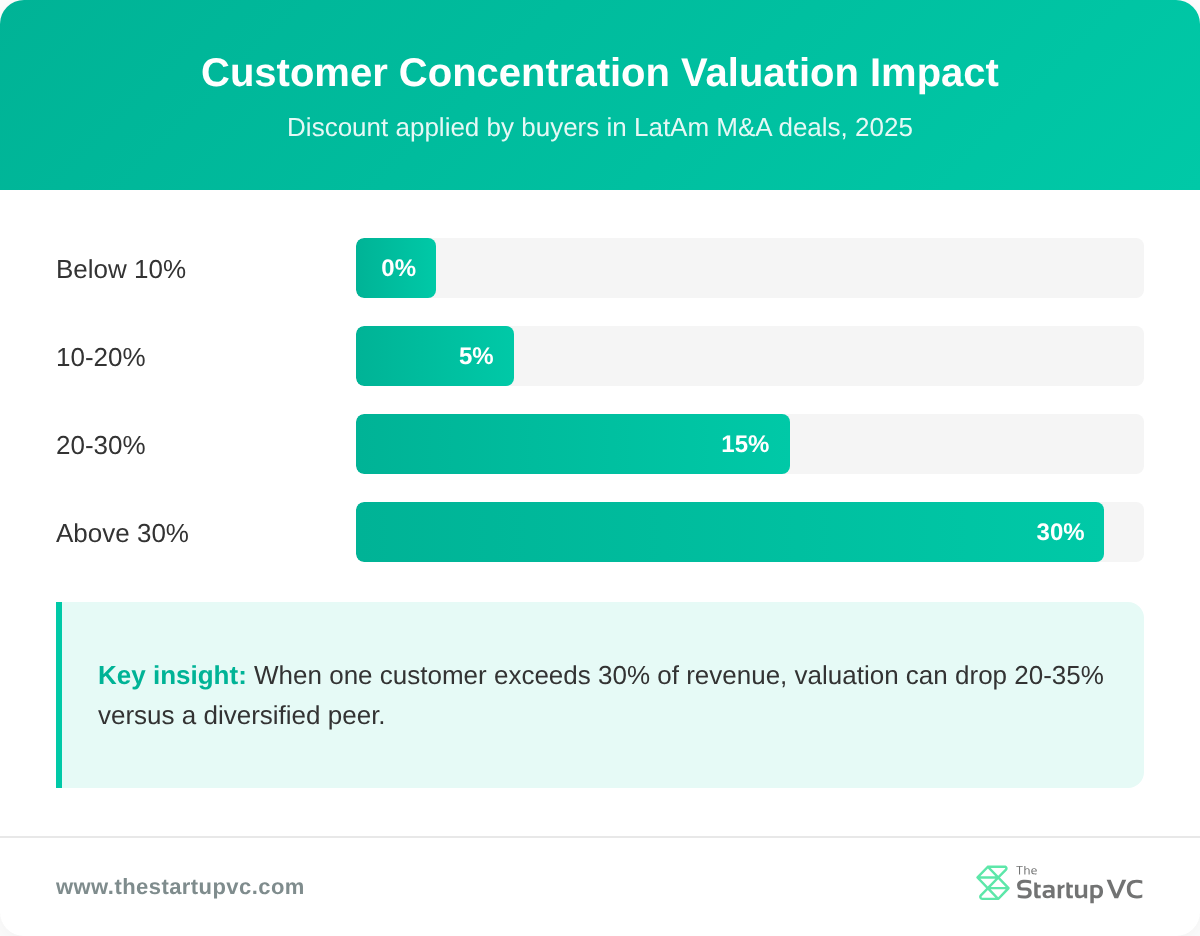

How Does Customer Concentration Affect Valuation?

Customer concentration affects valuation directly. When a single customer exceeds 30% of revenue, valuation can drop 20-35% versus a diversified peer. The table below shows the discount structure that LatAm buyers apply.

| Top Customer Share | Buyer Reaction | Valuation Impact |

|---|---|---|

| Below 10% | Clean profile, buyers compete | No discount |

| 10-20% | Diligence questions, manageable | Minimal discount |

| 20-30% | Yellow flag, deal structure shifts | 10-20% compression |

| Above 30% | Red flag, many PE firms pass | 20-35% discount or earnout |

If comparable businesses trade at 5.5x EBITDA, a concentrated company may trade at 4.5x to 5x. That single turn difference can be millions in enterprise value. Lock in multi-year contracts with large clients 6 to 12 months before going to market. This converts open-ended concentration risk into a defined window.

Latin American companies face greater working capital uncertainty than developed-market peers. Currency volatility, customer payment delays, and inventory swings all distort the baseline. A clean 24-month dataset filters out the noise.

What Legal, Tax, and Compliance Issues Must You Fix Before Going to Market?

You must fix labor contingencies, tax exposures, IP ownership gaps, and regulatory permit issues before going to market. Brazil and Mexico have complex labor regimes. Local counsel is essential for cleaning up legacy claims and worker classification questions.

Brazil’s tax system is undergoing the largest overhaul in decades. A unified dual VAT system is rolling out from 2026 to 2033. It replaces federal, state, and municipal indirect taxes. Brazilian targets must analyze recurring tax compliance costs, effective tax rate shifts, and contingent liabilities. All three affect deal pricing and risk allocation.

The legal cleanup checklist below covers the issues that most often delay LatAm sale processes.

- Labor contingencies. Audit pending claims, severance accruals, and worker classification.

- Tax exposures. Quantify open assessments, transfer pricing positions, and VAT credits.

- IP ownership. Confirm that all code, trademarks, and patents sit with the operating entity.

- Regulatory permits. Verify environmental, sector-specific, and operating licenses are current.

- Cross-border structure. Map the holdco-opco chain and tax treaty access for the buyer.

A second phase of Brazilian tax reform targets corporate income tax and dividend taxation. It could change deal structures and valuations once implemented. Sellers in Brazil should model both pre-reform and post-reform tax outcomes for buyers.

Anti-bribery compliance has become a standard diligence focus. Both Brazil and Mexico have evolving anti-corruption rules. Buyers expect documented controls, training records, and clean third-party screening logs. Founders should also review the broader regional exit landscape. The LatAm exits problem shapes how acquirers price risk across the region.

How Do You Build a Sell-Side Process That Attracts Strategic and Financial Buyers?

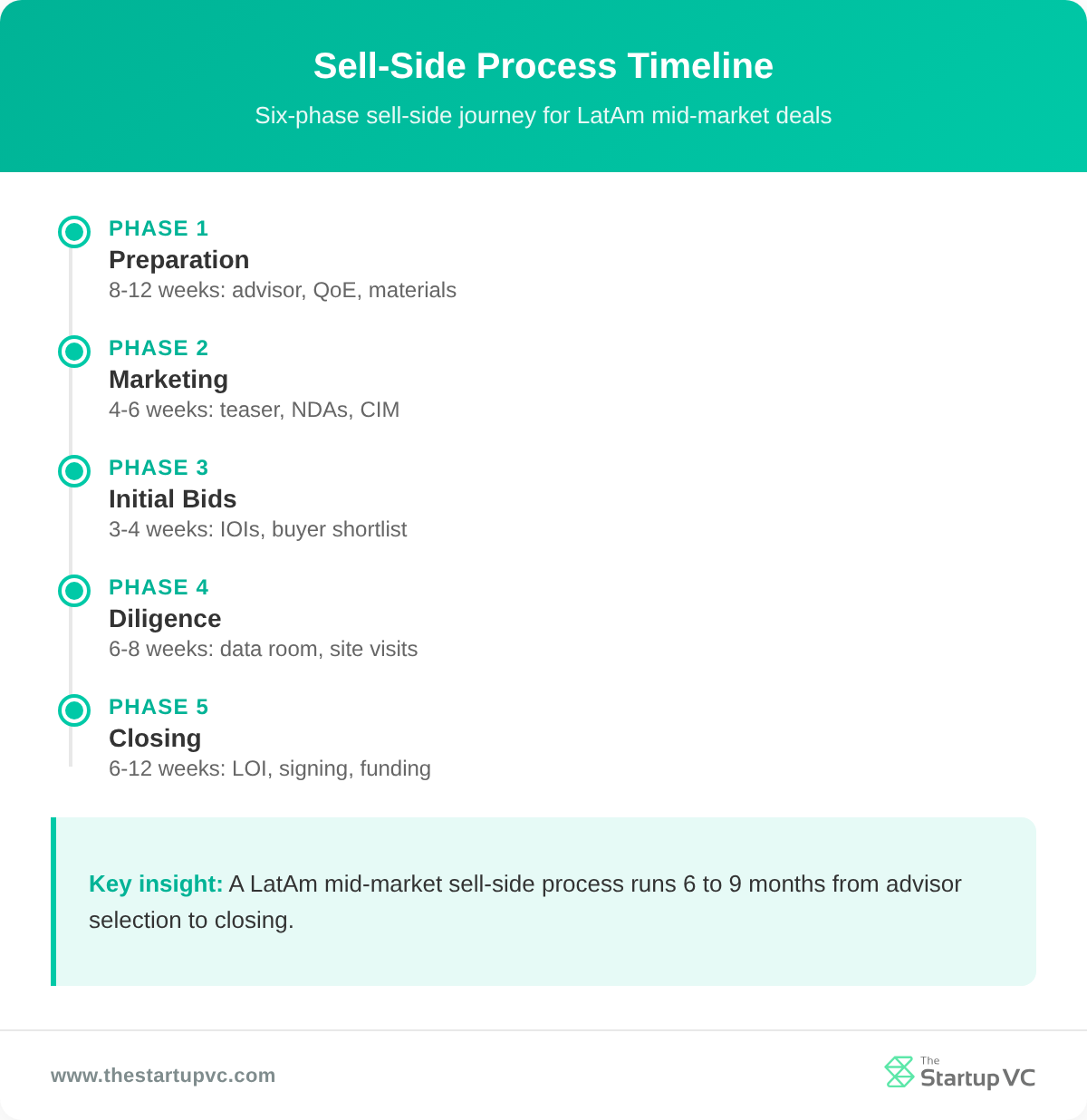

You can build a sell-side process by hiring an advisor and preparing a teaser and CIM. You then structure a data room and run a competitive auction. The process moves through four gated stages. Each layer of disclosure matches deeper buyer commitment.

What Is the Sell-Side Process Timeline?

The sell-side process timeline runs 6 to 9 months from launch to close in most LatAm mid-market deals. The phased breakdown below shows where time goes.

| Phase | Activity | Duration |

|---|---|---|

| Preparation | Advisor selection, QoE, materials | 8-12 weeks |

| Marketing | Teaser distribution, NDAs, CIM | 4-6 weeks |

| Initial bids | Indication of interest, buyer shortlist | 3-4 weeks |

| Diligence | Data room, management meetings, site visits | 6-8 weeks |

| Negotiation | LOI, definitive agreement, signing | 4-6 weeks |

| Closing | Regulatory approvals, funding | 2-6 weeks |

How Do Investment Banks Drive Competitive Bidding?

Investment banks drive competitive bidding by building a target list of strategic and financial buyers. They run those buyers in parallel through synchronized deadlines. The teaser is a 5-page document sent before any NDA. The CIM follows after NDA execution. The data room opens for shortlisted bidders.

All interested buyers submit initial bids at the same time. That synchronized deadline generates pressure. It also gives the banker options on price and structure.

The investment bank picks buyers by industry fit, strategic alignment, and financial capability. US investors regained the top spot as the main acquirer of Latin American M&A targets in 2025. Strategic acquirers from the US, Spain, and within LatAm now compete actively for regional B2B targets. To see how regional exits structure, read how to structure a startup exit in Colombia.

What Should Go Into the Data Room?

The data room should include the items in the list below. These are the documents buyers will demand before submitting a binding bid.

- Three years of audited financials and management accounts

- Quality of Earnings report and working capital analysis

- Customer contracts with the top 20 accounts

- Employee roster with comp, tenure, and key person agreements

- Legal entity charts, cap tables, and shareholder agreements

- Tax filings, assessments, and transfer pricing documentation

- Material contracts, leases, and IP registrations

- Regulatory licenses, permits, and compliance records

What Questions Do Founders Ask Most Often About Preparing a Company for Sale?

How Long Does Sell-Side Preparation Take in Latin America?

Sell-side preparation takes 12-18 months for a full readiness program in Latin America. A faster 3-6 month sprint can work if the company already has audited financials. The longer runway materially improves valuation and time to close.

How Much Does Sell-Side Preparation Cost?

Sell-side preparation costs $50,000 to $250,000 for a typical LatAm mid-market deal. The Quality of Earnings report alone runs $20,000-$75,000. Legal cleanup, tax structuring, and advisor retainers make up the rest. The investment pays back through higher valuation and fewer surprises in diligence.

What Is the Biggest Mistake Founders Make Before Selling?

The biggest mistake founders make is starting too late. Founders with messy financials, customer concentration above 30%, or unresolved legal claims sell for 20-50% below peers. Starting 12-18 months early prevents this.

Should You Use an Investment Bank or Sell Directly?

You should use an investment bank for any LatAm deal above USD 10 million in enterprise value. Banks run competitive processes that generate multiple bids. They also handle confidentiality, buyer screening, and negotiation. Direct sales work for smaller deals or when a single strategic buyer has already approached.

How Do You Keep a Sale Confidential?

You can keep a sale confidential by signing NDAs before sharing the CIM. You also limit data room access to named buyer team members and avoid identity disclosure in the teaser. The four-layer gating system controls who sees what. Leaks usually come from employees, so brief only the executives who must know.

What Happens to the Founder After Closing?

The founder usually stays on for 6-24 months after closing under a transition services agreement. Buyers often require an earnout tied to revenue or EBITDA targets. The earnout shifts post-close risk to the seller. It keeps the founder motivated to hit numbers.

Ready to Prepare Your Latin American Company for a Successful Sale?

The Startup VC is Craig Dempsey’s family office and company builder, creating and backing scalable ventures across Latin America. We work with founders on sell-side preparation, drawing on operational experience from our portfolio investments across the region. Our team brings hands-on M&A experience from real LatAm transactions, including portfolio company exits.

If you are 6-24 months from a sale, we can scope your financial cleanup, working capital, and KPI packaging. Contact us today to plan your exit readiness with Craig Dempsey and the team.