Selling a professional services firm in Latin America can deliver 0.7x to 4.5x EBITDA, with global buyers like Vistra and TMF Group active.

Latin America recorded around 2,650 M&A deals worth nearly $96 billion in the first 11 months of 2025. Total deal value rose 13% year over year. Strategic acquisitions drive 67% of VC-backed exits in the region.

The Startup VC is Craig Dempsey’s family office and company builder. Craig sold Biz Latin Hub to Vistra in December 2025 after scaling it across 17 countries. Below, you will find buyer profiles, valuation benchmarks, the sell-side process, deal structures, and FAQs from founders preparing their own exit.

What Is a Professional Services Company Exit in Latin America?

A professional services exit is the sale of an accounting, legal, BPO, payroll, corporate secretarial, or tax firm to a strategic buyer, private equity platform, or family office. The exit converts founder equity into cash, rollover stock, or earn-out payments.

Latin America’s M&A market hit nearly $96 billion in deal value through November 2025. Deal count was around 2,650 transactions. Total value rose 13% year over year despite a small dip in deal volume. This signals a “quality over quantity” shift toward larger, more professional deals.

The region’s professional services sector draws strong buyer demand for three reasons. Firms generate predictable, recurring revenue. Margins are stronger than industrial sectors. Capital needs are lower than asset-heavy businesses.

| LatAm Exit Path | Share of VC-Backed Exits | Typical Timeline |

|---|---|---|

| Strategic acquisition | 67% | 8 to 15 years |

| Secondary sale | 27% | 5 to 10 years |

| IPO or public listing | 6% | 10 to 20 years |

The average time from founding to M&A exit in Latin America is 11.9 years. This is longer than the US benchmark. Founders must plan their exit window carefully. Read our deeper view on the LatAm exits problem for context on regional liquidity trends.

Who Buys Professional Services Firms in Latin America?

The most active buyers are global corporate services consolidators, US-based BPO acquirers, regional roll-up platforms, and family offices. Each buyer type pays different multiples and structures deals differently.

Five recent transactions show the buyer landscape clearly:

- Vistra acquired Biz Latin Hub in December 2025, gaining 17 countries and 36 partner firms. Vistra now sits as a top-four global payroll provider.

- Grant Thornton US acquired Auxis, a Fort Lauderdale BPO firm with 1,400 staff. Auxis operates across Costa Rica, Colombia, Mexico, and Guatemala.

- TMF Group acquired KMC Campos y Campos and Matas Lorenzo in Mexico. The deal expanded TMF’s accounting, tax, and payroll capacity.

- Auxadi acquired Resolve BPO, adding offices across Costa Rica, Guatemala, Nicaragua, Honduras, El Salvador, and Panama.

- Vistra also acquired iiPay before the Biz Latin Hub deal. This built scale in global payroll.

US buyers led inbound LatAm M&A activity. They accounted for 30% of deal value and a third of deal volume. France, China, and Switzerland followed as the next largest acquirer countries.

Buyer profiles fall into four categories:

- Global corporate services consolidators. Vistra, TMF Group, and Auxadi buy regional firms to expand country coverage.

- Big Four and mid-tier accounting firms. Grant Thornton, BDO, and RSM acquire to add nearshore delivery capacity.

- Private equity roll-up platforms. PE-backed groups in the US and Spain buy multiple LatAm firms to build pan-regional brands.

- Family offices and strategic operators. Craig Dempsey’s The Startup VC backs and exits service ventures across the region.

How Much Is a Professional Services Firm Worth in Latin America?

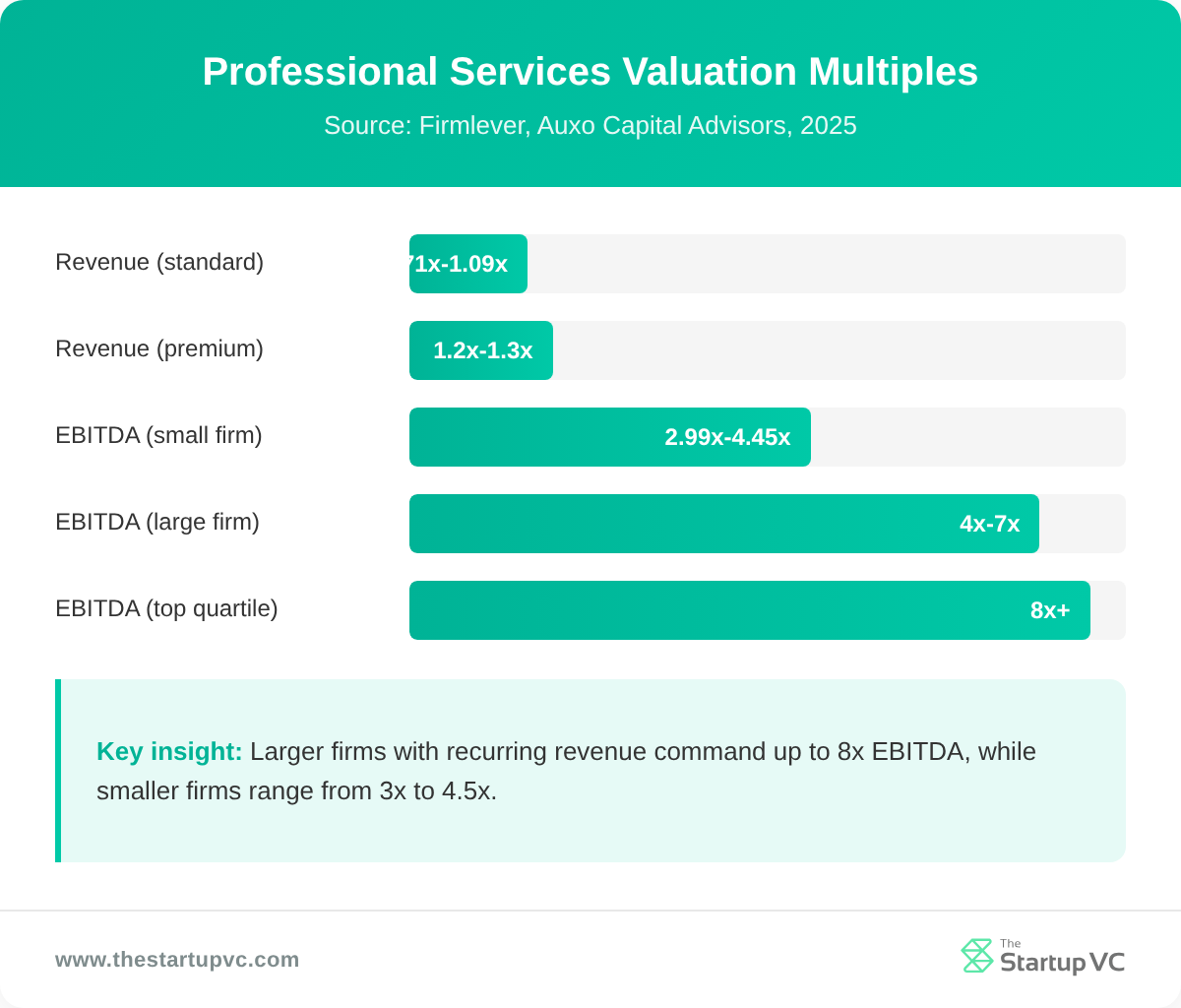

A professional services firm in Latin America is worth 0.7x to 1.3x annual revenue or 3x to 7x EBITDA. Size, recurring revenue mix, and growth set the final multiple. Larger firms with sticky compliance books command the top of these ranges.

Three benchmarks anchor most valuations:

| Multiple Type | Typical Range | Top Quartile | Driver |

|---|---|---|---|

| Revenue multiple | 0.71x to 1.09x | 1.2x to 1.3x | Recurring compliance work |

| EBITDA multiple (small firm) | 2.99x to 4.45x | 5.0x+ | Owner-replacement cost |

| EBITDA multiple (large firm) | 4x to 7x | 8x+ | Scale and growth visibility |

Recurring revenue is the single biggest value lever. Firms with 80% or more recurring revenue earn 0.2x to 0.4x higher multiples than peers with project-based revenue. Buyers pay this premium because retention reduces post-close risk.

A formal sell-side process also lifts price. Firms that take an off-market offer often land at 4x EBITDA with backloaded terms. A competitive auction can push the same firm to 6x-8x+ EBITDA with more cash at close.

Other value drivers include client concentration below 15%, partner depth beyond the founder, advisory mix above 20% of revenue, and clean AR aged under 60 days. Weak scores on these metrics drag valuation down by up to a full turn of EBITDA.

For deeper buyer-side criteria, see our guide on what acquirers look for in Latin American B2B service companies.

What Are the Main Steps to Sell a Professional Services Company in Latin America?

You can sell a professional services company in Latin America by following a six-stage sell-side process. The full timeline runs 6 to 12 months from kickoff to close.

The process has six steps:

- Step 1: Pre-marketing prep. Build clean three-year audited financials, normalize EBITDA, and prepare a quality of earnings report. Address client concentration and partner risk before going to market.

- Step 2: Advisor selection. Hire an M&A advisor or boutique investment bank with LatAm professional services experience. Negotiate fees, retainer, and tail period.

- Step 3: Buyer outreach. The advisor builds a targeted buyer list of 30 to 80 names. Strategic buyers, PE platforms, and family offices receive a teaser and CIM.

- Step 4: Indication of interest. Interested buyers submit non-binding bids with valuation range and structure. Sellers shortlist 3 to 6 buyers for management meetings.

- Step 5: Due diligence and LOI. A lead bidder signs a letter of intent. Diligence covers financial, legal, tax, commercial, and HR areas over 60 to 90 days.

- Step 6: Signing and closing. Final purchase agreement, working capital peg, escrow, and reps and warranties insurance get negotiated. Regulatory and antitrust clearance trigger closing.

Pre-engagement matters as much as process. The Vistra-Biz Latin Hub deal closed after a multi-year affiliate partnership that began around 2018. Strategic buyers often pre-qualify targets through commercial relationships before bidding.

Cross-border deals in Brazil add complexity. Sellers must navigate indirect transfer rules, treaty protections, and anti-abuse measures. Mexico and Colombia have similar though less burdensome rules.

Founders should also prepare for diligence requests on data privacy, anti-corruption controls, and tax residency of holdcos. Buyers in 2025 weigh ESG and compliance gaps heavily.

Learn more about Craig Dempsey’s journey building and selling Biz Latin Hub on his founder profile.

How Do You Structure a Professional Services M&A Deal in LatAm?

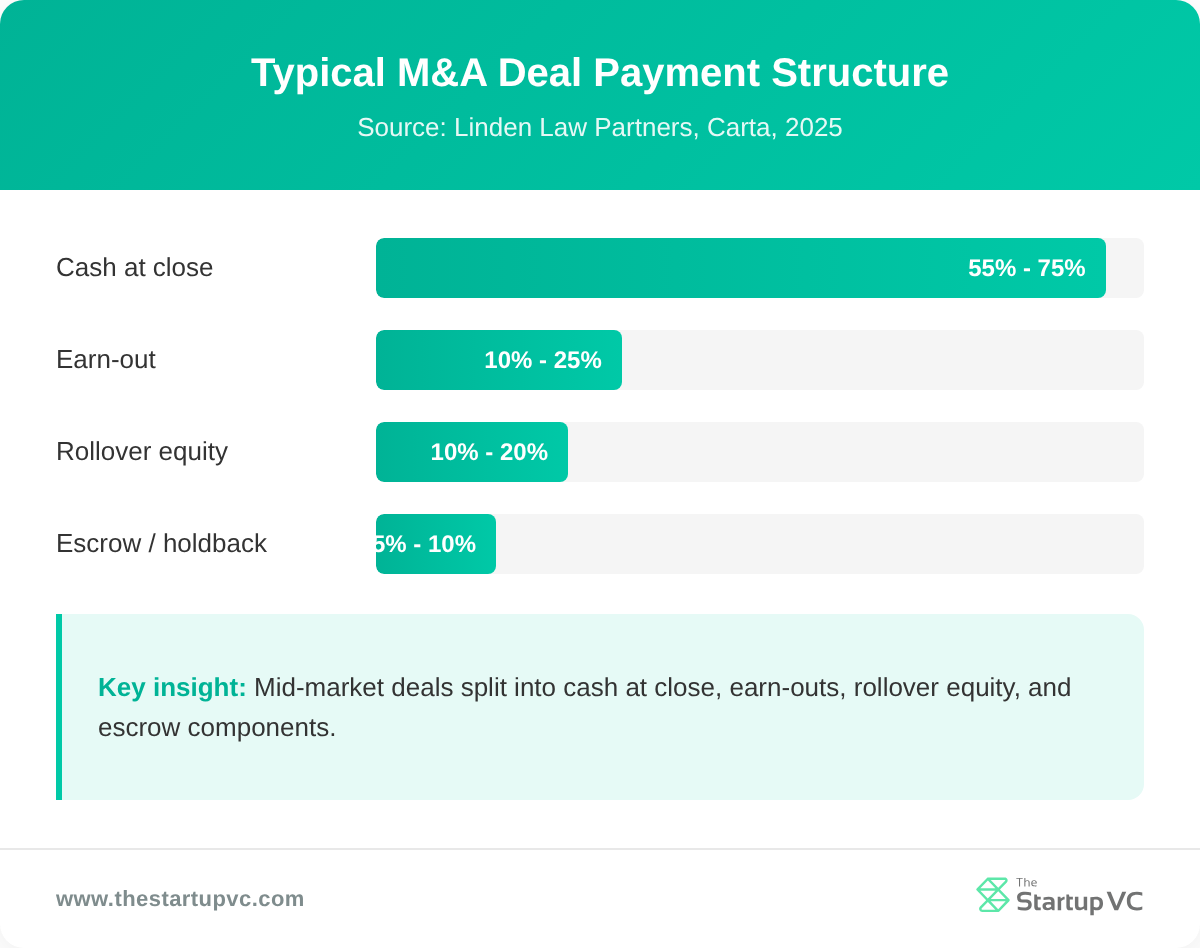

You structure a LatAm professional services deal by combining cash at close, earn-outs, rollover equity, working capital adjustments, and tax-efficient holdco routing. Mid-market deals rarely close on 100% cash.

A typical payment mix looks like this:

| Component | Share of Purchase Price | Purpose |

|---|---|---|

| Cash at close | 55% to 75% | Founder liquidity |

| Earn-out | 10% to 25% | Performance retention |

| Rollover equity | 10% to 20% | Founder alignment, second bite |

| Escrow or holdback | 5% to 10% | Indemnity coverage |

Earn-outs typically run 2 to 3 years against revenue or EBITDA targets. They carry execution risk for the seller, so terms matter. Sellers should push for clear, auditable targets and avoid buyer-controlled accounting changes.

Rollover equity gives founders a stake in the post-close platform. The rollover stock can grow if the buyer scales the platform and exits to a larger PE firm or strategic buyer. Founders who rolled equity in Vistra-style deals often see strong second-bite value at the platform exit.

Tax-efficient structuring is critical. Most cross-border deals route through Spanish, Dutch, or Delaware holdcos. These structures access treaty benefits in Brazil, Mexico, and Colombia. This can save 10% to 25% in withholding taxes on consideration paid.

Other deal mechanics now standard in mid-market LatAm professional services deals:

- Working capital peg. A target net working capital is set, with dollar-for-dollar adjustment at close.

- Reps and warranties insurance. Replaces large escrows and shifts indemnity risk to insurers.

- Transition services agreement. The seller stays 12 to 36 months to keep clients and run the operational handover.

- Non-compete and non-solicit. Standard 2 to 5 year scope across LatAm jurisdictions where the business operates.

For an inside look at how Vistra structured the Biz Latin Hub deal, read Biz Latin Hub Exit.

What Questions Do Founders Ask Most Often About Selling a Professional Services Firm?

When Is the Best Time to Sell a Professional Services Firm in Latin America?

The best time to sell is when revenue growth, recurring revenue mix, and partner depth are all strong. Buyers pay top multiples for firms with 20%+ growth, 80%+ recurring revenue, and a deep bench. Selling at a peak earns the highest multiple.

How Much Do M&A Advisor Fees Cost in Latin America?

M&A advisor fees on mid-market LatAm deals usually run 3% to 8% of transaction value. Most advisors also charge a monthly retainer of $5,000 to $25,000. Larger deals carry lower percentage fees. Boutique firms with sector expertise often outperform big-name banks on outcome.

How Long Does It Take to Sell a Professional Services Firm?

A professional services firm sale takes 6 to 12 months from kickoff to close. Preparation adds another 3 to 6 months before kickoff. Founders should plan 12 to 18 months total when factoring in pre-marketing work.

Can Founders Stay in the Business After the Sale?

Yes, founders typically stay 12 to 36 months post-close under a transition services agreement. This keeps clients, staff, and earn-out targets aligned. Many founders also keep rollover equity in the platform.

What Tax Planning Is Needed Before Selling?

Tax planning typically starts 12 to 24 months before signing to optimize capital gains treatment. Common tools include holdco restructuring, treaty-protected entities, and timing of dividend versus capital gain treatment. Local tax advice is essential in Brazil, Mexico, and Colombia.

What Happens to Employees After a Professional Services Acquisition?

Most strategic buyers retain key employees and add junior staff to the new platform. Earn-outs and retention bonuses often tie key partners to the buyer for 2 to 3 years. Layoffs typically focus on duplicate back-office functions rather than client-facing teams.

Ready to Exit Your Professional Services Company in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder. We back, build, and exit B2B service ventures across Latin America. Craig sold Biz Latin Hub to Vistra in 2025 after scaling it to 17 countries.

We work with founders preparing for an exit, planning a roll-up, or seeking capital and operational support. Our regional teams cover accounting, legal, payroll, and corporate services across Mexico, Colombia, Brazil, Chile, and beyond.

Contact us today to discuss your exit path or learn more about our investment focus.