Structuring a cap table for cross-border investors requires choosing between Delaware and Cayman: 47.7% of LatAm unicorns choose Cayman.

A cross-border cap table must track equity across multiple legal entities. It must also comply with FATCA, OFAC, and country-specific requirements. Delaware C-Corps work for US-focused raises. Cayman Islands structures protect LatAm founders at exit.

The Startup VC has worked with founders across Colombia, Brazil, and Mexico to structure cross-border equity. Craig Dempsey’s team navigates entity choices, SAFE agreements, and compliance requirements for international investors. Below, you will find step-by-step guidance on cap table setup, investor rights, and tax rules for your international shareholders.

What Is a Cap Table and Why Does It Matter for International Fundraising?

A cap table is a financial record that tracks equity ownership in a company. It lists every stakeholder’s name, share count, share class, ownership percentage, and vesting schedule. It is the single source of truth for who owns what and on what terms.

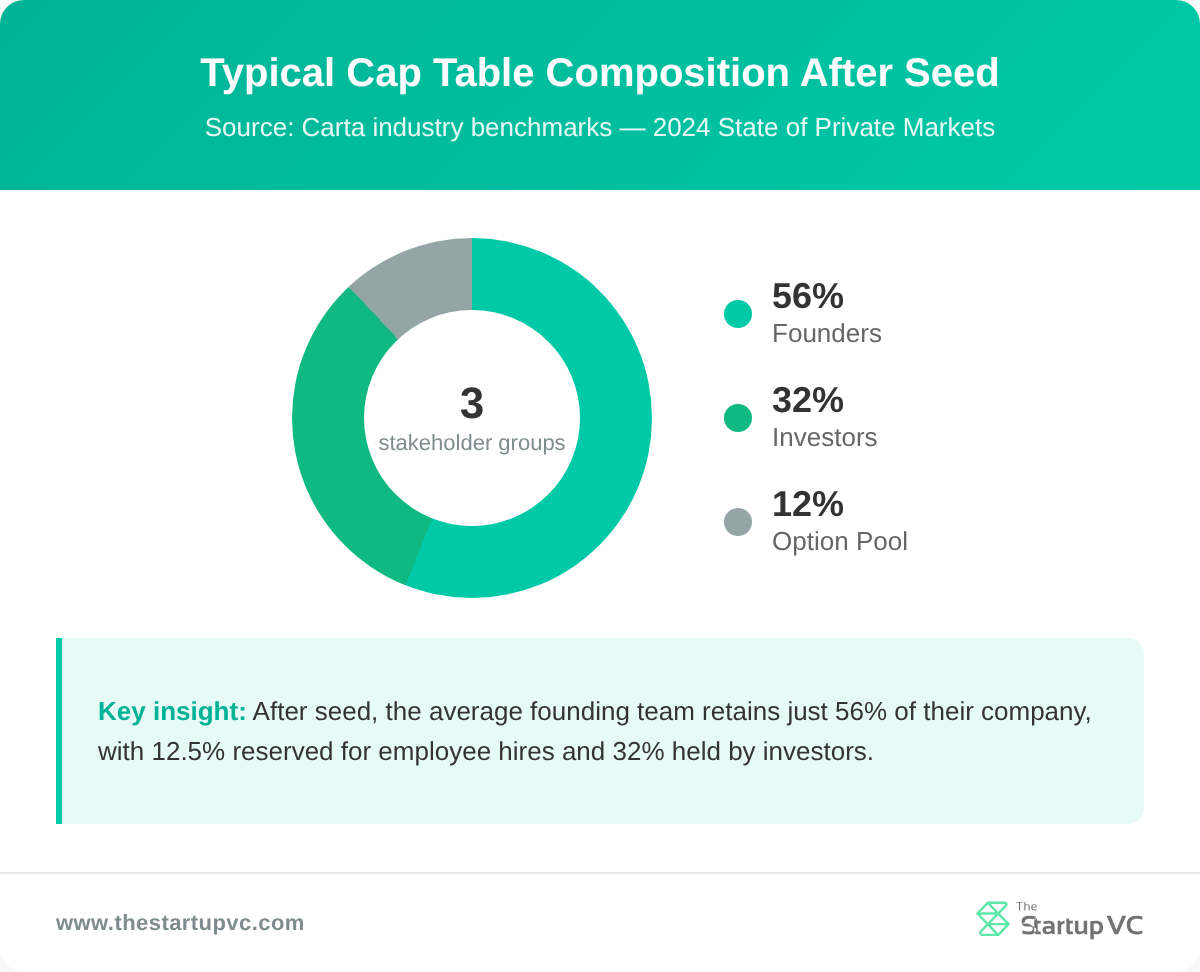

Cap tables organize stakeholders into four main groups:

- Founders hold common stock, typically issued at incorporation.

- Investors hold preferred stock, organized by funding series.

- Employees and advisors hold stock options that vest over time.

- Unallocated option pool holds shares reserved for future hires.

Based on analysis of 20,000+ equity programs, employee option pools typically represent 14–21% of fully diluted shares. Seed-stage pools average 12.5% (Carta Q4 2023 data). Series A pools are usually set at 10–12%.

Venture capital investors request the cap table early in due diligence. They look for three red flags: over-diluted founders, unresolved SAFEs, and dead equity. Dead equity is stock held by inactive co-founders who no longer contribute. Industry benchmarks expect founders to sell 20–35% at Series A. A cap table already below that threshold can stall a deal.

Best-practice cap tables limit direct investor entries to 10–15 names. More entries create governance problems. Getting approval from 30 separate angels for any board decision signals poor organization. Special purpose vehicles (SPVs) consolidate angel investors into a single cap-table line.

What Does Cross-Border Investment Add to a Cap Table?

Cross-border investors add four compliance layers to your cap table. Managing each layer requires extra documentation and legal review.

- OFAC sanctions screening. Every foreign investor must be checked against the U.S. Treasury’s Specially Designated Nationals list before you accept their capital.

- KYC and AML verification. Financial institutions spent more than $274 billion on compliance globally in 2024. Cross-border deals require verification across multiple jurisdictions.

- Foreign ownership caps. Some countries limit how much foreign investors can own. Brazil limits foreign ownership in mass media companies to 30%.

- Beneficial ownership reporting. FinCEN’s March 2025 rule requires foreign-formed entities doing business in the U.S. to disclose all non-U.S. beneficial owners.

What Legal Entity Structure Should You Use for Cross-Border Investment?

You should choose a legal entity based on your investors’ requirements, home country, and exit plans. The four main options are a Delaware C-Corp, a Cayman holding company, a BVI company, or an SPV.

Delaware C-Corps dominate VC-backed startups. Approximately 88% of C-corp startups on PitchBook were Delaware-incorporated in late 2024. Delaware also hosted 81.4% of all U.S.-based IPOs in 2024.

The table below compares the four most common structures for founders raising cross-border capital.

| Structure | Setup Cost | Tax on Exit | Best For |

|---|---|---|---|

| Delaware C-Corp | $500–$2,000 | 21% US corporate tax | US-focused fundraising |

| Cayman Sandwich | $5,000–$15,000 | 0% at Cayman level | LatAm founders, global VCs |

| BVI HoldCo | $2,000–$5,000 | 0% corporate/capital gains | Simple cross-border holding |

| SPV (Delaware LLC) | ~$8,000 per SPV | Pass-through for US partners | Syndicating co-investors |

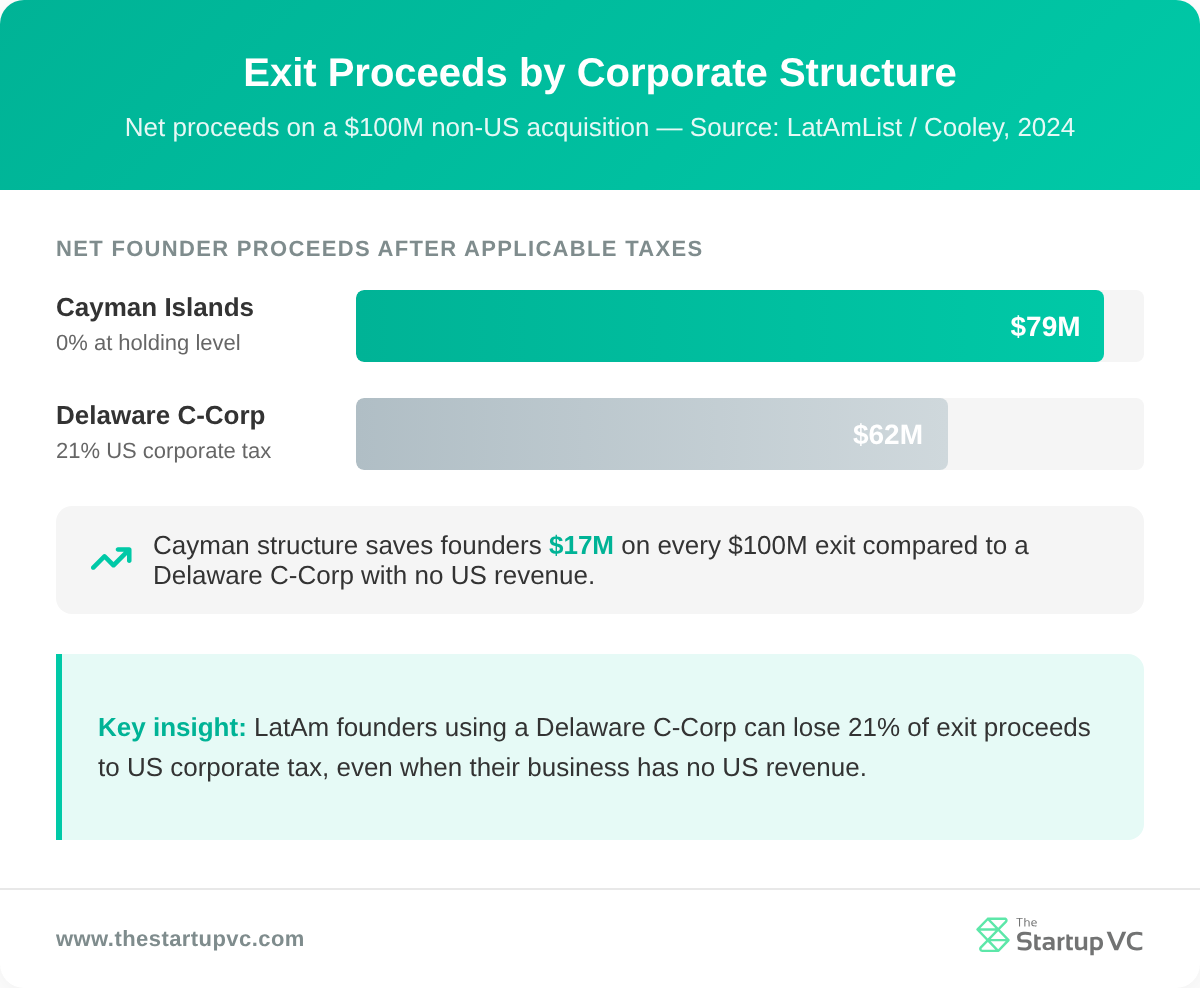

Choosing a Delaware C-Corp over a Cayman structure carries real exit-tax risk. On a $100M non-US acquisition, a Delaware C-Corp nets approximately $62M after 21% US corporate tax. The same exit through a Cayman structure returns approximately $79M. Vivareal co-founder Brian Requarth has stated his company paid over $100M to the US government despite having zero US revenue.

What Is the Delaware Flip and When Should You Use It?

The Delaware flip restructures a foreign company into a wholly-owned subsidiary of a new US parent. It places a Delaware C-Corp as the top holding entity. Legal fees run $15,000–$25,000 for straightforward cases. Complex cases with prior priced rounds can cost six figures.

You should do a flip before closing your first institutional equity round. After a priced round closes, the flip may be legally infeasible. Brazil is the most difficult LatAm jurisdiction for this process. Brazilian corporate income tax on capital gains from a share exchange is 34%. The Receita Federal can treat a share-for-share exchange as a taxable event rather than a tax-neutral reorganization.

When Does a Cayman Islands Structure Make More Sense?

The Cayman Islands structure works better for founders planning large-scale global raises. As of 2022, 47.7% of all LatAm unicorns use a Cayman Islands holding company. The most common form is the Cayman Sandwich. A Cayman exempted company holds a Delaware LLC, which owns the local operating entity.

Nubank shows how this structure works at scale. Nu Holdings Ltd. incorporated in the Cayman Islands in February 2016. It raised capital from Sequoia, Tiger Global, and Berkshire Hathaway. It IPO-d on the NYSE in December 2021 at a $52 billion valuation. The Cayman Sandwich let Nubank raise from global and US investors. It also kept exit proceeds outside US corporate tax jurisdiction.

Learn more about where venture capital is going in Latin America.

How Do Share Classes and Investor Rights Work for Foreign Shareholders?

Share classes and investor rights work by dividing equity into preferred and common stock. Each class carries different economic and governance rights. Foreign shareholders typically hold preferred stock, which comes with stronger protections than common stock.

Startups issue common stock to founders and employees. They issue preferred stock to investors by funding series. Preferred stock sits ahead of common stock in the payout order at exit.

How Do Liquidation Preferences and Anti-Dilution Rights Work?

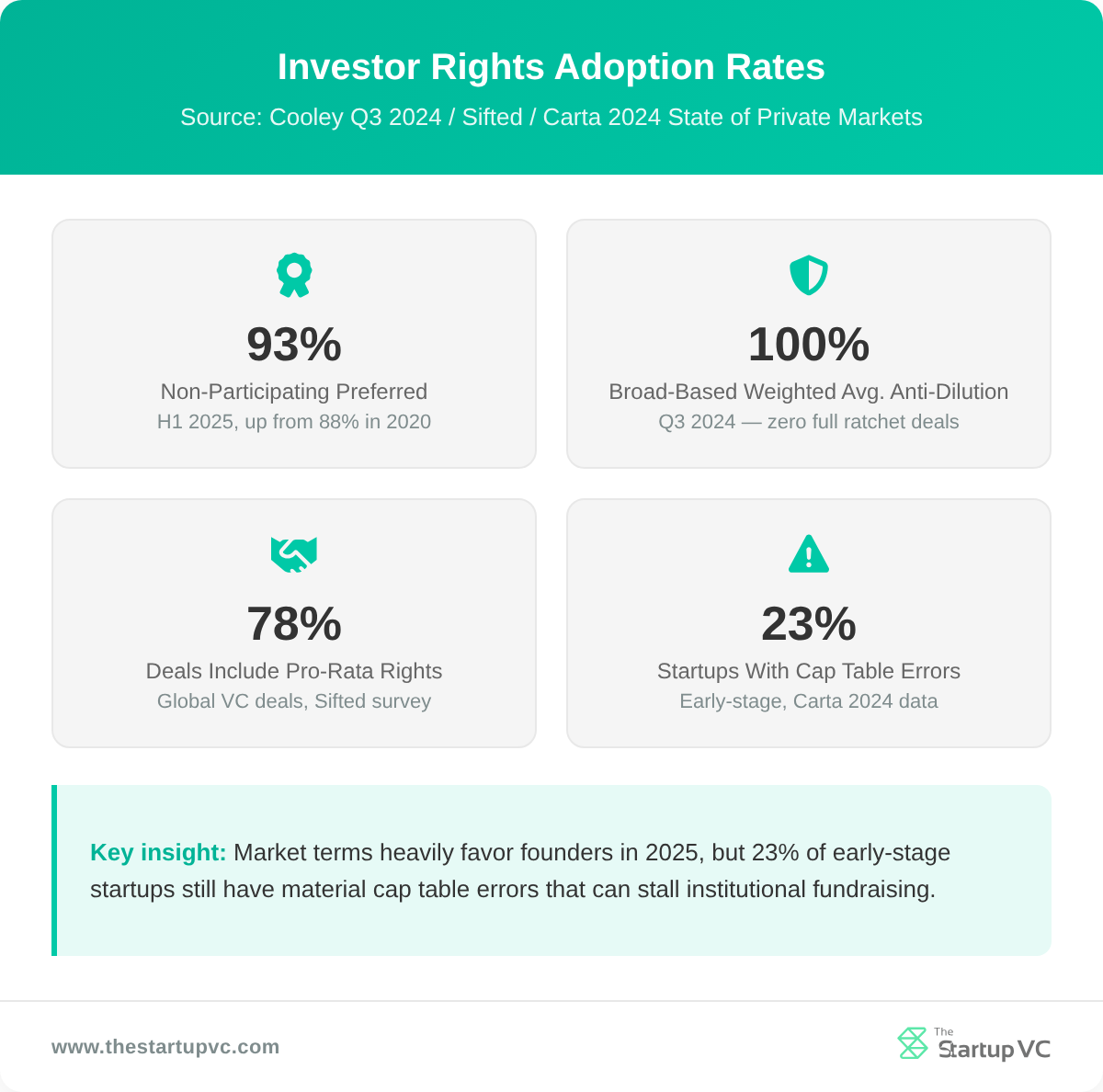

Liquidation preferences work by setting the payout order when a company is acquired. The 1x non-participating preferred structure is the current market standard. As of H1 2025, 93% of VC deals use non-participating preferred, up from 88% in 2020.

Under a 1x non-participating structure, investors receive the greater of two amounts:

- Their original investment returned in full, or

- Their pro-rata share of total proceeds

They do not receive both. Participating preferred gives investors their investment back and a share of remaining proceeds. That structure is less favorable for founders.

Anti-dilution protection guards investors against down rounds. In Q3 2024, 100% of US venture deals used broad-based weighted average anti-dilution. This was the first time in Cooley’s reporting history that zero deals included full ratchet provisions. Broad-based weighted average uses the fully diluted share count to recalculate the conversion price. This makes down-round adjustments less punishing for founders.

What Are Pro-Rata, Information, and Drag-Along Rights?

Pro-rata, information, and drag-along rights are investor protections that govern equity participation, reporting access, and exit decisions. Each right is typically negotiated in the term sheet and formalized in the Investors’ Rights Agreement.

Pro-rata rights let investors maintain their ownership percentage in future rounds. They appear in roughly 78% of VC deals globally. Companies typically set a 5% ownership threshold to qualify as a Major Investor with pro-rata participation.

The NVCA updated its Investors’ Rights Agreements in October 2024. Under these agreements, Major Investors invest $1–2 million or more at Seed stage. They receive formal reporting rights as shown below.

| Report | Deadline |

|---|---|

| Quarterly unaudited financials | Within 45 days of quarter-end |

| Annual financials | Within 90–120 days of fiscal year-end |

| Monthly income statements | Within 30 days of month-end |

| Annual board-approved budget | 30 days before the new fiscal year |

Non-US foreign investors who negotiate board observer rights face an added concern. Observer rights can trigger CFIUS passive-investment review in the US context. This requires careful structuring with legal counsel.

Two exit-related rights protect shareholders during a sale:

- Drag-along rights allow majority holders to compel all shareholders to sell at the same terms. The activation threshold is typically 75% of shares.

- Tag-along rights let minority holders co-sell at the same price when a controlling shareholder sells.

In Cayman Islands structures, both rights are embedded in the Articles of Association. These structures are used by 47.7% of LatAm unicorns. They apply equally to local and foreign shareholders.

How Do You Build a Cross-Border Cap Table Step by Step?

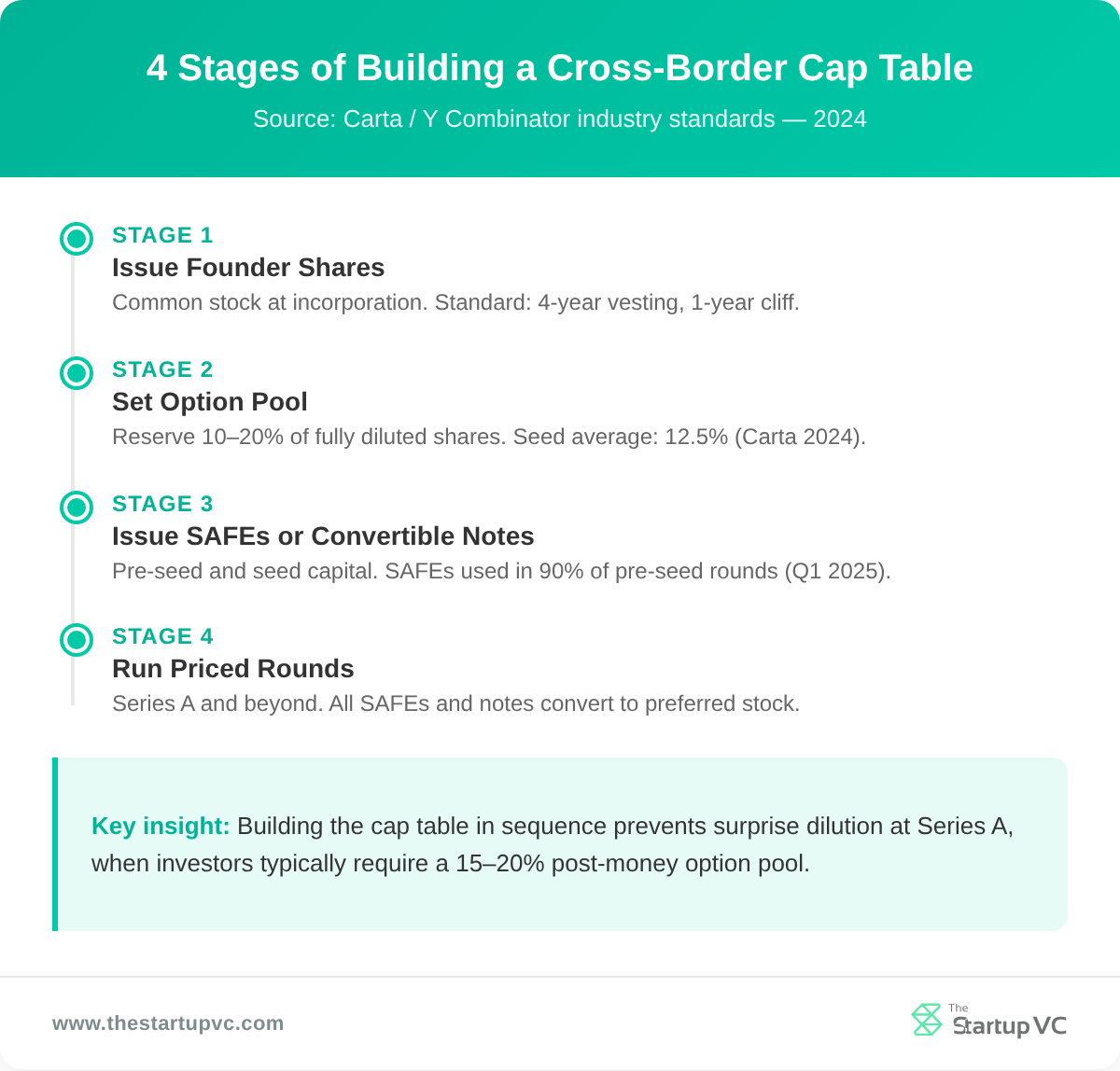

You can build a cross-border cap table by working through four sequential stages. Each stage adds new equity holders and changes your ownership percentages.

- Issue founder shares. Divide equity among co-founders at incorporation. Attach vesting schedules (typically four years with a one-year cliff). Founder shares are common stock.

- Set up the option pool. Reserve 10–20% of fully diluted shares for employees and advisors. Seed-stage pools average 12.5%. Series A pools typically require 15–20% post-financing.

- Issue SAFEs or convertible notes. Use these instruments to raise pre-seed and seed capital. They convert to preferred stock at the next priced round.

- Run priced rounds. Issue preferred stock to institutional investors at Series A and beyond. All outstanding SAFEs and convertible notes convert to preferred stock at this point.

How Do SAFEs and Convertible Notes Affect Your Cap Table?

SAFEs and convertible notes affect your cap table by adding instruments that convert to preferred stock at the next priced round. Each conversion dilutes existing shareholders and adds a new class of preferred holders.

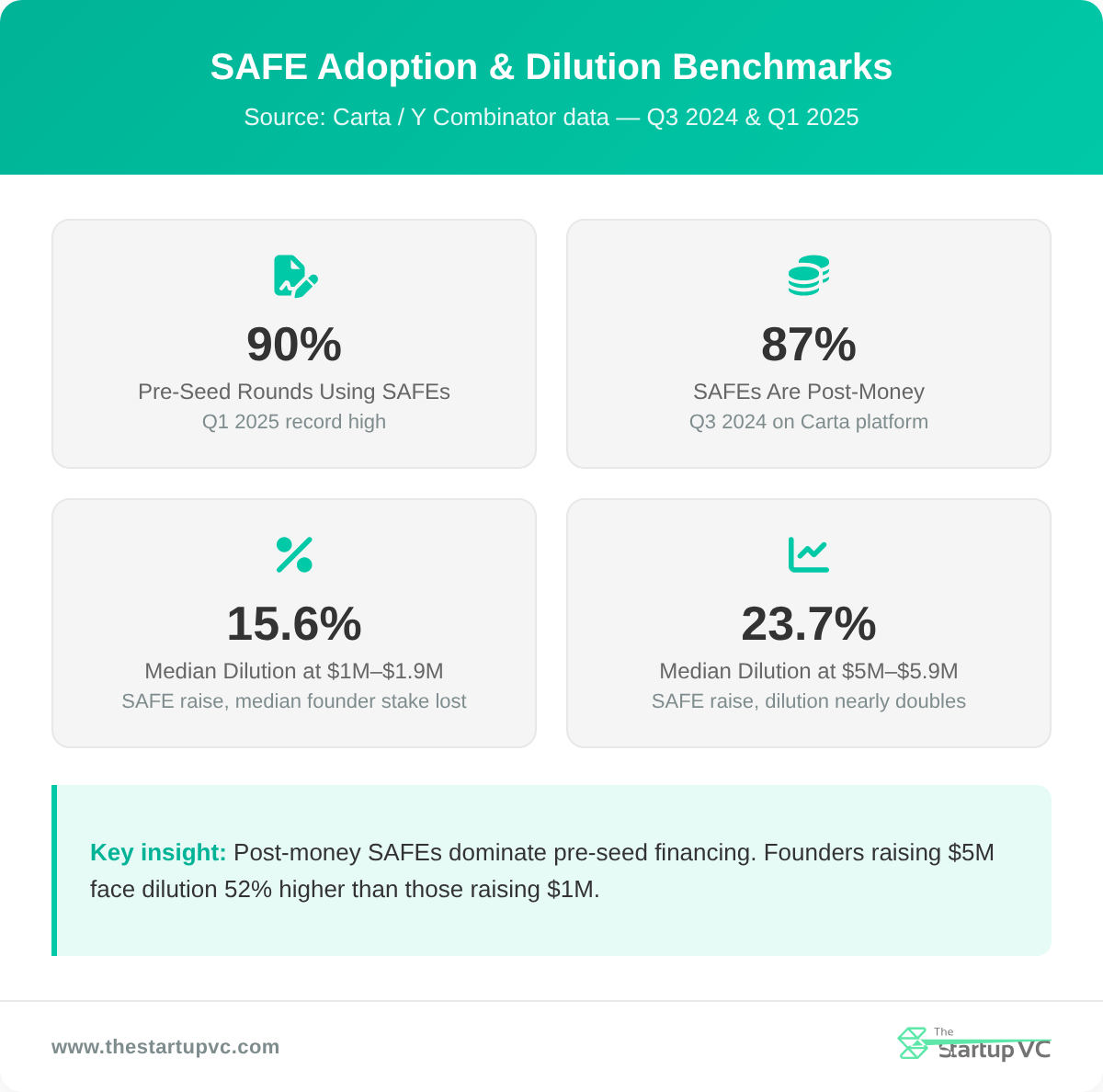

Y Combinator introduced the SAFE in 2013. By Q3 2024, 87% of all SAFEs on Carta were post-money. In Q1 2025, SAFEs were used in 90% of all pre-seed rounds. Post-money SAFEs make dilution predictable because the ownership percentage is fixed at signing.

Convertible notes work similarly but carry interest. Key 2024 terms are shown below.

| Term | Typical Range | 2024 Average |

|---|---|---|

| Interest rate | 4–10% annually | 7.5% (Q3 2024) |

| Discount rate | 15–25% | 20% (most common) |

| Maturity period | 18–30 months | 20–24 months |

Convertible notes differ from SAFEs in one key way. If no qualifying fundraise occurs, unpaid principal plus interest must be repaid at maturity.

For a $1M–$1.9M SAFE raise, median founder dilution is 15.6%. For a $5M–$5.9M raise, dilution rises to 23.7%.

What Tools Do Founders Use to Manage Cross-Border Cap Tables?

Founders use cap table management software to track equity across jurisdictions. The right tool keeps your cap table accurate and investor-ready.

Carta is the dominant platform with over 80% market share. It serves 50,000+ private companies and reported $370M ARR as of early 2024. Carta enterprise pricing ranges from $6,000 to $77,000 per year. Pulley holds roughly 15% market share and starts at $1,200 per year.

Cross-border requirements vary by country. In Colombia, all foreign capital must be registered with the Banco de la República within 30 days. You file Form F4 through an authorized exchange intermediary. Banks enforce Colombia’s SARLAFT 4.0 AML framework and require full UBO disclosure before any investment is formalized.

The Cayman Sandwich structure simplifies cross-border management. It allows SAFEs and convertible notes to be issued at the Cayman holding level. This bypasses direct foreign investment registration at the operating-company level in Colombia and Mexico.

Learn more about business tips for startups in Latin America.

What Tax and Compliance Rules Apply to Cross-Border Investors on Your Cap Table?

The tax and compliance rules for cross-border investors include FATCA, FBAR, country-specific ownership caps, and OFAC screening. Failing to meet these requirements can result in withholding taxes, financial penalties, and blocked investment.

What US Reporting Requirements Apply to Cross-Border Equity?

The main US reporting requirements for cross-border equity are FATCA, FBAR, and IRS Form 5471. Each applies to different parties in the investor-startup relationship.

FATCA (Foreign Account Tax Compliance Act) affects foreign investors in US entities. Foreign financial institutions must register with the IRS. These include foreign VC funds and private equity funds. Those that do not register face a 30% withholding tax on US-source payments. Startups with a US entity must collect a W-8BEN-E form from every foreign investor before closing.

Any US person with foreign accounts exceeding $10,000 must file FBAR annually. This applies even if the balance exceeded $10,000 for just one day. FBAR is filed as FinCEN Form 114.

IRS Form 5471 applies to US persons who are officers, directors, or shareholders in certain foreign corporations. The base penalty for failing to file is $10,000 per form per year. Continuation penalties can reach $50,000. The IRS released a revised Form 5471 in December 2024. US investors holding equity in a LatAm operating company often must file this form.

Under US law, the default withholding tax on dividends paid to foreign shareholders is 30%. This rate can be reduced by a bilateral tax treaty. A US HoldCo structure is preferred for LatAm startups seeking US capital. It allows investors to sell US entity shares at exit, avoiding complex foreign share transfers.

What Foreign Ownership Caps Apply in Latin America?

The main foreign ownership caps in Latin America apply to media, financial, and strategic sectors in Brazil and Colombia. Most other sectors allow 100% foreign ownership under national treatment rules.

| Country | Sector | Cap | Notes |

|---|---|---|---|

| Brazil | Open TV and journalism | 30% foreign voting equity | — |

| Brazil | Financial institutions | No set cap | Central Bank prior approval required |

| Brazil | Nuclear, postal, aerospace | 0% | Fully reserved for government |

| Colombia | National television | 40% of operator | — |

| Colombia | Radio broadcasts | 25% | — |

| Colombia | Most other sectors | 100% | National treatment applies |

You must screen all investors against OFAC’s Specially Designated Nationals (SDN) list before accepting capital. In April 2024, OFAC’s statute of limitations was extended from 5 years to 10 years. OFAC assessed $48.8 million in civil penalties across 12 enforcement actions in 2024. A single unscreened investment from a sanctioned country can expose your startup to legal liability.

Learn more about why Latin American startups are having to change and evolve.

What Questions Do Startup Founders Ask Most Often About Cross-Border Cap Tables?

Can foreign founders own stock in a US company? Yes, any non-US founder can own stock in a Delaware corporation. Citizenship and residency do not affect your right to hold equity. However, US institutional investors typically require a Delaware C-Corp or Cayman holding company as the parent entity before investing.

How common are cap table errors in early-stage startups? Cap table errors affect 23% of early-stage startups, according to Carta’s 2024 data. The most frequent mistakes include incorrect capitalization bases, omitted interim issuances, and pro-rata rights granted too early. A clean cap table is one of the first things institutional investors check.

How should you handle currency differences on a cross-border cap table? You should handle currency by denominating all equity in USD at the holding company level. Local currency mismatches create valuation complexity. They can also trigger currency controls in some LatAm countries. Using a consistent currency at the top-level entity avoids these problems.

What happens to a cap table when a company is acquired? Preferred shareholders are paid first in an acquisition, following the liquidation stack. A 1x non-participating preference on a $50M acquisition means VCs recoup their capital first. Founders and employees split the remaining proceeds.

What happens to preferred shares in an IPO? Preferred shares typically convert to common stock at IPO. This eliminates the liquidation preference. All shareholders then hold the same class of stock.

What ownership thresholds trigger investor rights? The thresholds that trigger investor rights vary by right type. Major investor status, which unlocks pro-rata participation and information rights, typically requires 1% ownership or a $100,000+ check. Board observer rights are often set around 10% ownership. Veto rights typically require 66.66% or more of preferred shareholders to approve key changes.

Ready to Raise Capital From International Investors?

The Startup VC is Craig Dempsey’s family office and company builder in Latin America. The team has structured equity for founders across Colombia, Brazil, and Mexico. Cap table design and cross-border entity structure are among the most critical decisions founders make before raising institutional capital. The wrong structure can block future rounds or cost millions at exit.

Contact us today to discuss your cap table structure and fundraising strategy.