LatAm seed funding fell to a five-year low of $408M in 2024, with pre-seed deals down 77% from the 2022 peak.

Latin America’s seed funding collapsed from a $19.5B VC peak in 2021 to $408M in 2024. Pre-seed deal count fell 77% from its 2022 peak. Local fund managers now support over 80% of early-stage deals by count.

The Startup VC builds and backs ventures across Latin America. Our experience spans multiple funding cycles, from the 2021 boom to the current tighter market. Below, you will find the data behind the decline and practical strategies for raising in this environment.

What Is Happening to Seed Funding in Latin America?

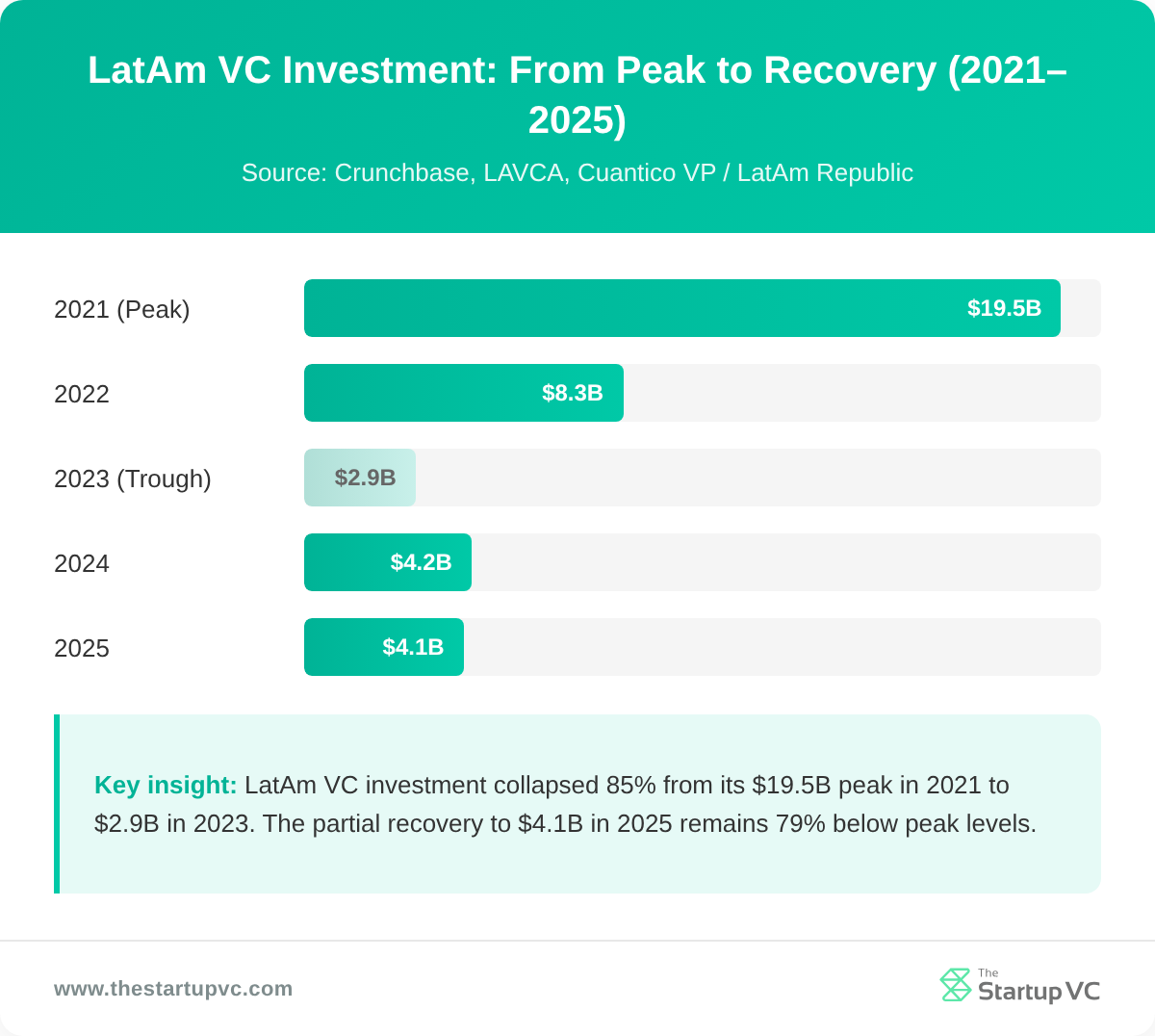

Seed funding in Latin America is at a five-year low. Total venture capital investment across the region fell from a $19.5 billion peak in 2021 to $2.9 billion in 2023. The market has partially recovered, reaching $4.1 billion in 2025. But seed-stage deal volume has not recovered alongside the broader numbers.

The table below shows total LatAm VC investment and seed-stage activity from 2021 to 2025.

| Year | Total LatAm VC | Seed Investment | Seed Deal Count |

|---|---|---|---|

| 2021 | $19.5B | n/a | n/a |

| 2022 | $8.3B | n/a | n/a |

| 2023 | $2.9B | n/a | n/a |

| 2024 | $4.2B | $408M | 321 |

| 2025 | $4.1B | $427M | 247 |

Sources: Crunchbase, LAVCA, Cuantico VP / LatAm Republic

Seed investment fell to $408 million in 2024, the lowest in five years. It edged up slightly to $427 million in 2025, but deal count continued to fall. Average seed check sizes grew from $1.27 million in 2024 to $1.73 million in 2025. Fewer startups received funding, but those that did received larger checks.

What Has Happened to Pre-Seed Funding in Latin America?

Pre-seed funding in Latin America has fallen even more sharply than seed-stage investment. Deal count fell from 251 transactions in 2024 to just 152 in 2025, a 39.4% year-over-year decline. That represents a 77% drop from the 2022 peak. Pre-seed capital fell from $110 million to $66 million, the lowest level since 2018.

In Q3 2025, seed and angel funding across Latin America totaled only $105 million. That figure is 47% below the same quarter in 2024. The contraction at the earliest stages has continued even as larger deal sizes pushed total VC numbers higher.

Why Has Seed Funding in Latin America Dropped So Significantly?

Seed funding in Latin America dropped because global interest rate hikes reduced LP (limited partner) appetite for high-risk, emerging-market investments. When central banks raised rates from near-zero beginning in 2022, investors could earn safe returns from bonds. That shift made locked-up VC positions in developing markets far less attractive.

Latin America-focused VC funds raised only $548 million across 52 funds in 2023–2024. Five interconnected factors drove the seed-specific drop:

- Rising interest rates. LPs cut exposure to high-risk markets as risk-free bond yields rose. LatAm-focused VC fundraising dropped sharply between 2022 and 2024.

- Top investor withdrawal. The five most active 2021 investors went from 149 combined rounds in 2021 to just 11 in H1 2023. That is a 90%+ collapse from the region’s most active investors.

- Mega-round collapse. Deals of $100 million or more fell from 35 in 2021, to 19 in 2022, to just 6 in 2023. These large rounds had pulled up early-stage activity across all funding stages.

- Longer exit timelines. The average time to close a Series C grew from 13 months in 2021 to 24 months in 2023. This stretched the deal pipeline and reduced capital available for new seed bets.

- Preference for serial founders. Serial founders’ share of capital rose from 23% in 2021 to 42% in 2023–2024. This left first-time founders with less access to capital. Most seed-stage startups are led by first-time founders.

Which Investor Types Are Pulling Back the Most From LatAm Seed Deals?

The investor types pulling back the most are large global VCs. SoftBank Latin America Ventures and Tiger Global Management led the retreat from early-stage LatAm deals after 2021.

The table below compares deal activity from the region’s largest investors before and after the 2021 peak.

| Investor | Peak Activity (2021–22) | 2023–24 Activity |

|---|---|---|

| SoftBank LatAm Ventures | ~34 rounds | 2 rounds (Q1 2023) |

| Tiger Global Management | Significant activity | 0 rounds (2023) |

| Kaszek Ventures | 55 rounds | 3 rounds (by mid-2023) |

| FEMSA Ventures (CVC) | Multiple rounds | 2 rounds (2024) |

| IDB Lab (development bank) | Limited | $2M seed fund anchor (2025) |

Sources: Crunchbase, TechCrunch, iadb.org

SoftBank dropped from 34 rounds in 2021–2022 to 2 rounds in Q1 2023 alone. Tiger Global completed zero LatAm deals in all of 2023. Together, these two firms had written roughly 63 checks in the region in 2021.

Kaszek Ventures, the largest VC firm based in Latin America, also pulled back sharply. It made just 3 investments by mid-2023 despite holding $975 million in fresh capital across two new funds. This shows that even committed regional funds chose to wait rather than put capital to work. FEMSA Ventures made only 2 investments in 2024. Broader corporate VC participation fell alongside global VCs.

Which Investors Are Still Supporting LatAm Seed Deals?

The investors still supporting LatAm seed deals include development banks, local specialist funds, and angel networks. IDB Lab committed $2 million to anchor 500 LatAm Seed Fund IV in 2025. That fund targets 40 startups at $300,000 each across Costa Rica, Dominican Republic, Ecuador, Guatemala, Peru, and Uruguay.

Local and regional fund managers now support over 80% of seed deals by count. Magma Partners has backed 125+ companies with over $80 million deployed. Rockstart LatAm made 13 investments in 2024. Angel Ventures in Mexico operates a network of 440+ members focused on pre-seed and seed rounds.

For more on the shifting VC landscape, see where venture capital is going in Latin America.

How Does the Seed Funding Decline Affect Early-Stage Founders in Latin America?

The seed funding decline affects early-stage founders by making fundraising slower, valuations lower, and the traction bar much higher. Founders in 2025 are operating in a market that looks structurally different from 2021.

The four most significant effects on founders are:

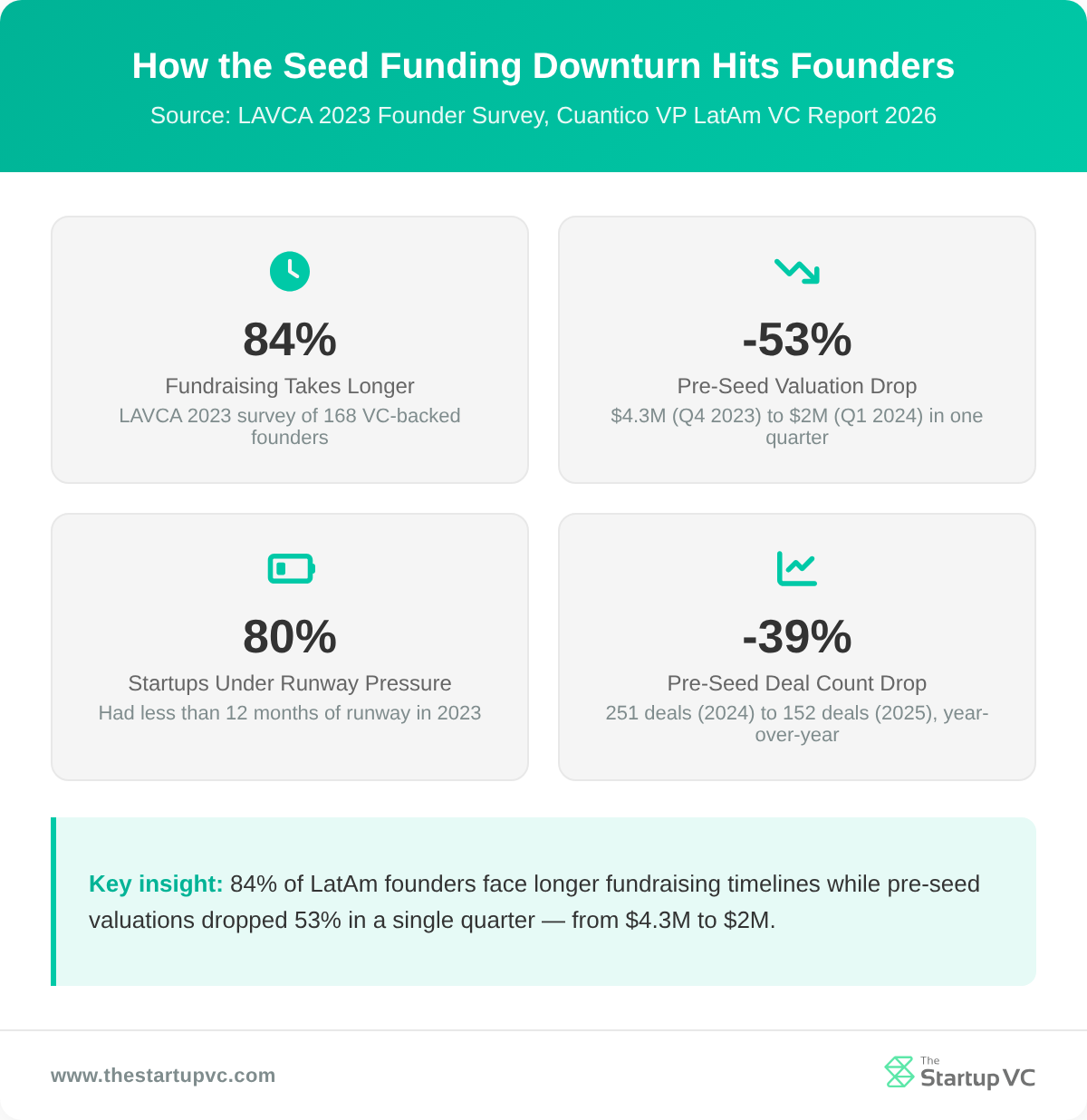

- Longer fundraising timelines. In a 2023 LAVCA survey of 168 VC-backed founders, 84% said fundraising was taking longer than expected. Seed-stage companies faced the most difficulty.

- Lower valuations. The median pre-seed valuation in Latin America dropped from $4.3 million in Q4 2023 to $2 million in Q1 2024. That is a 53% decline in a single quarter.

- Tighter runway. Four out of five early-stage LatAm companies had less than 12 months of runway in 2023. Many chose to cut costs rather than pursue growth.

- Layoffs. As capital tightened, startups reduced headcount to survive. Betterfly cut 30% of its workforce. Unico laid off 10.5%, or around 110 employees. Merama cut around 10% of staff. Bayz reduced headcount by 50%.

What Does the Revenue-First Shift Mean for LatAm Founders?

The revenue-first shift means that investors now expect measurable revenue before writing a seed check. Chile’s Buk bootstrapped for five years before taking institutional capital. It reached $87.3 million in ARR before closing a $50 million Series B. That model is now the standard investors hold up across Latin America.

Cuantico VP CEO José Kont stated there is “a lack of clear traction signals at early stages” in LatAm. The market has shifted from rewarding growth stories to rewarding capital efficiency and unit economics. First-time founders building without revenue face a harder path to their first institutional round. Chile’s startup environment has been a leading example of this model. For more context, see our overview of startups in Chile.

What Can Early-Stage Founders Do to Raise Seed Funding in a Tighter Market?

You can raise seed funding in a tighter market by building revenue first. Target local and regional investors and use non-dilutive capital programs alongside VC.

What Revenue Milestones Should You Hit Before Raising Seed?

You should aim for measurable revenue traction before approaching VC firms. Leadsales, a Mexican B2B startup, bootstrapped to $1.6 million in ARR and 1,400 paying customers before raising. It then closed a $3.7 million seed round led by Ulu Ventures and Blue Pointe Ventures in 2023. That level of traction is now the baseline most LatAm VCs expect.

Investors now focus on capital efficiency, unit economics, and AI integration. Y Combinator’s Winter 2024 batch included only one LatAm startup. That is down from 33 in Winter 2022. AI-focused positioning now helps LatAm founders compete for global top-tier accelerator spots.

Which Accelerators and Regional Funds Are Still Writing Checks?

The accelerators and regional funds still writing seed checks are 500 Global LatAm, Platanus Ventures, Magma Partners, and Rockstart LatAm.

| Fund | Check Size | Terms |

|---|---|---|

| 500 Global LatAm | $300,000 | 10% equity |

| Platanus Ventures | $200,000 | 5.5% post-money SAFE |

| Magma Partners | Up to $600K+ | Equity (varies) |

| Rockstart LatAm | Varies | Equity |

| Angel Ventures | Up to $500K | Varies |

Regional specialist funds continue to write checks even as global VCs have pulled back. Magma Partners has backed over 125 startups with more than $80 million deployed. Rockstart LatAm made 13 investments in 2024. These funds fill the gap left by large global VCs.

What Non-Dilutive Funding Options Exist for LatAm Founders?

The non-dilutive funding options for LatAm founders include government grant programs and revenue-based financing. These vary by country and company stage.

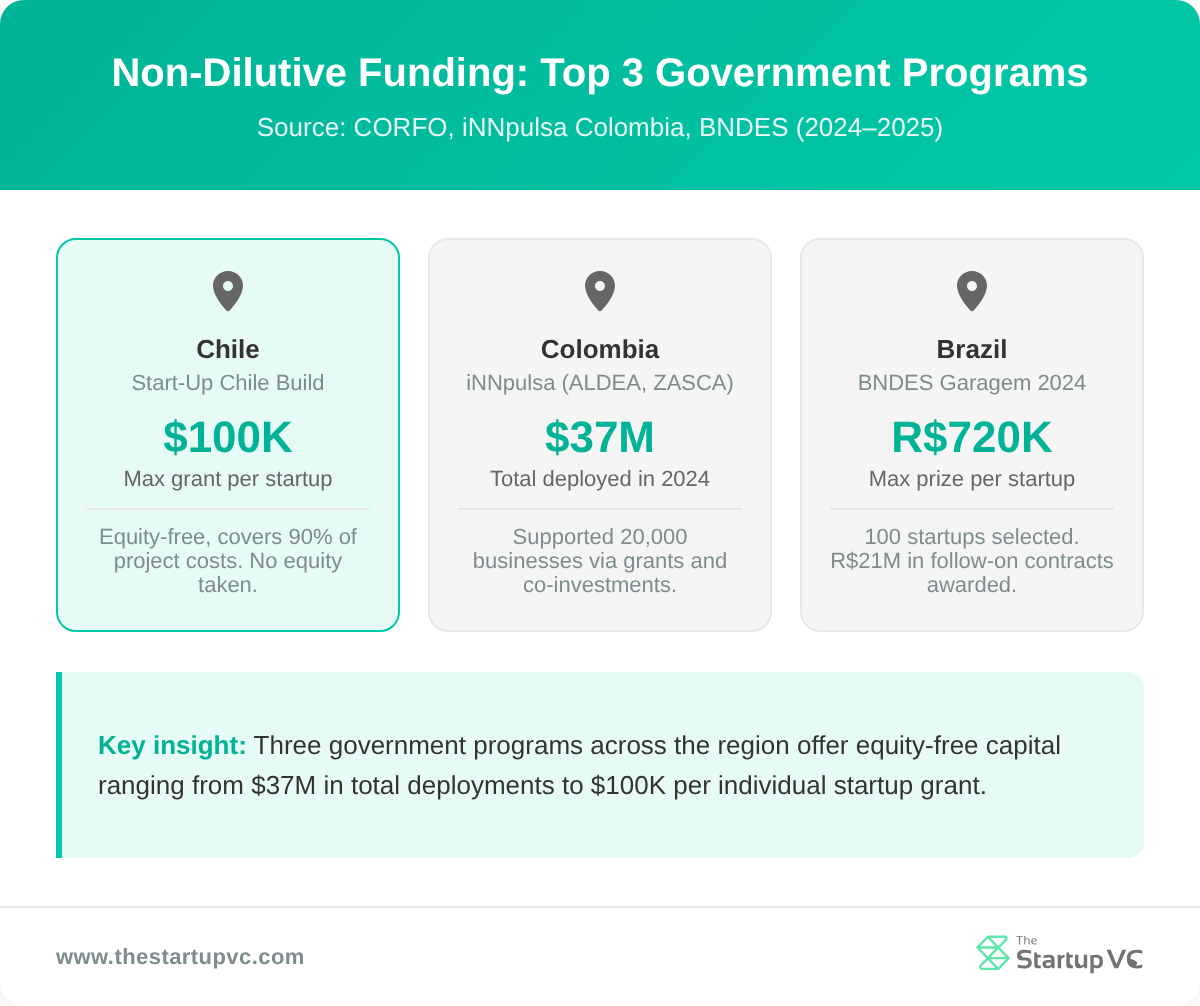

Government programs in the region include:

- Start-Up Chile Build (CORFO). Equity-free grants up to approximately $100,000, covering 90% of project costs.

- iNNpulsa Colombia (ALDEA, ZASCA). Deployed COP $150 billion (about $37M USD) to 20,000 businesses in 2024.

- BNDES Garagem (Brazil). Selected 100 startups from 1,840 applicants. Prizes reach up to R$720,000. Follow-on contracts totaled R$21 million.

Revenue-based financing is a growing option for B2B SaaS startups in the region. Providers like Efficient Capital Labs offer up to 65% of projected ARR at a flat fee of 10–12%. Funding arrives in as little as 72 hours. For more on building in the region, see our business tips for startups in Latin America.

What Questions Do LatAm Founders Ask Most Often About the Seed Funding Decline?

These are the questions early-stage founders ask most often about the current funding environment across Latin America.

Is the LatAm funding market recovering?

The LatAm funding market is partially recovering. Total VC investment reached $4.126 billion in 2025, up 13.8% year-over-year. However, deal count fell to its lowest level since 2017. Larger average check sizes are driving the rebound, while the number of funded startups remains at historic lows.

What do investors look for in early-stage LatAm startups now?

Investors look for capital efficiency, clear unit economics, and AI integration. Governance maturity is also a key factor. Growth narratives without revenue data no longer secure seed deals.

What is the typical seed check size in Latin America?

The typical seed check in Latin America rose from $1.27 million in 2024 to $1.73 million in 2025. Pre-seed investment fell to $66 million total in 2025. That is the lowest pre-seed capital pool since 2018.

How long does it take to raise a seed round in Latin America?

A seed round in Latin America takes 6 to 9 months in the current environment. Global averages run about 115 days. LatAm rounds stretch longer due to heavier due diligence and legal structuring. Setting up a Delaware C-Corp for US investors adds extra weeks to the process.

What funding alternatives to VC exist for early-stage LatAm founders?

The main alternatives to VC include government grants, accelerators, and revenue-based financing. Start-Up Chile offers up to $100,000 with no equity taken. iNNpulsa Colombia deployed about $37 million to 20,000 businesses in 2024. BNDES in Brazil awarded prizes up to R$720,000 through the Garagem program. Efficient Capital Labs funds up to 65% of ARR within 72 hours.

Is angel investment still active in Latin America?

Yes, angel investment is still active across Latin America. Angel Ventures in Mexico has more than 440 members and invests at pre-seed and seed stages. The Guadalajara Angel Investors Network (GAIN) covers fintech, proptech, and SaaS. These networks focus on rounds below $500,000.

Ready to Build Your Startup in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder. It creates, backs, and scales ventures across Latin America. Our portfolio includes Biz Latin Hub, operating in 17 Latin American countries. We provide capital, hands-on operational support, and access to regional networks built through years of on-the-ground experience.

Whether you are navigating a difficult fundraise or building revenue before raising, we can help. Contact us today to learn how The Startup VC supports early-stage founders across Latin America.