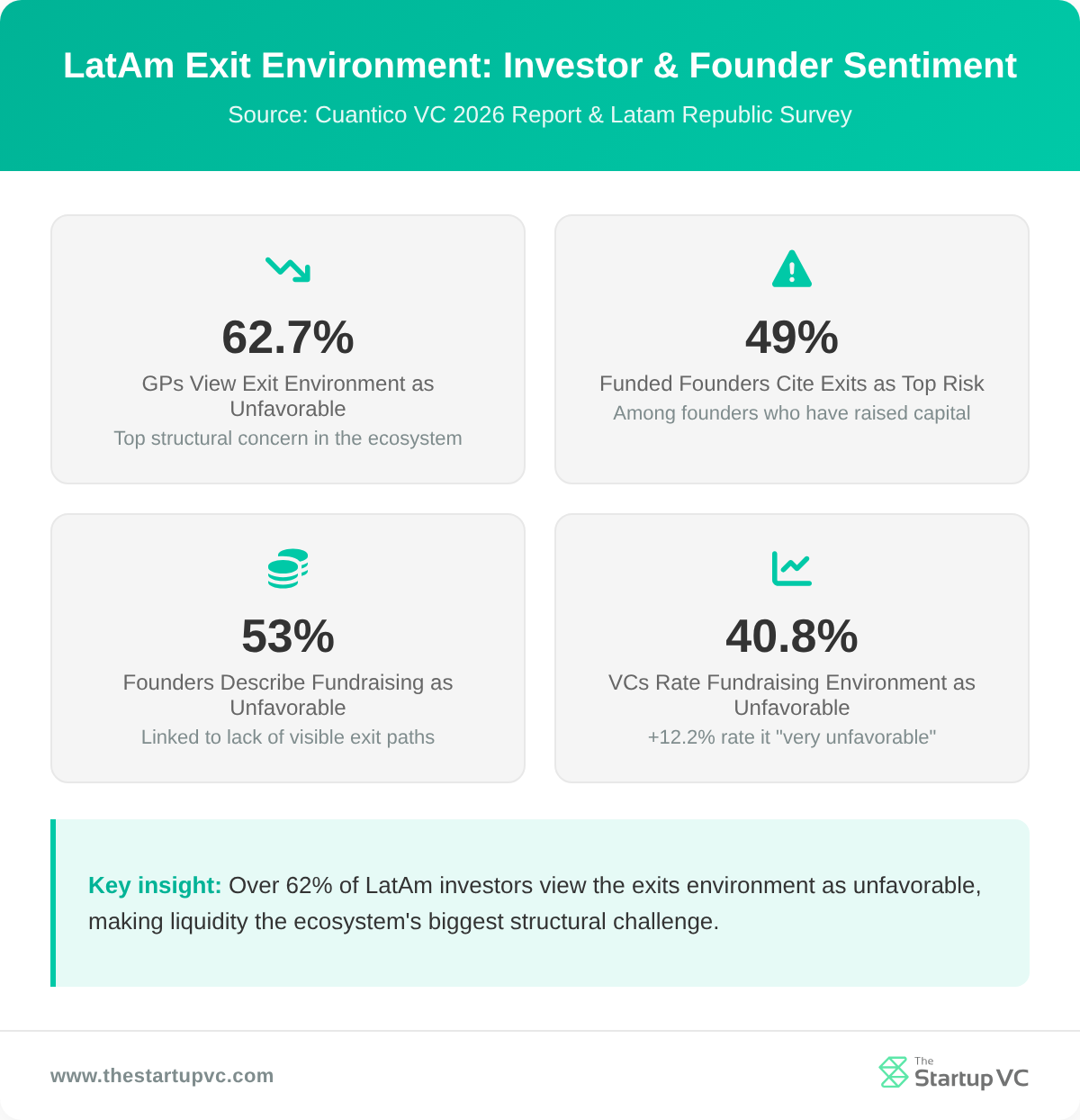

62.7% of LatAm VCs call the exit environment unfavorable, with only 79 startups exiting in 2024, the region’s lowest total in years.

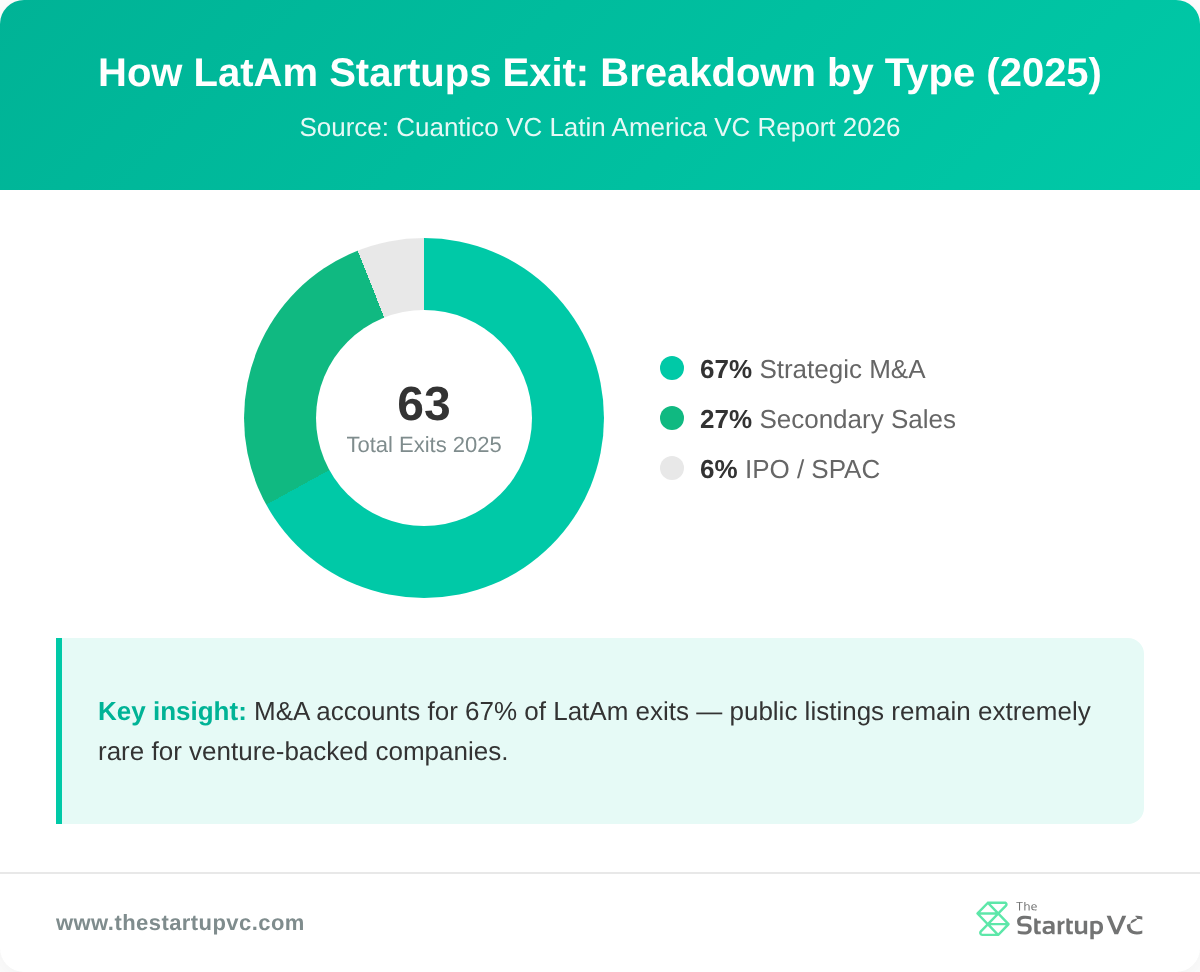

In 2024, Latin America recorded only 79 VC-backed exits worth US$1.8 billion, down from US$8.8 billion in 2021. M&A accounts for 67% of exits. Just 8 funds operate at Series C, limiting the scale startups need to attract buyers.

The Startup VC tracks the LatAm venture landscape from the inside. We have built and exited portfolio companies, including Biz Latin Hub, acquired by Vistra in December 2025. This article covers why exits are scarce, how the shortage affects LP capital, and what founders need to know about realistic exit paths today.

What Is the LatAm Exits Problem?

The LatAm exits problem is the shortage of liquidity events for venture-backed startups in Latin America. An exit happens when a startup’s investors and founders can convert their equity into cash. This can happen through an acquisition, a public listing, or a secondary sale.

Without exits, the venture capital cycle breaks down. Investors cannot return money to LPs. LPs cannot reinvest in new funds. New funds cannot back the next generation of founders.

In 2024, only 79 VC-backed companies exited across all of Latin America. That is the lowest total in recent years. Exit values hit a low of US$1.8 billion in 2024. Even the 2025 recovery, which brought US$4.9 billion across 63 transactions, remains far below the 2021 peak of US$8.8 billion.

The data makes the problem clear. A Cuantico VP survey found that 62.7% of General Partners consider the exit environment unfavorable. Among founders who have received funding, 49% name the lack of exits as their top ecosystem risk.

| Metric | 2021 (Peak) | 2024 (Low) | 2025 (Recovery) |

|---|---|---|---|

| Exit value (US$B) | 8.8 | 1.8 | 4.9 |

| Number of exits | High | 79 | 63 |

| Avg deal size (US$M) | High | 29 | 77.8 |

The problem is structural, not cyclical. The region has not built the market infrastructure needed to support regular, large exits. That gap affects every participant in the ecosystem.

Why Are Exits So Rare in Latin America?

Exits are rare in Latin America because of three overlapping structural problems: underdeveloped public markets, a shortage of growth-stage capital, and valuation overhang from the 2021 funding peak.

Why Do Public Markets Fail LatAm Startups?

Public markets fail LatAm startups because local exchanges in Brazil, Mexico, and Colombia lack depth and liquidity. No Brazilian company completed an IPO from 2021 until PicPay listed on Nasdaq in early 2026. Even that deal priced much lower than founders expected.

Listing in the US is equally difficult. US investors apply valuation discounts to LatAm companies because of FX risk, governance concerns, and political instability. Founders who spent years building IPO-ready companies have found the window stayed closed.

Why Is Growth-Stage Capital So Scarce?

Growth-stage capital is scarce because the LatAm fund landscape is concentrated at the early stage. 74.4% of all VC funds in Latin America operate at early stages. Only 8 funds are active at Series C. Without Series C investors, most startups cannot reach the scale needed for a serious exit.

This creates a funnel problem. Many companies get funded at seed. Far fewer reach Series A. Very few ever attract growth capital needed for an exit that returns meaningful value.

How Does Valuation Overhang Block Deals?

Valuation overhang blocks deals by creating a price gap between what sellers expect and what buyers will pay. Many startups raised money at inflated 2021 valuations. They took capital at prices that assumed continued high growth in a favorable market. That market did not last.

Now these companies cannot exit at their last round price. Buyers will not pay 2021 multiples for 2025 performance. Founders and investors would rather hold than accept a down-round exit. The result is a market full of companies that are too expensive to sell and not big enough to list.

How Does the Exits Shortage Affect Investors and LP Capital?

The exits shortage affects investors and LP capital by breaking the feedback loop that keeps venture capital healthy. When exits do not happen, LPs do not receive returns. When LPs do not receive returns, they stop committing to new funds. When new funds cannot form, founders lose access to capital.

What Happens to LP Returns When Exits Stall?

LP returns stall because the deals that would deliver them never close. Brazilian VC funds post a MOIC of 2.60x when exits do occur, compared to 2.11x for US funds. But a high return rate means nothing if exits never happen.

Most LPs in LatAm funds have been waiting years for liquidity. Many funds launched between 2018 and 2021 are now approaching or past their expected return windows without meaningful distributions. This damages trust. LPs who have not received returns are cautious about committing to new funds.

How Does the Exit Drought Shrink the Capital Pool?

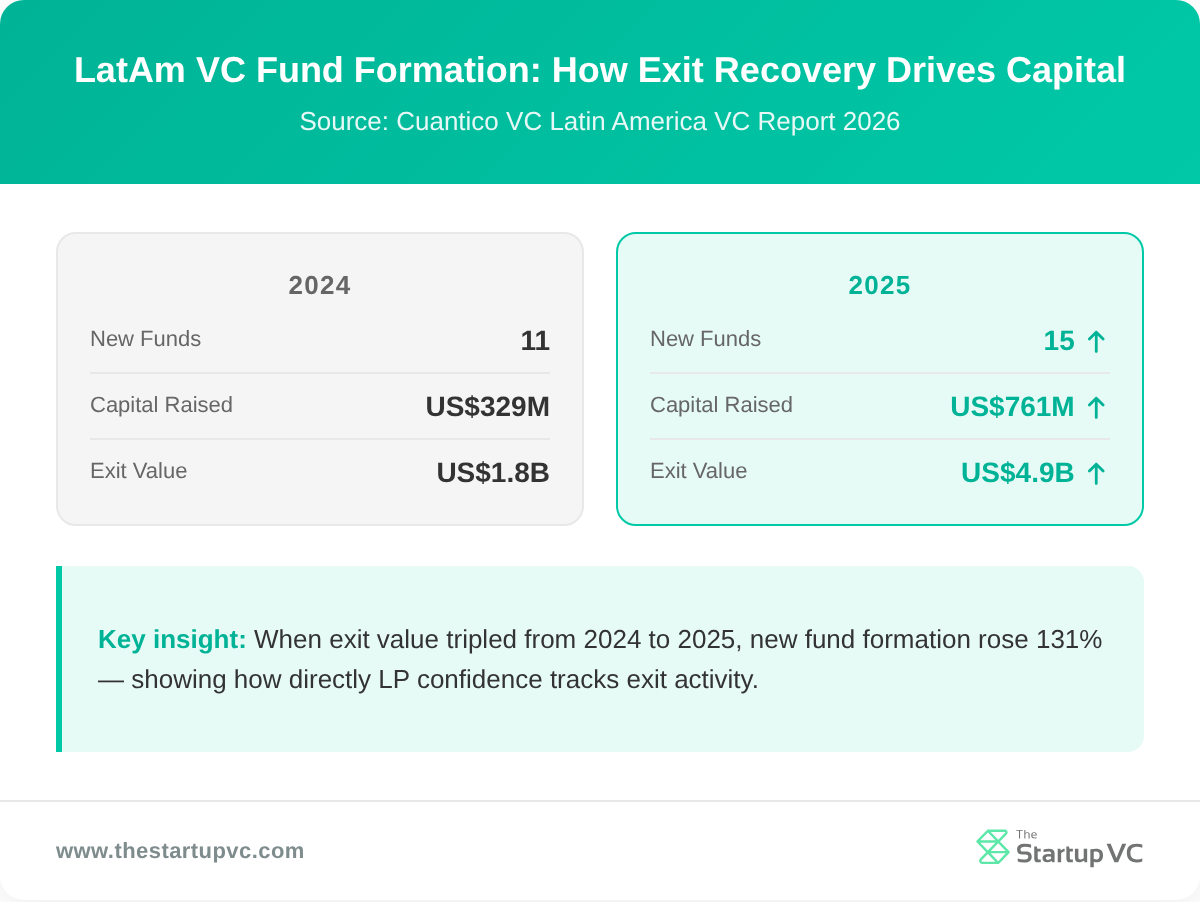

The exit drought shrinks the capital pool by cutting off the source of new fund formation. In 2024, venture capital fund formation in Latin America collapsed. Only 11 new funds launched, raising a combined US$329 million. That is a fraction of what the region needs to sustain a healthy startup ecosystem.

The 2025 recovery helped. Fifteen new funds launched, raising US$761 million, a 131% increase over 2024. But this recovery is directly tied to the improvement in exit activity. The Cuantico VC 2026 report projects LP confidence recovering in 2026 to 2027, citing the 2025 exit surge as the reason.

The linkage is direct. Exit value goes up. LP confidence goes up. New fund formation goes up. Founders get funded. The reverse is equally true.

Learn more about where venture capital is going in Latin America at The Startup VC.

| Year | New Funds | Capital Raised | Exit Value |

|---|---|---|---|

| 2024 | 11 | US$329M | US$1.8B |

| 2025 | 15 | US$761M | US$4.9B |

What Exit Paths Are Available to LatAm Founders Today?

The exit paths available to LatAm founders today are strategic acquisitions, secondary sales, and public listings. These paths differ significantly in frequency, timeline, and likely outcome.

How Do Strategic Acquisitions Work for LatAm Startups?

Strategic acquisitions work by connecting LatAm startups with buyers who want their product, team, or market position. They account for 67% of all VC-backed exits in Latin America and are the most realistic path for most founders.

Two types of buyers are active. The first is global strategic players. Companies like BBVA, Nubank, and Mercado Libre have each made acquisitions to expand their regional product and distribution. BBVA acquired Openpay. Nubank acquired Plata and Spin Pay. Mercado Libre acquired Kangu for last-mile logistics.

The second type is startup-to-startup acquisitions. Unicorns now buy smaller startups for compliance tools, logistics networks, vertical SaaS platforms, and data infrastructure. This category barely existed in LatAm before 2020. It now represents a legitimate exit path.

Recent deal examples include Gringo, a Brazilian vehicle app, acquired by Cambridge Global Payments for about US$172 million. Biz Latin Hub was acquired by Vistra in December 2025, extending Vistra’s coverage to 50+ global markets.

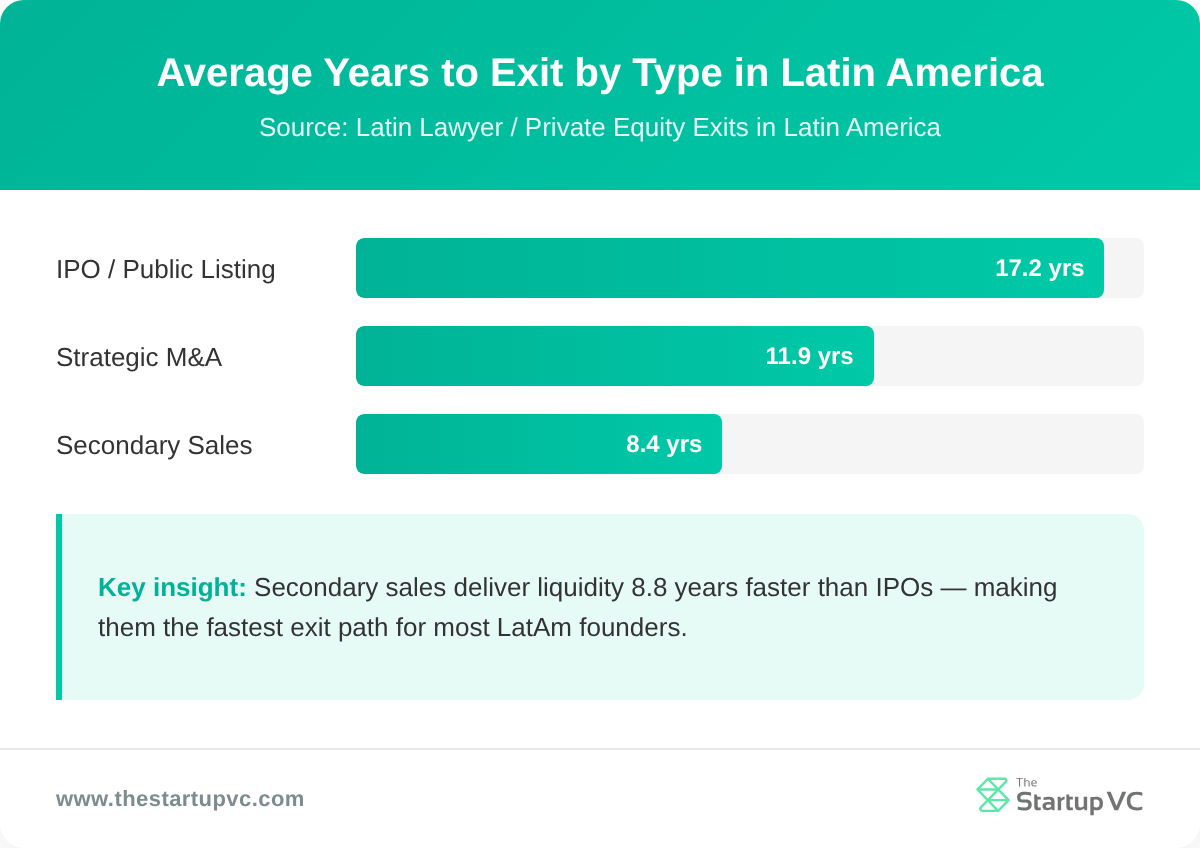

M&A deals occur after an average of 11.9 years in Latin America. That is a long time, but it is still shorter than the alternatives.

What Are Secondary Sales and How Common Are They?

Secondary sales represent 27% of LatAm exits. In a secondary, an investor sells their shares to another private buyer rather than through a public market or acquisition. The company does not need to be acquired or listed.

Secondaries provide partial liquidity. Founders or early investors can sell a portion of their stake without a full exit event. Companies like Vercel, Plata, Contabilizei, and Omie have used secondary transactions in recent years.

Secondary sales occur after an average of 8.4 years, faster than M&A at 11.9 years. For founders looking for earlier liquidity, secondaries are a practical tool.

Is an IPO Still a Realistic Option?

An IPO is rarely realistic for most LatAm founders today. Brazilian IPOs average 17.2 years from founding to listing. Local exchanges lack the depth to support large tech IPOs. US listings carry valuation discounts.

The one recent example, PicPay on Nasdaq in early 2026, is the first Brazilian company to list in nearly four years. It priced lower than expected. This is not an encouraging benchmark.

For founders at early or growth stages, building toward an IPO is a low-probability strategy. M&A or secondaries offer more reliable timelines.

| Exit Type | Share of LatAm Exits | Avg Timeline |

|---|---|---|

| Strategic M&A | 67% | 11.9 years |

| Secondary sales | 27% | 8.4 years |

| IPO/SPAC | ~6% | 17.2 years (Brazil) |

How Does the Exits Problem Shape What Founders Can Realistically Build?

The exits problem shapes what founders can build by changing what investors will fund, how much money is available, and which business models attract capital. Founders who ignore this build for an environment that no longer exists.

How Has the Fundraising Bar Changed for LatAm Founders?

The fundraising bar has risen by requiring founders to show a credible exit path, not just a growth story. More than 53% of founders describe the LatAm fundraising environment as unfavorable or very unfavorable. Investors now require measurable traction before committing capital.

This is a shift from 2019 to 2021, when early-stage narrative was enough. Today, investors ask directly: who will buy this company, and at what price?

Pre-seed funding shows the impact most clearly. Pre-seed capital fell 40% from US$110 million to US$66 million in 2025. Deal volume fell 39.4% from 251 rounds to 152. The companies that do not get funded are those without a visible exit story.

What Types of Companies Attract Capital in This Environment?

The types of companies that attract capital are those that solve clear, high-value problems for identifiable strategic buyers. The practical test is whether a buyer would pay US$50 million or more for the product or team.

This favors B2B companies over consumer apps. It favors vertical SaaS with deep integrations over general-purpose platforms. It favors companies with revenue and retention over those with user counts.

Corporate venture capital has also grown as a funding source. Companies in fintech, energy, retail, logistics, and healthcare have become more active early-stage investors. That capital comes with an expectation that the startup will be acquired by or aligned with the corporate’s strategy.

Founders who take corporate VC need to understand this dynamic. The exit path is often built into the investment thesis from day one.

See how Latin American startups are having to change and evolve in response to this environment.

The “more money for fewer startups” dynamic of 2025 reflects all of this. Total VC investment rose 13.8% to US$4.1 billion. But deal volume fell. Larger checks went to fewer companies. The companies that won those checks had clear exit strategies, not just growth stories.

What Questions Do Founders Ask Most Often About Exits in Latin America?

How long does it take to exit a startup in Latin America? Exit timelines vary by type. Strategic acquisitions average 11.9 years from founding. Secondary sales average 8.4 years. Brazilian IPOs average 17.2 years. Most founders will reach a liquidity event through M&A, not a public listing.

What is the most common exit path for LatAm startups? Strategic acquisitions are the most common exit path, accounting for 67% of VC-backed exits in the region. Secondary sales account for 27%. Public listings are rare and require significant scale.

How does the exit environment affect how much funding I can raise? It affects funding directly. Investors need to see a plausible exit before they commit capital. When exits are scarce, LPs stop funding new VC vehicles. More than 53% of LatAm founders describe the fundraising environment as unfavorable today.

Should I target a US listing or a local stock exchange? Neither path is realistic for most LatAm founders. No Brazilian company completed an IPO from 2021 to early 2026. US listings apply valuation discounts for FX and governance risks. Build toward acquisition or secondary liquidity first.

Who are the most active acquirers of LatAm startups? Active acquirers include regional unicorns like Nubank and Mercado Libre, global banks like BBVA, and cross-border buyers like Vistra and Cambridge Global Payments. Corporate venture capital arms are also growing as investors and eventual buyers.

Can I build a large company in LatAm given the exits problem? Yes, but the strategy must align with the environment. Build deep value for identifiable acquirers. Prioritize B2B, vertical SaaS, or service businesses with strong retention. Avoid scale-at-all-costs models that depend on public market exits.

Ready to Build a Fundable Company in Latin America?

The exits landscape in Latin America is difficult. But founders who understand it can navigate it.

The Startup VC is Craig Dempsey’s family office and company builder. We create, back, and scale ventures across Latin America with hands-on operational support, not just capital. Our portfolio includes Biz Latin Hub, which built real value and completed a successful exit to Vistra in December 2025.

If you are building in LatAm and want practical guidance on exit strategy, fundraising, and company building, we can help. Contact us today to start the conversation.