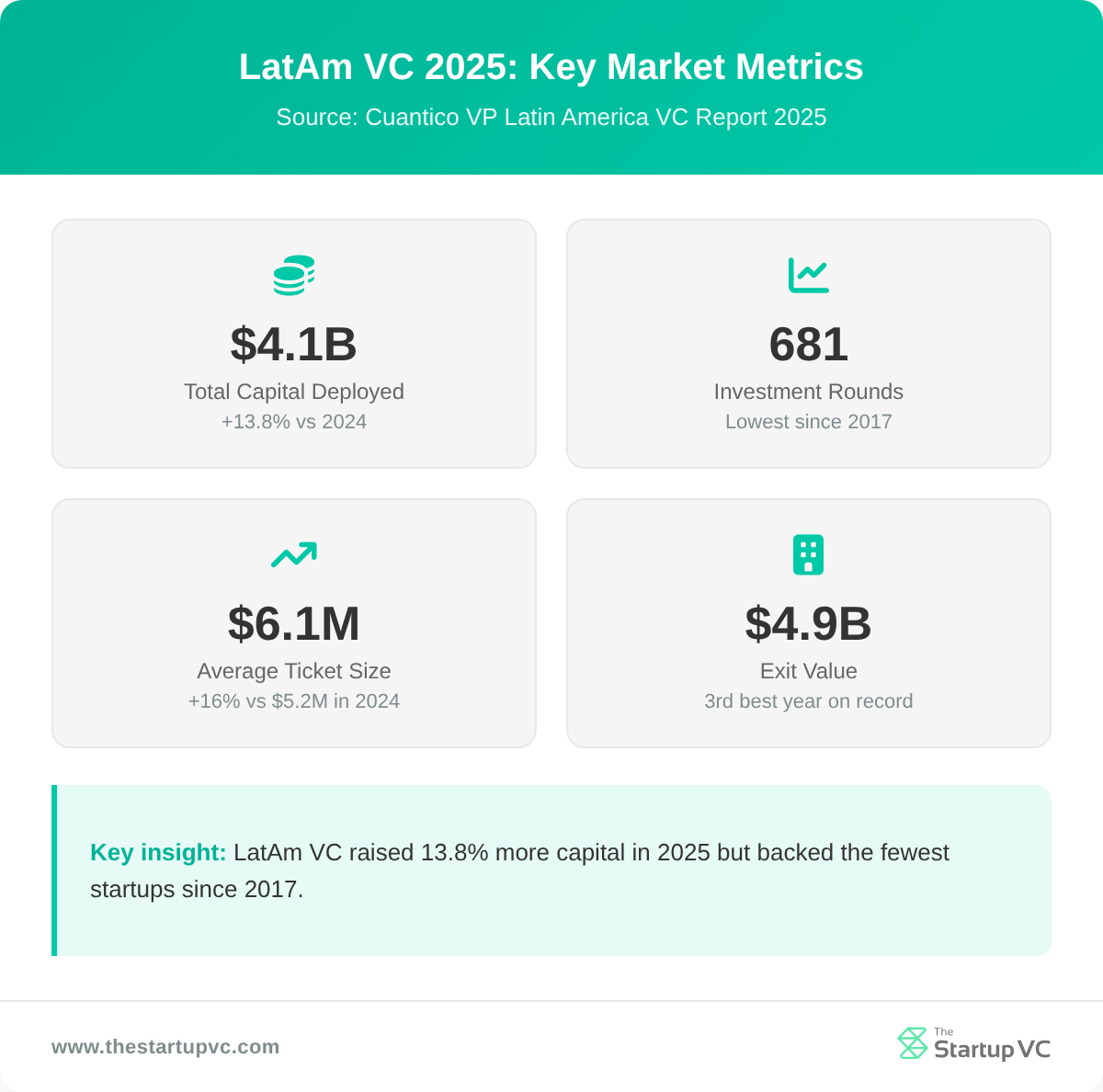

LatAm VC raised US$4.1B across 681 rounds in 2025, 13.8% more capital but the fewest deals since 2017.

Latin America’s venture capital reached US$4.126 billion across 681 rounds in 2025, a 13.8% increase but the fewest deals since 2017. Average round size rose 16% to US$6.1 million. Investors deployed more capital to fewer startups.

The Cuantico VP report confirms what many LatAm investors already felt: this rebound is not a return to 2021. It is a flight to quality. The Startup VC has tracked these shifts through Biz Latin Hub’s presence across 17 countries. Below, you will find what the 2025 data means for founders and what it takes to raise in 2026.

What Happened to Venture Capital in Latin America in 2025?

Venture capital in Latin America raised US$4.126 billion across 681 rounds in 2025. That total is 13.8% higher than the US$3.627 billion raised in 2024. But the headline number hides a more complex story: more money went to fewer startups.

Why Did Capital Rise While Deal Count Fell?

The average ticket size rose 16%, from US$5.2 million to US$6.1 million. Investors deployed larger checks but backed fewer companies. Deal count fell 1.9%, from 694 to 681 rounds. That 681 figure is the lowest since 2017.

The top 10 deals alone accounted for US$1.229 billion, or about 30% of all capital. That concentration tells you where the money went: a handful of large, later-stage rounds dominated the year.

Did Exits Improve in 2025?

Exit activity improved sharply in 2025. Exit value surged to US$4.9 billion across 63 transactions, up from US$1.8 billion in 2024. The average exit size rose from US$29 million to US$77.8 million.

That makes 2025 the third-best year on record for LatAm exits. Only 2021 (US$8.8 billion) and 2018 (US$7.2 billion) rank higher. Two new unicorns were created, matching 2024, but far below the 22 created in 2021.

Why Did Deal Count in LatAm VC Fall to Its Lowest Level Since 2017?

Deal count fell because the market shifted from volume to quality. Investors stopped funding speculative early-stage bets. They concentrated capital in startups with proven models and measurable traction.

What Happened to Pre-Seed Funding?

Pre-seed funding fell sharply in 2025. Capital at this stage dropped 40%, from US$110 million to US$66 million. Deal count at pre-seed fell 39.4%, to just 152 rounds, the lowest since 2018.

This represents a 77% decline from the 2022 pre-seed peak of 661 deals. For a deeper look at the data behind early-stage contraction, see LatAm seed funding is declining. José Kont, CEO of Cuantico VP, summarized the problem: “Deal flow in Latin America is far from where the industry needs it to be. Ecosystems are not generating enough startups.”

Of the 351 active VC funds in LatAm, 74.4% operate at early stages (pre-seed and seed). That means many funds are competing for a shrinking pool of investable deals.

Where Did Capital Concentrate Instead?

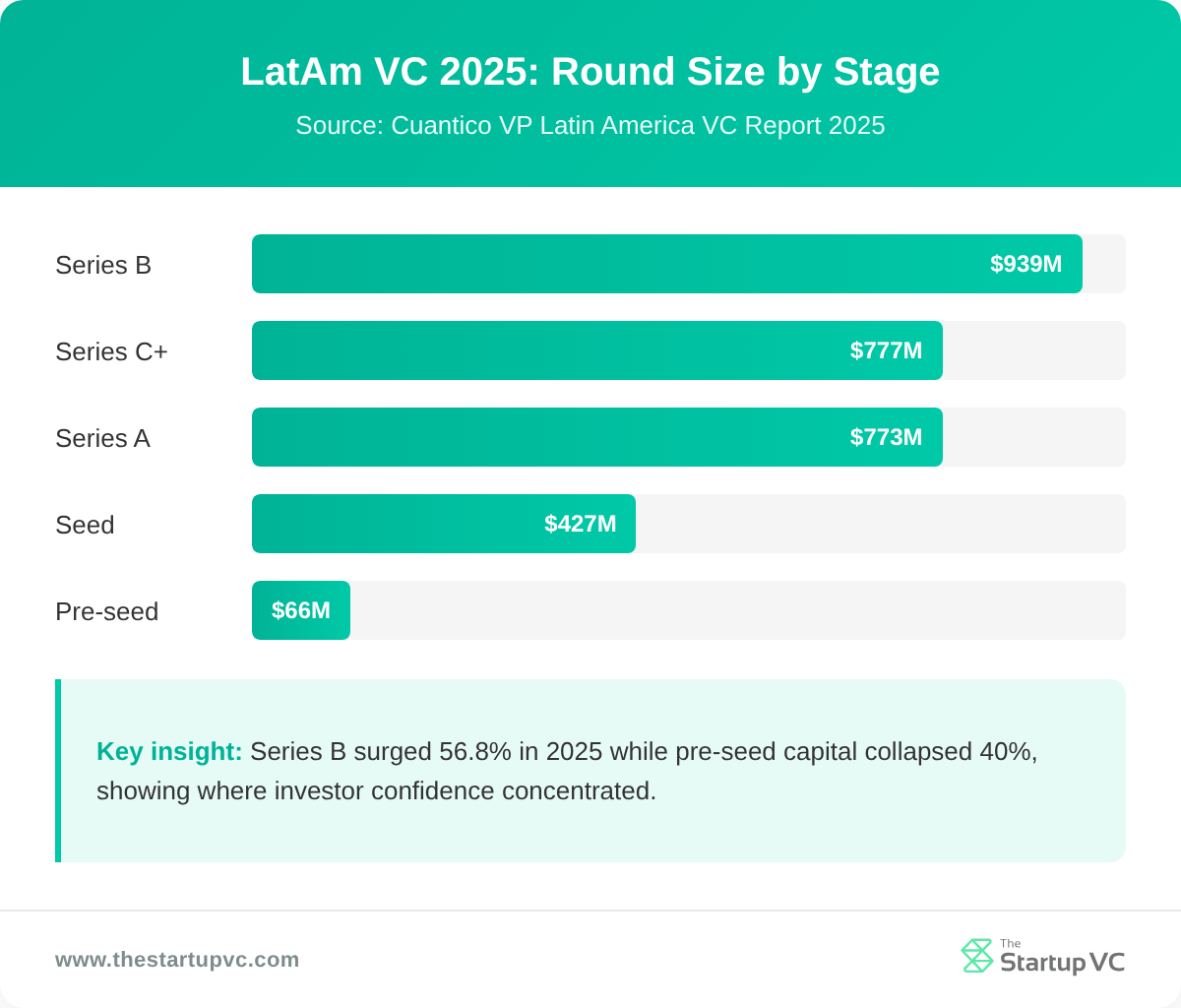

Capital moved toward mid-stage rounds. Series B funding surged 56.8%, rising to US$939 million across 24 deals. Series A grew 9.3% to US$773 million across 72 deals. Seed funding grew modestly, up 4.7% to US$427 million.

Series C+ contracted sharply, falling 56.8% to US$777 million. This suggests the largest late-stage checks were selective too, reserved for companies with strong exit paths.

What Is “Flight to Quality” and How Does It Shape LatAm VC in 2025?

Flight to quality is the shift in investor behavior toward fewer, stronger companies. Investors are writing fewer checks. When they do write one, they require better governance, clearer unit economics, and a faster path to profitability.

How Are Founders Experiencing This Shift?

Founder sentiment reflects the difficulty. More than 53% of founders describe the fundraising environment as unfavorable or very unfavorable in 2025. Around 30.6% of founders were still in the process of closing their round. Among those who completed a round, 24.5% took between six and twelve months to secure capital.

That fundraising timeline is a direct result of investor selectivity. Investors run longer due diligence processes. They demand more governance and reporting than they did in 2021.

What Do Investors Now Prefer in LatAm?

Investors favor proven founders. Repeat and serial entrepreneurs accounted for 42% of total capital deployed in 2023 and 2024. That compares to just 23% in 2021.

In 2025, the criteria investors apply most consistently are:

- Founder track record. Serial entrepreneurs have a significant advantage over first-time founders.

- Revenue traction. Repeatable sales matter more than growth projections.

- Unit economics. Strong margins and controlled customer acquisition costs are non-negotiable.

- Governance. Clean cap tables, formal reporting, and clear equity structures reduce diligence friction.

Fund activity tells a different story from deal selectivity. Fifteen new VC funds launched in 2025, raising US$761 million. That is a 131% increase from 11 funds raising US$329 million in 2024. Fund managers are bullish on LatAm’s long-term potential. But they are selective about which startups get the capital.

Which Countries and Sectors Attracted the Most VC Capital in LatAm in 2025?

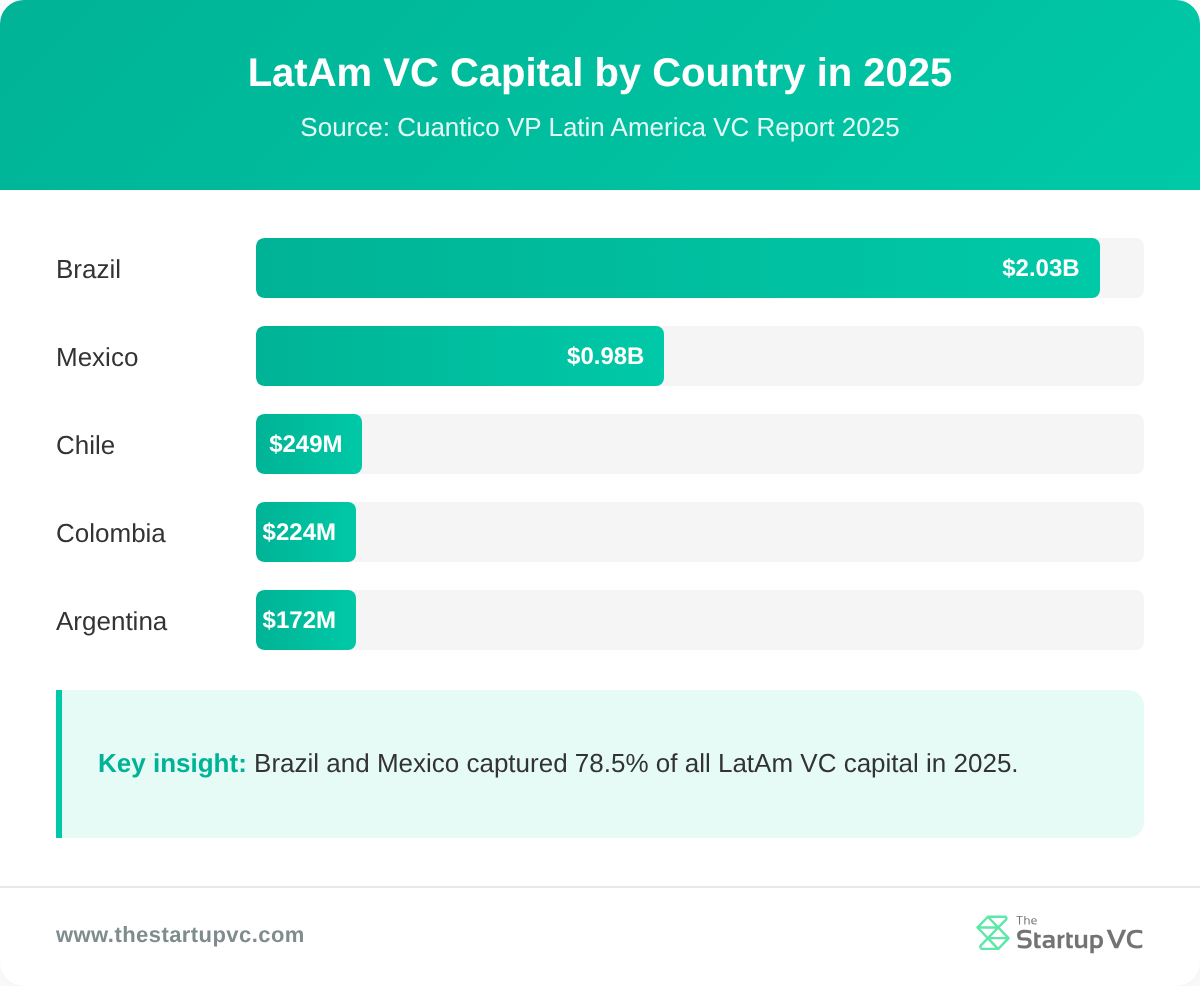

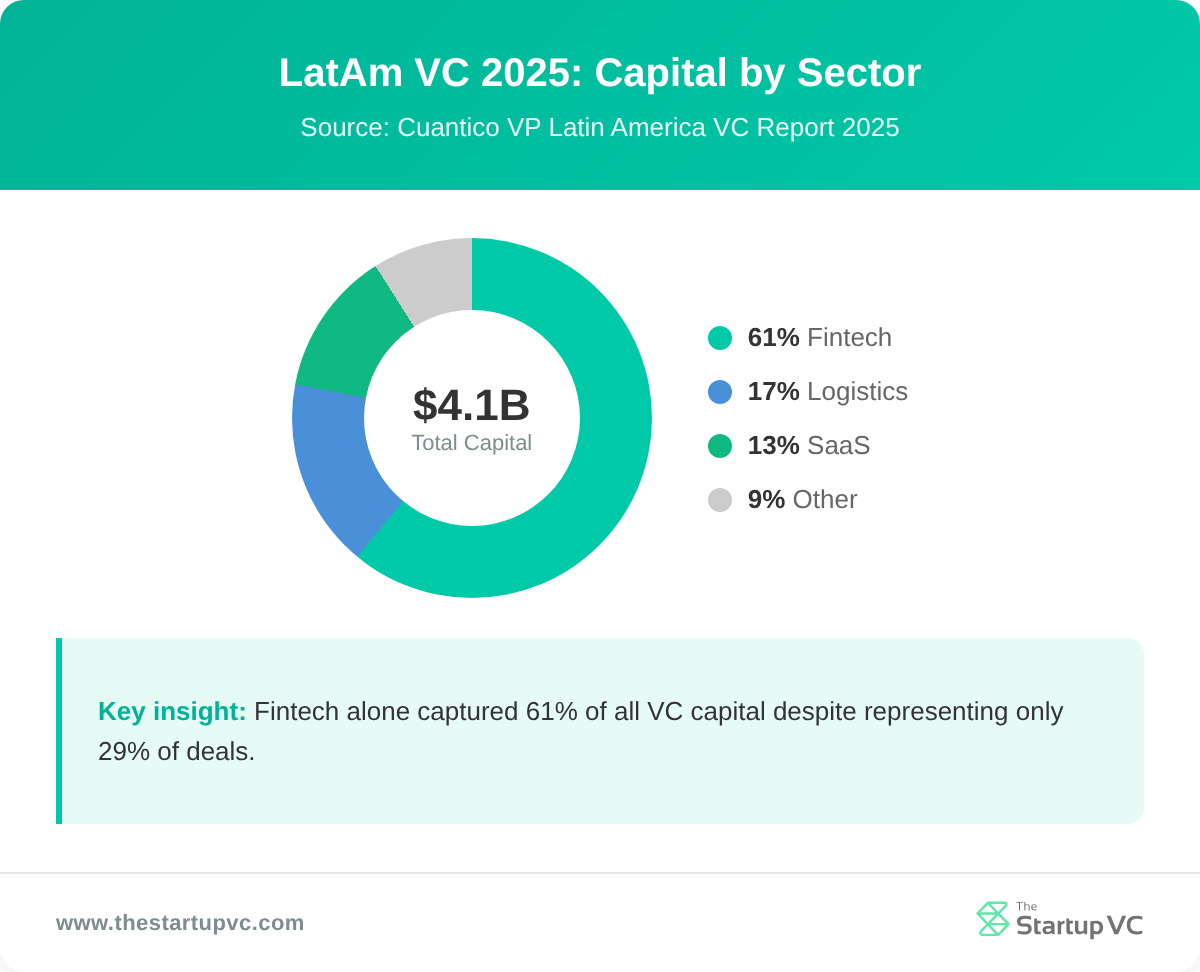

The most VC capital in LatAm went to Brazil and Mexico, which together captured 78.5% of all regional funding. Fintech dominated by sector, taking 61% of total capital despite representing only 29% of deals.

Which Countries Led in 2025?

Brazil led with US$2.032 billion across 363 deals, capturing 52.9% of all VC capital in the region. São Paulo remained the dominant hub. Mexico ranked second with US$980 million across 86 deals (25.5% of total).

The table below shows the full country breakdown:

| Country | Capital (US$M) | Deals | Share of Total | Avg. Ticket |

|---|---|---|---|---|

| Brazil | 2,032 | 363 | 52.9% | US$5.6M |

| Mexico | 980 | 86 | 25.5% | US$11.4M |

| Chile | 249 | 53 | 6.0% | US$4.7M |

| Colombia | 224 | 62 | 5.4% | US$3.6M |

| Argentina | 172 | 34 | 4.2% | US$5.1M |

Mexico’s average ticket size of US$11.4 million was the highest in the region. That reflects fewer but larger rounds, particularly in fintech and logistics. For a broader look at where venture capital is going in Latin America, see the full overview on The Startup VC.

Which Sectors Won the Most Investment?

Fintech captured 61% of total VC capital in LatAm while representing only 29% of deals. The top three fintech rounds were Plata (US$250M Series B), Klar (US$170M Series C), and Omie (US$160M Series D). Together, they totaled US$580 million.

SaaS ranked second with 13% of both deals and capital. Logistics captured 17% of capital despite only 5% of deals, reflecting a few very large infrastructure rounds. Energy took 10% of capital across 4% of deals.

| Sector | Deal Share | Capital Share |

|---|---|---|

| Fintech | 29% | 61% |

| SaaS | 13% | 13% |

| Logistics | 5% | 17% |

| Energy | 4% | 10% |

| Healthtech | 7% | 3% |

How Does the 2025 LatAm VC Environment Compare to Previous Years?

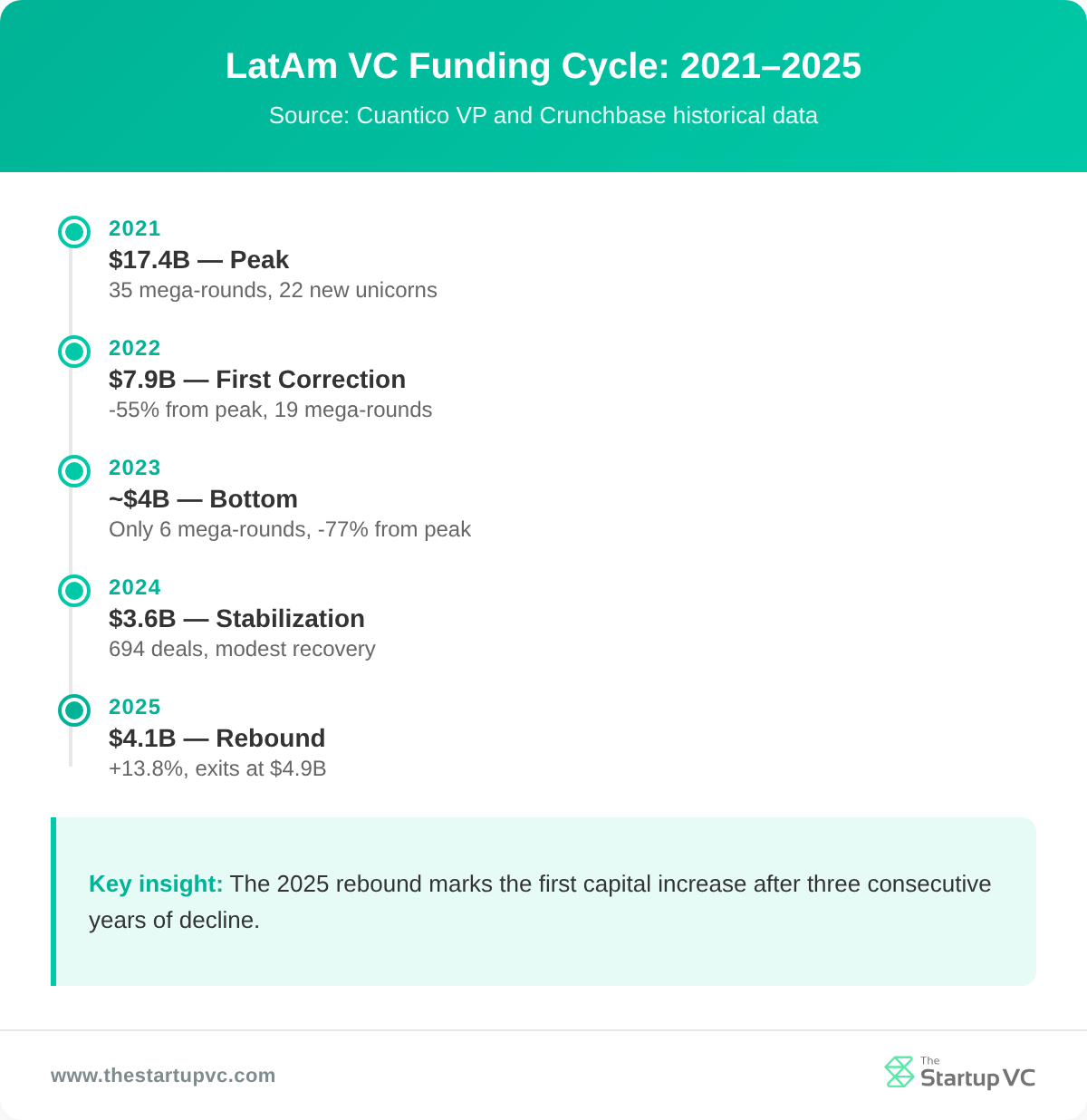

The 2025 numbers represent a recovery, but a partial one. LatAm VC is still 76% below its 2021 peak. The market has moved from a sharp correction to a cautious rebound.

What Happened at the 2021 Peak?

LatAm VC peaked at US$17.381 billion in 2021. Low interest rates and pandemic-era digitalization drove that surge. Thirty-five mega-rounds (over US$100 million) closed that year. Twenty-two new unicorns were created. It was an anomaly, not a baseline.

What Did the 2022-2023 Correction Look Like?

The correction was severe. Investment fell to US$7.9 billion in 2022, a 55% drop from the peak. It declined further to approximately US$4 billion in 2023, a total 77% collapse from the peak.

In 2023, only 6 mega-rounds closed, down from 19 in 2022 and 35 in 2021. Many startups that raised at 2021 valuations could not raise follow-on rounds. Portfolios stagnated.

Where Does 2025 Fit in the Recovery?

The table below maps the full cycle:

| Year | Total Capital | Deals | Notable Signal |

|---|---|---|---|

| 2021 | US$17.4B | ~1,000+ | Peak: 35 mega-rounds, 22 unicorns |

| 2022 | US$7.9B | ~900 | First correction: 55% drop |

| 2023 | ~US$4B | ~750 | Bottom: only 6 mega-rounds |

| 2024 | US$3.6B | 694 | Stabilization: modest recovery |

| 2025 | US$4.1B | 681 | Rebound: 13.8% capital growth |

José Kont of Cuantico VP has noted that 2026 and 2027 should bring more liquidity to the region. Exit activity in 2025 reached US$4.9 billion, the third-best year on record. That supports that view.

How Should Founders Raise Funding in LatAm’s 2026 Environment?

Founders raise successfully in 2026 by proving execution, not telling a story. Capital is now priced around measurable results. Investors want repeatable go-to-market, clean unit economics, and governance that holds up under real due diligence.

What Metrics Matter Most to LatAm Investors in 2026?

The metrics that matter most are unit economics, revenue traction, and capital efficiency. Investors look for startups with strong margins, low customer acquisition costs, and high retention. A startup with messy financials will struggle to close a round, regardless of market size or product quality.

Traction matters more than vision. Founders must show repeatable growth, not a spike from a single customer or campaign. Follow-on raises are now conditional on capital efficiency, not just survival. Weak unit economics and overvaluation are the most common red flags cited by LatAm investors.

How Should Founders Prepare for a 2026 Round?

You should prepare by addressing five key areas before starting the raise process:

- Plan runway assuming no follow-on. Build 18 to 24 months of runway before starting a raise. Investors can tell when a founder is raising from desperation.

- Show repeatable go-to-market. Isolated wins do not close rounds. Investors want to see that the sales engine works consistently across multiple customers or markets.

- Build governance early. Maintain financial reporting and cap table clarity. Investors conduct real diligence now. Sloppy records create doubt.

- Use warm introductions. Cold outreach converts at low rates in LatAm. A warm introduction from a portfolio founder or advisor dramatically improves access.

- Consider venture debt. Venture debt has emerged as a significant non-dilutive financing option, particularly for fintech companies. It can extend runway without diluting equity.

Founders targeting Series A or B rounds should focus on Brazil and Mexico, where 78.5% of capital concentrates. Colombia and Chile offer opportunities at seed stage, particularly for fintech and climate tech startups. Understanding why Latin American startups are having to change and evolve helps frame the mindset shift required in 2026.

What Questions Do Startup Founders Ask Most Often About LatAm VC in 2025 and 2026?

How much did LatAm VC grow in 2025?

LatAm VC grew 13.8% in 2025, reaching US$4.126 billion across 681 rounds. That is the first meaningful recovery after three years of decline from the 2021 peak of US$17.4 billion.

Why did deal count fall if total funding rose?

Deal count fell because investors concentrated capital in fewer, stronger companies. The average round size grew 16%, from US$5.2 million to US$6.1 million. Investors backed quality over volume.

Which sectors have the best chances of raising VC in LatAm in 2026?

The sectors with the best chances are fintech, SaaS, and logistics. Fintech captured 61% of all VC capital in 2025. SaaS and logistics also showed strong round sizes relative to deal count.

How long does fundraising take for LatAm startups in 2025?

Fundraising takes six to twelve months for most startups. Around 24.5% of founders who completed a round spent that much time closing it. Another 30.6% were still in process. Plan your timeline accordingly.

Do LatAm investors prefer first-time or repeat founders?

Repeat founders have a clear advantage. Serial entrepreneurs accounted for 42% of capital deployed in 2023 and 2024, versus 23% in 2021. First-time founders need stronger traction to compensate.

Is it better to raise equity or venture debt in 2026?

It depends on your stage and sector. Equity rounds remain the primary funding path. Venture debt is growing fast in LatAm. It is especially useful for fintech startups that need non-dilutive capital to scale.

Ready to Raise in Latin America’s Evolving VC Market?

The LatAm VC market is recovering, but the rules have changed. Investors are backing fewer companies. The ones that get funded have strong traction, clean finances, and experienced operators.

The Startup VC is Craig Dempsey’s family office and company builder. Craig creates, backs, and scales ventures across Latin America. The Startup VC portfolio includes Biz Latin Hub, which operates in 17 countries with on-the-ground teams across the region.

If you are building a startup in Latin America and want practical, experience-backed guidance, Contact us today.