Corporate Venture Capital now backs 15% of startup deals in Latin America, with CVC activity doubling between 2020 and 2023.

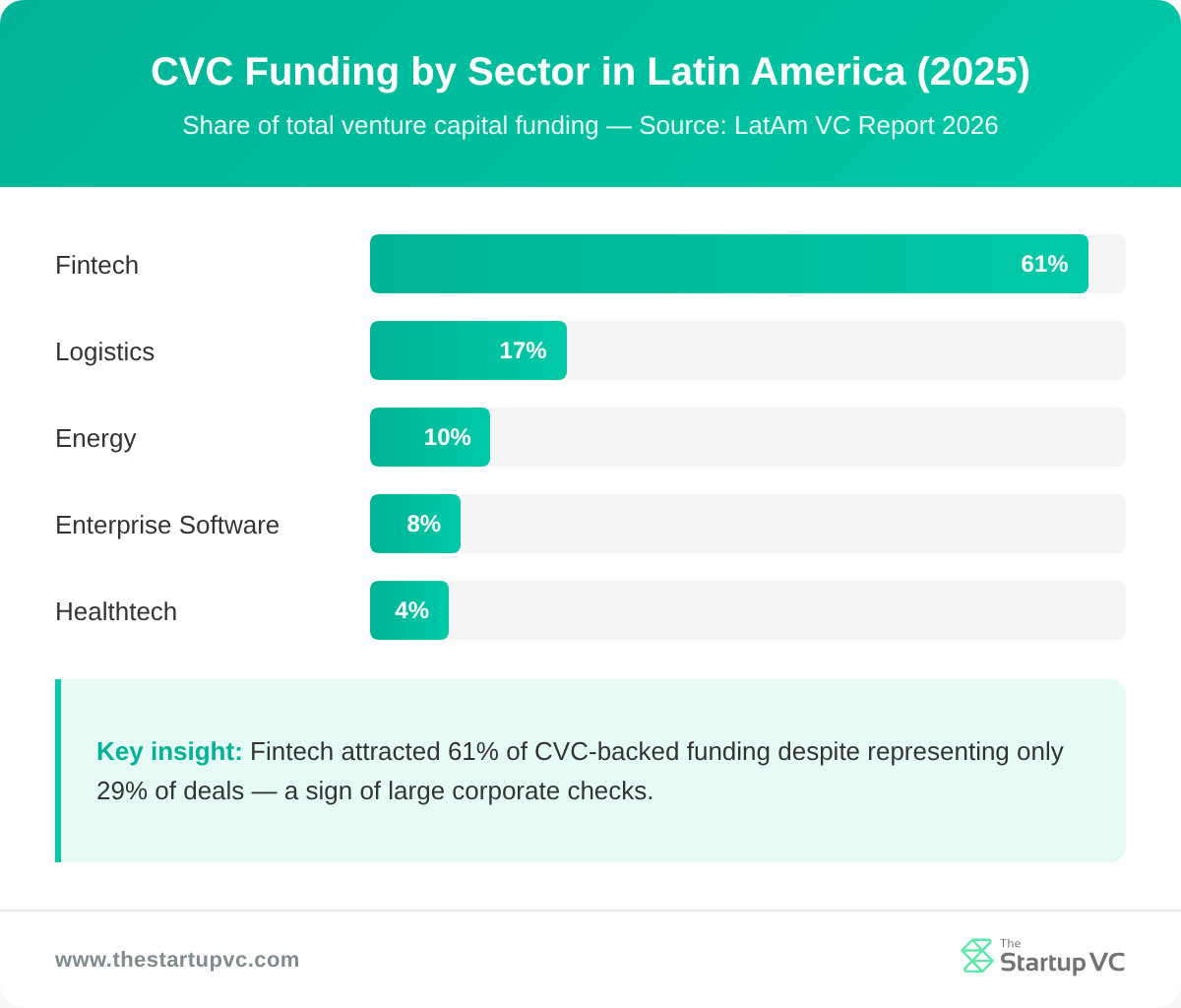

By 2025, LatAm CVCs from companies like Mercado Libre, Credicorp, FEMSA, and Telefónica had invested in over 150 startups across the region. Fintech captured 61% of CVC-backed funding. Corporate teams became more autonomous and selective, investing with clear strategic mandates.

The Startup VC tracks venture capital trends across Latin America and works directly with founders navigating institutional and corporate fundraising. This guide covers how CVC works, which sectors are most active, and how to approach a corporate investor without giving up strategic independence.

What Is Corporate Venture Capital and How Does It Work in Latin America?

Corporate Venture Capital (CVC) is a form of investment where large companies fund startups directly in exchange for equity. Unlike traditional venture capital, which focuses on financial returns alone, CVC combines capital with strategic assets. These assets include distribution networks, procurement pipelines, and market access.

In Latin America, CVC has grown quickly. CVC activity in the region doubled between 2020 and 2023. By 2023, corporate investors participated in 15% of all venture capital deals across LatAm.

The structure of LatAm CVCs varies. 53% maintain separate venture and partnering programs. 44% conduct technology scouting. 49% operate internal venture-building programs. Some CVCs act purely as financial co-investors. Others take a hybrid approach, combining investment with co-development and pilot programs.

The most active LatAm CVC arms include:

| Corporate | CVC Arm | Focus | Scale |

|---|---|---|---|

| Mercado Libre | CVC Fund | E-commerce, fintech | 27 portfolio companies, $9B+ combined valuation |

| Telefónica | Wayra | Digital entrepreneurship | €233M invested, 1,100+ startups, 7 hubs |

| Cencosud | Cencosud Ventures | Retail, fintech | Chile-based, Andean region |

| Credicorp | Krealo | Fintech | 26 investments, Andean region |

| FEMSA | FEMSA Ventures | Logistics, retail | 26 investments, latest Cayena Series B 2024 |

| CMI | CMI Ventures | Renewable energy, food tech | Central America focus |

Other corporations actively co-investing in LatAm rounds include FEMSA, Qualcomm, Citi Ventures, and Globo. SoftBank remains the largest single investor in the region across IT, consumer, financial services, and transport sectors.

What Makes CVC Different From a Traditional VC in Practice?

CVC is different from traditional VC in that the investor has a strategic agenda beyond returns. A traditional VC wants a financial exit. A CVC also wants a business outcome. That outcome might be adopting the startup’s technology internally. It might also mean using the startup as a distribution partner or positioning for a future acquisition.

This dual agenda shapes every part of the relationship: the diligence process, the terms, the support offered, and the timeline.

Why Have LatAm Corporations Shifted From Occasional Investors to Consistent Early-Stage Players?

LatAm corporations shifted because of three converging pressures: digital transformation demands, traditional VC pullback, and rising competition from global technology companies.

Between 2022 and 2023, traditional VC funds scaled back their LatAm activity significantly. Corporate investors stepped in. Pre-Seed and Seed rounds accounted for over 80% of all LatAm deals that period. Corporates kept the early-stage market alive.

Three industries drove this shift:

- Banking. Digital challengers threatened core revenue. CVCs funded fintech startups to stay relevant.

- Retail. E-commerce competition demanded faster technology adoption across logistics and payments.

- Energy and logistics. Infrastructure companies needed software they could not build internally.

How Did CVC Teams Professionalize in LatAm?

LatAm CVC teams professionalized by building autonomous deal structures and defined investment mandates by late 2025. They stopped investing opportunistically. They tightened investment criteria around core business adjacency. They set clear expectations for governance, collaboration timelines, and pilot program outcomes.

This professionalization changed how founders experience CVC conversations. Earlier interactions were informal and slow. By 2025, structured processes and dedicated deal teams had become the norm. The most active LatAm CVCs set up defined portfolio management practices.

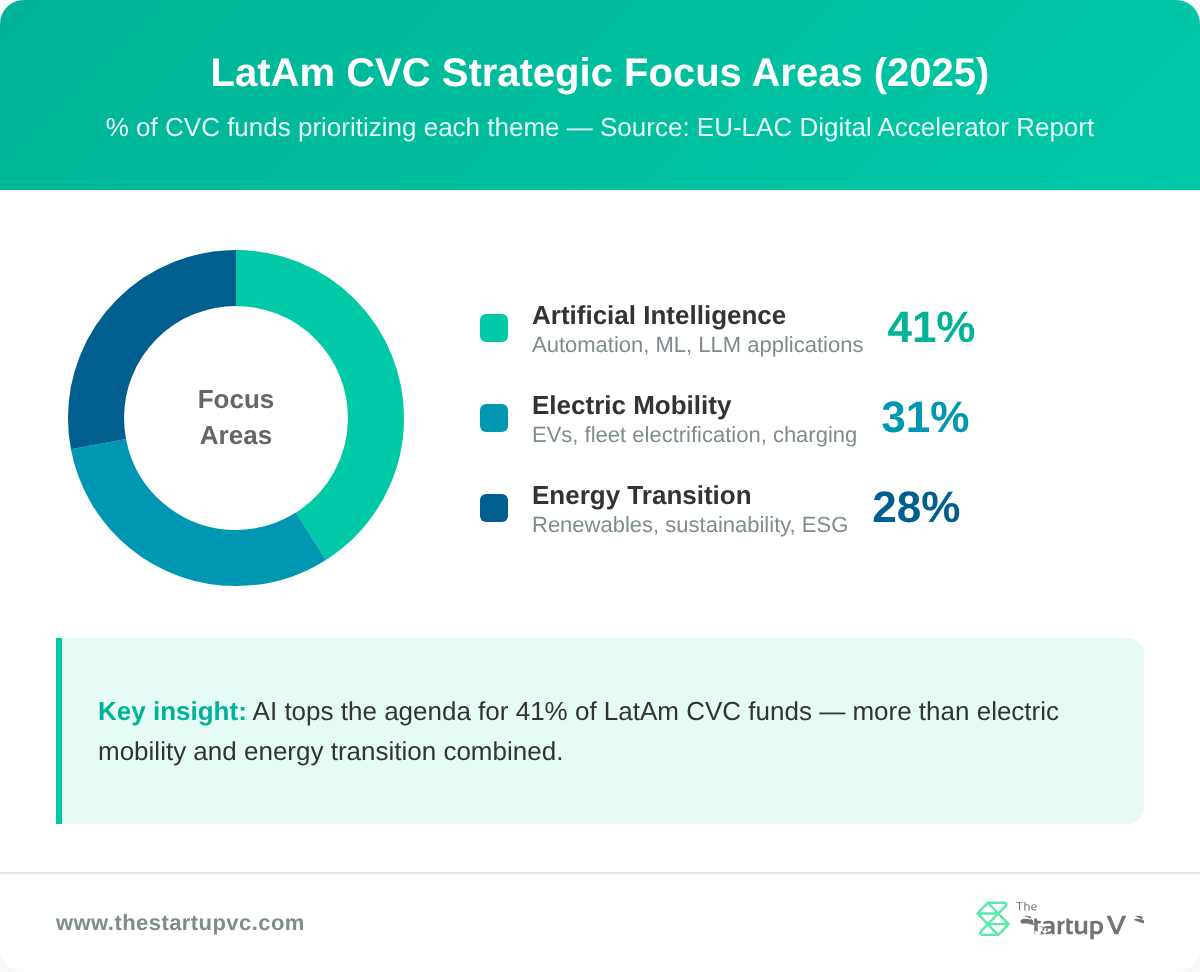

What Themes Are Driving CVC Portfolio Construction in 2025?

The themes driving CVC portfolio construction in 2025 reflect the strategic priorities of LatAm’s largest companies. 41% of LatAm CVC funds prioritize AI investments. 31% are backing electric mobility startups. Another 31% focus on sustainability and energy transition technologies.

These themes are not coincidental. They map to the pressures facing LatAm corporates: regulatory requirements on energy, competitive threats from e-commerce, and internal cost optimization through AI tools.

Which Sectors Are Attracting the Most Corporate Venture Capital in Latin America?

The sectors attracting the most corporate venture capital in Latin America are fintech, logistics, energy, enterprise software, and healthtech. These sectors share a common characteristic: they sit at the intersection of digital transformation and core corporate operations.

The table below shows corporate-backed investment distribution in Latin America:

| Sector | Share of Funding | Share of Deals | Notable Corporate Investors |

|---|---|---|---|

| Fintech | 61% | 29% | Krealo, Citi Ventures, Mercado Libre |

| Logistics | 17% | 5% | FEMSA Ventures, Güil (Kaufmann), CMI Ventures |

| Energy | 10% | 4% | CMI Ventures, SQM Lithium Ventures |

| Enterprise Software | Emerging | 14 rounds | SoftBank, Mercado Libre |

| Healthtech | Second most active vertical | High deal activity | Multiple CVCs and hybrid funds |

Why Does Fintech Attract the Most CVC Activity?

Fintech attracts the most CVC activity because it sits directly inside the operations of the most active corporate investors: banks, retailers, and telecom companies. Krealo is the CVC arm of Credicorp, Peru’s largest financial group. It has built a portfolio of 26 fintech investments in the Andean region. Its mandate is clear: find startups that complement Credicorp’s existing services.

Fintech in LatAm attracted an estimated US$2.8 billion in 2025, capturing 61% of all venture funding with only 29% of deals. The high funding-to-deal ratio reflects large ticket sizes from corporate co-investors.

What Is Driving Corporate Investment in Logistics and Energy?

Corporate investment in logistics and energy is driven by infrastructure complexity and the need for faster technology adoption. Logistics and energy companies cannot easily build software internally. They acquire it or fund its development by investing in startups.

FEMSA Ventures, backed by FEMSA, focuses on logistics, retail, and beverage distribution startups across Latin America and the United States. Its latest logistics investment was Cayena’s Series B round in September 2024. CMI Ventures is the CVC arm of Corporación Multi Inversiones in Central America. It focuses on renewable energy, food technology, and next-generation logistics. SQM Lithium Ventures is the most active Chilean corporate investor in the energy sector.

Logistics attracted 17% of LatAm CVC funding in 2023–2025. Energy attracted 10%. Both show higher average deal sizes than the sector averages, reflecting infrastructure-intensive business models that require larger checks.

How Is Healthtech Emerging as a Corporate Investment Target?

Healthtech is emerging as a corporate investment target by attracting hybrid equity and debt structures from companies addressing LatAm’s healthcare delivery gaps. Healthtech ranked as the second most active vertical in LatAm in 2024–2025. Rounds reached up to US$400 million. Companies combining healthcare delivery with financing solutions attracted the most CVC attention.

FEMSA invested MX$2.6 billion in its health division in 2025 through its YZA, FM Moderna, and Cruz Verde pharmacy chains. This was a 44% increase from 2024. Funds went to warehouse expansion and technology upgrades.

How Does Strategic Capital From a CVC Differ From Financial Capital From a Traditional VC?

Strategic capital from a CVC differs from financial capital in that it comes with a corporate agenda attached. Traditional VCs provide money and expect financial returns. CVCs provide money and expect strategic outcomes. These can include technology access, market entry, competitive intelligence, or positioning for an acquisition.

This difference matters for founders. It changes what you need to prove, what the investor will help you with, and how long they will stay on your cap table.

What Does a CVC Actually Offer Beyond Cash?

A CVC offers distribution channels, procurement pipelines, customer introductions, and operational expertise beyond cash. The most valuable benefit is often the fastest: the corporate becoming an early anchor customer. This cuts the startup’s sales cycle and provides reference revenue that validates the business for other investors.

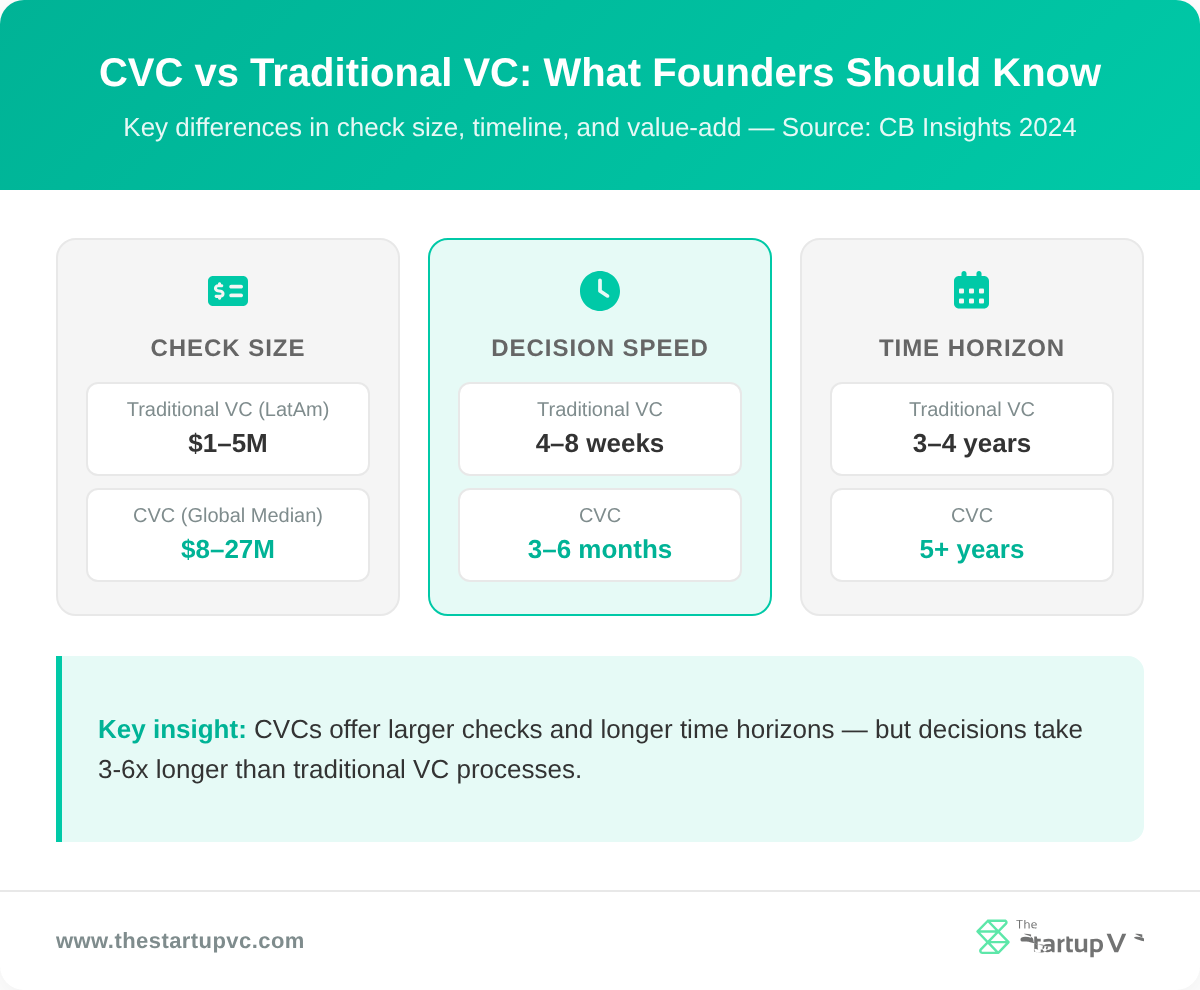

The table below compares what traditional VCs and CVCs typically offer:

| Dimension | Traditional VC | CVC |

|---|---|---|

| Primary goal | Financial returns | Financial returns + strategic value |

| Check size | $1–5M (seed/Series A in LatAm) | $8–27M average globally |

| Investment horizon | 3–4 years | 5 years or more |

| Value-add | Networks, board experience | Distribution, customers, operations |

| Exit preference | IPO or acquisition by third party | May prefer internal acquisition |

| Decision speed | 4–8 weeks typical | 3–6 months typical |

Do Startups With CVC Backing Perform Better?

Startups with CVC backing perform better on survival and exit outcomes. Research cited by BBVA Spark shows that companies with corporate investors had their risk of bankruptcy cut in half. They also showed higher exit multiples in acquisition and IPO scenarios. This is partly because corporate investors provide strategic support that reduces business risk. It is also because a corporate investor signals market validation to other buyers.

In 2024, the average global CVC deal reached $27.3 million, a 34% year-over-year increase. The median deal size was $8.6 million. Both figures exceed the average LatAm seed check, which grew from $1.27 million in 2024 to $1.73 million in 2025. CVCs typically co-invest alongside traditional VCs rather than leading solo rounds.

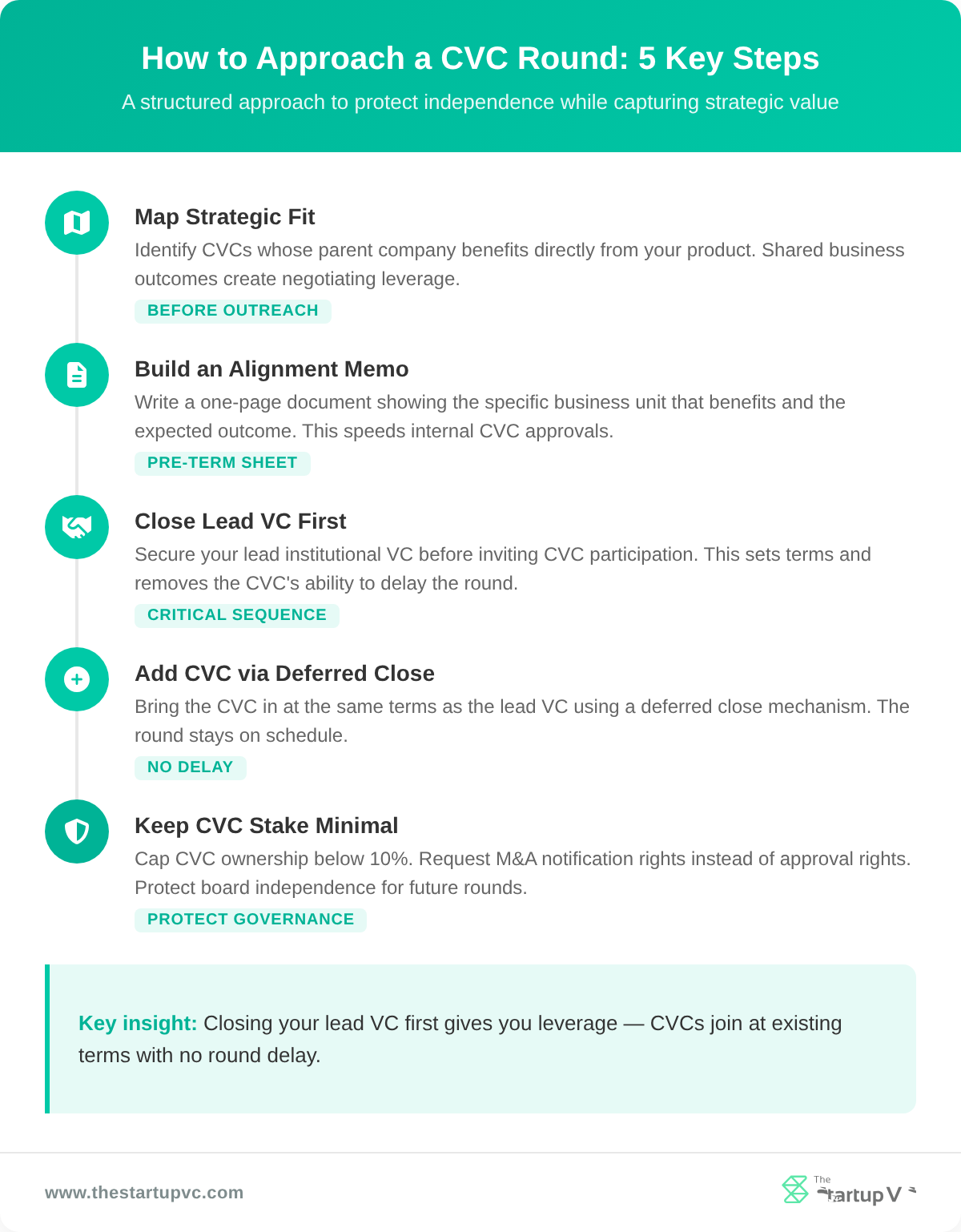

How Should Founders Approach a CVC Round Differently Than a Traditional VC Round?

Founders should approach a CVC round by starting with strategic fit, not funding need. A traditional VC evaluates market size, traction, and team. A CVC evaluates all of those things and also asks: what does this startup do for our business? If you cannot answer that question clearly, the CVC conversation will stall.

How Do You Identify the Right CVC for Your Startup?

You identify the right CVC for your startup by mapping your product’s value against the corporate’s active strategic challenges. Research the corporate investor’s business. What does it sell? Where does it compete? What problems is its board discussing publicly? Then build a short strategic alignment memo. Show three to five specific synergies: a distribution opportunity, a cost-reduction use case, or a shared customer segment.

LatAm CVCs by sector include:

- Fintech: Krealo (Andean region), Citi Ventures, Mercado Libre CVC

- Logistics and retail: FEMSA Ventures (Mexico, LatAm), Güil (Kaufmann, Chile)

- Energy: CMI Ventures (Central America), SQM Lithium Ventures (Chile)

- Telecom and digital: Wayra Hispam (Telefónica, 5 LatAm countries)

What Terms Should Founders Watch Out For in a CVC Deal?

Founders should watch for four specific CVC term risks: IP transfer clauses, exclusivity restrictions, right of first refusal (ROFR), and market tagging.

IP transfer clauses. Some CVCs include terms stating that if the startup fails, all intellectual property transfers to the corporate. Push back on this immediately. It creates a perverse incentive for the investor to watch you fail.

Exclusivity restrictions. Avoid clauses that prevent you from working with the corporate’s competitors. This limits your market and signals to other potential customers that you are tied to one player.

ROFR on acquisitions. A right of first refusal requires you to share all acquisition details with the CVC before accepting any offer. Negotiate instead for an M&A Notification clause. This requires only notifying the CVC that an offer exists. You do not have to disclose the buyer or price.

Market tagging. If one corporate holds significant equity, potential customers in that corporate’s competitive space may avoid you. Mitigate this by bringing two or more CVCs from different (non-competing) sectors onto the same round.

How Do You Manage the CVC’s Slower Approval Process?

You manage the CVC’s slower approval process by structuring your round so that it does not depend on the CVC’s timeline. CVCs involve multiple business units in their investment decisions. Approval cycles run three to six months, compared to four to eight weeks for traditional VCs.

Use a deferred closing structure: allow the CVC to join the round after the primary close. This means your lead investor and other co-investors commit and close first. The CVC signs later, at the same terms. This approach protects your runway and removes pressure from both sides.

Keep CVC ownership small. The strategic benefits (customers, distribution, market access) are the same whether the corporate holds 1% or 10% of your cap table. Keeping the stake small limits their governance influence while capturing the full value of the relationship.

What Questions Do Startup Founders Ask Most Often About Corporate Venture Capital in Latin America?

How much do LatAm CVCs typically invest per deal?

LatAm CVCs typically co-invest checks ranging from $500,000 to $5 million at seed and Series A. Global CVC median deal size reached $8.6 million in 2024. LatAm CVC checks tend to be smaller. CVCs rarely lead rounds solo. They join alongside traditional VCs or impact funds.

Is CVC money “smart money” in Latin America?

CVC money is smart money when the corporate has direct strategic relevance to your business. The value comes from customers, distribution, and pilots. It is not smart money if the corporate is investing purely for financial exposure with no operational connection to your space.

How long does a CVC deal take to close in Latin America?

A CVC deal in Latin America takes three to six months to close. This is longer than traditional VC processes. Multiple business units review the investment, including strategy, finance, legal, and sometimes the relevant business division. Plan for this timeline and use deferred closing to protect your round.

Can a CVC investment make it harder to raise future rounds?

A CVC investment can make future rounds harder if it signals exclusive alignment with one corporate. Other corporate investors in the same space may avoid co-investing if they see a competitor on your cap table. Mitigate this by bringing multiple CVCs from different sectors onto the same round early.

What do LatAm CVCs look for in early-stage startups?

LatAm CVCs look for startups in sectors adjacent to their core business, with clear synergy pathways. They evaluate cap table structure, governance, team experience, and the startup’s fit with the corporate’s customer base or technology roadmap. Founders with a clear strategic alignment memo close CVC conversations faster.

Should founders approach CVCs before or after traditional VCs?

Founders should approach traditional VCs first, then bring in CVCs as co-investors in the same round. Having a lead VC creates leverage. It signals validation and sets a market price. This gives you a better negotiating position with CVCs and speeds up their internal approval process.

Ready to Raise Strategic Capital in Latin America?

The Startup VC is Craig Dempsey’s family office and company builder, focused on scalable ventures across Latin America. We have direct experience navigating CVC conversations, structuring rounds with corporate co-investors, and protecting founder independence through deal terms. Whether you are approaching your first corporate investor or building a mixed VC and CVC cap table, we can help you structure the right conversation. Contact us today to discuss your raise.