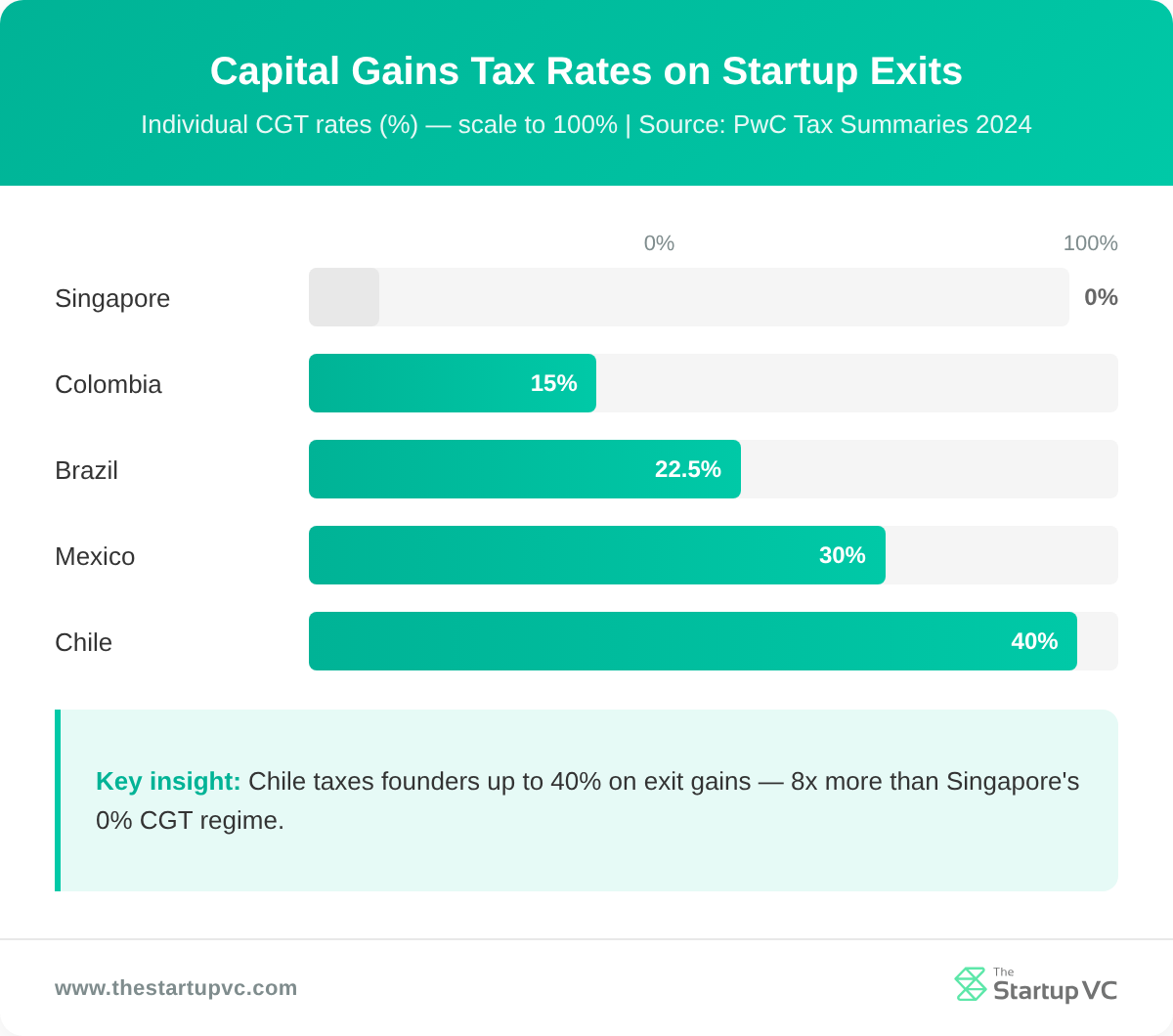

Startup exit regulations vary by country, with capital gains tax ranging from 0% in Singapore to 40% in Chile.

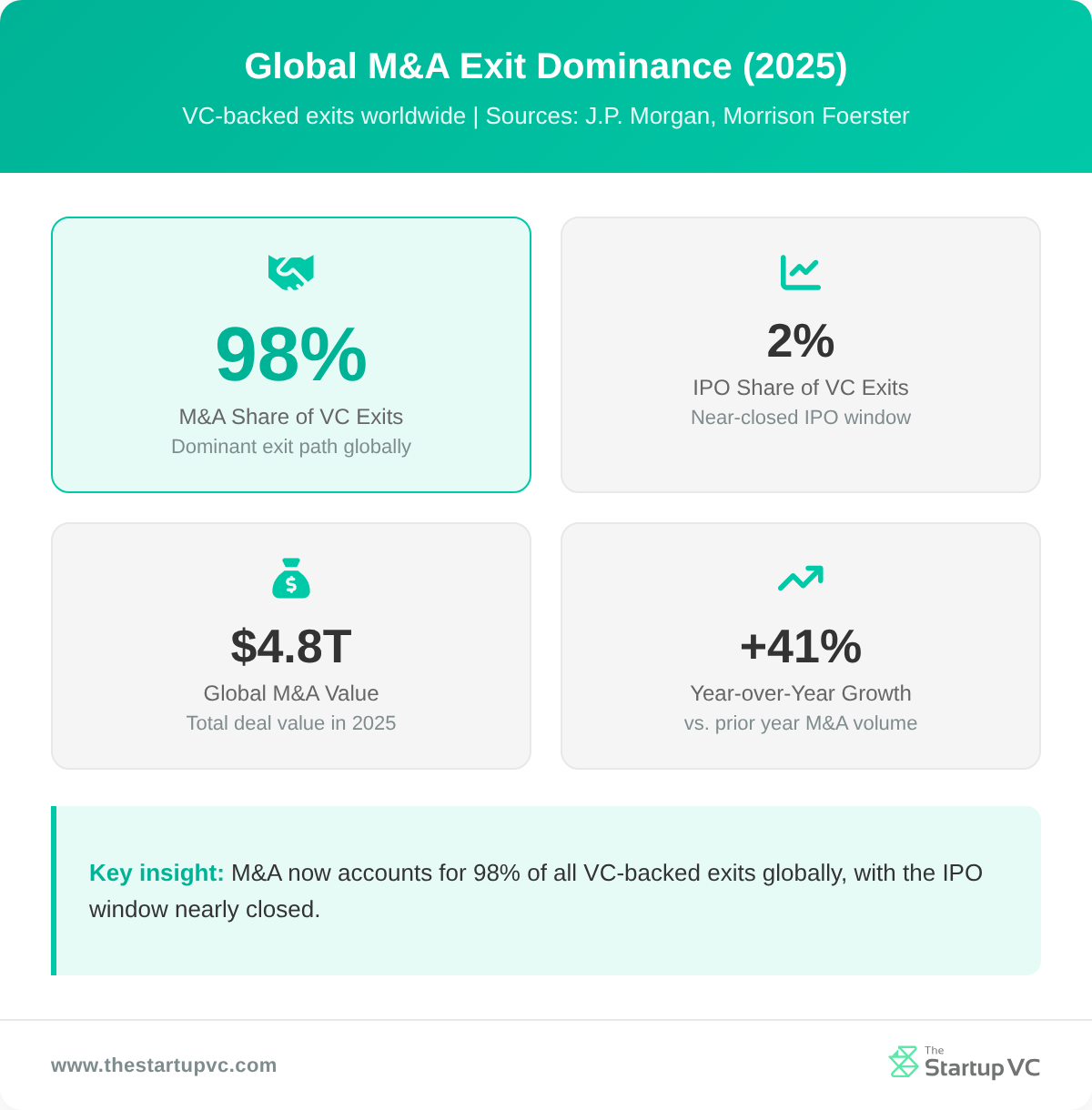

M&A accounts for 98% of VC-backed exits globally as of H1 2025. Capital gains tax rates range from 0% in Singapore to 40% in Chile. Cross-border deals require CFIUS, EU FDI screening, and up to 24 months of regulatory review.

The country where a startup is incorporated shapes every aspect of its exit. It determines how much founders keep and how long a deal takes to close. The Startup VC has built and guided ventures across Brazil, Colombia, Mexico, and Chile. Below, you will find a country-by-country comparison of CGT rates and investor protection laws. Cross-border deal rules and practical guidance for Latin American founders are also covered.

What Is a Startup Exit and Why Does Regulation Matter?

A startup exit is the process by which founders and investors convert their equity into cash or acquirer shares. The three main exit routes are mergers and acquisitions (M&A), initial public offerings (IPOs), and secondary sales. Each route operates under a different set of legal rules. Those rules determine how fast a deal closes, how much founders keep, and whether the deal happens at all.

What Are the Main Types of Startup Exits?

The main exit types are M&A, IPOs, and secondary sales. M&A is by far the most common route. It accounts for 98% of VC-backed exits as of H1 2025, up from 90% in 2015. In an M&A exit, a strategic or financial buyer acquires the startup outright. The deal is governed by corporate law, tax law, and national security review rules.

IPOs let founders list shares on a public stock exchange. They peaked at 14% of venture-backed exits in 2021. By 2024, that share had fallen to just 2%. IPOs require compliance with securities law in the listing country. That adds substantial legal cost and time.

Secondary sales allow early shareholders to sell existing shares to new private buyers. They provide liquidity without a full company sale. Private equity buyouts follow a similar structure. They have grown as a substitute for IPOs among later-stage startups.

Why Do Regulations Shape Exit Outcomes?

Regulations shape exit outcomes because they determine deal speed, retained proceeds, and available buyer pools. A well-structured legal environment can cut a deal timeline from 18 months to 3 months. A hostile one can kill the deal entirely.

Regulatory scrutiny adds 3 to 6 months to typical M&A timelines. Contested cross-border deals can take 12 to 24 months due to antitrust reviews and national security approvals. Tax law determines what percentage of proceeds founders keep. Corporate law determines whether minority shareholders can block a deal.

Global M&A value reached $4.8 trillion in 2025. That is a 41% increase from 2024 and the second-highest annual total on record. The regulatory environment in each country shapes which of those deals close smoothly and which stall.

How Do Capital Gains Tax Rules Shape Exit Proceeds Across Countries?

Capital gains tax rules shape exit proceeds by setting the percentage of sale value founders and investors actually keep. The difference between a 0% CGT regime and a 40% one is not a minor detail. On a $10 million exit, that gap is $4 million. Founders who understand CGT rules before structuring their company can plan to keep significantly more.

Which Jurisdictions Offer Low or Zero Capital Gains Tax on Exits?

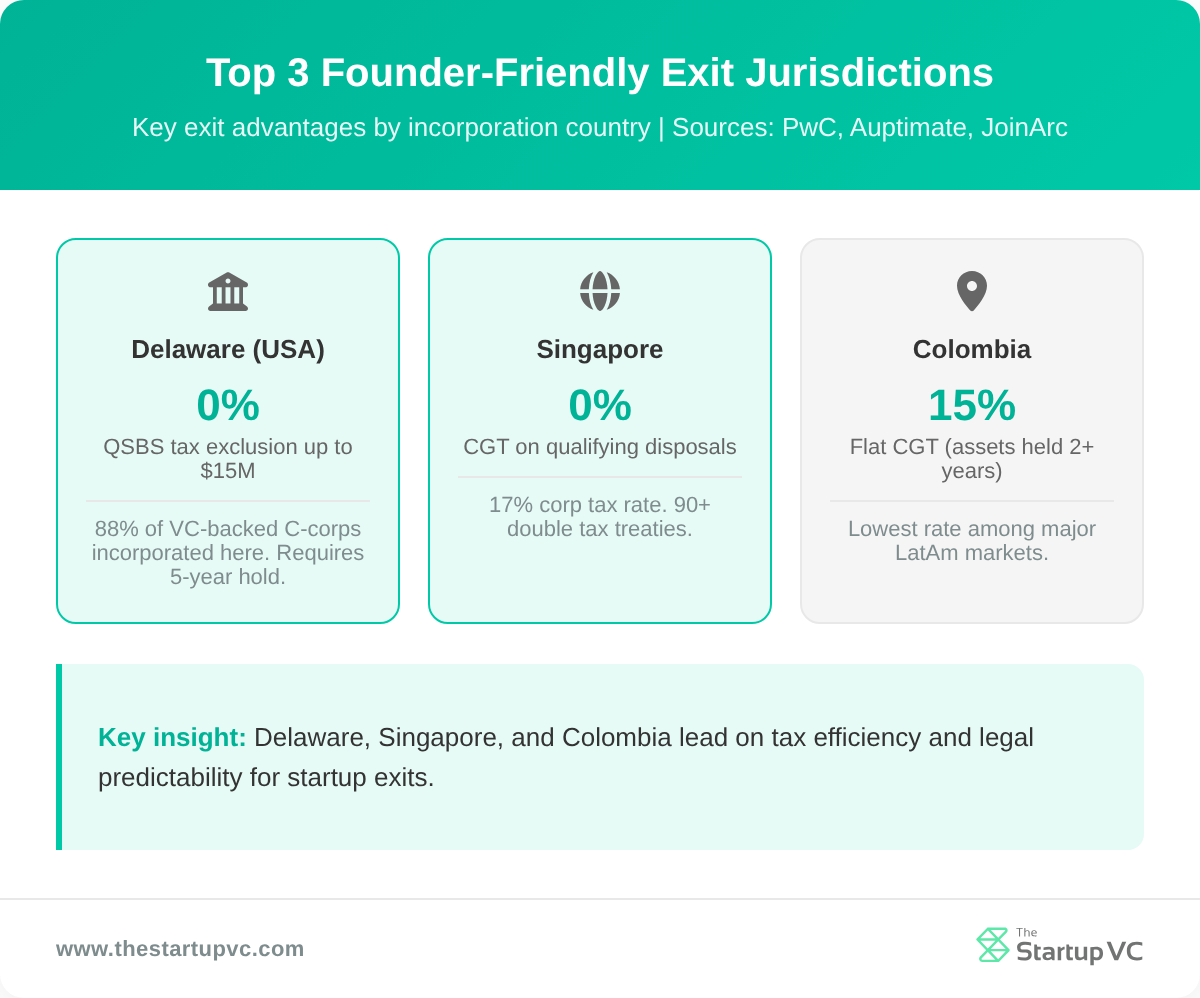

The best CGT environments for startup exits are Singapore and the United States under specific conditions. Singapore imposes no capital gains tax on qualifying investment disposals. That makes it the default holding company location for many Asia-Pacific and Latin American founders planning future exits. From January 2024, Singapore introduced an economic substance requirement. Gains from foreign asset sales become taxable if received in Singapore without real local operations. The safe harbour requires holding at least a 20% stake for 24 or more months.

The United States taxes individual long-term capital gains at 0%, 15%, or 20% depending on income. That rate alone is not the full story. Founders holding qualifying Delaware C-Corp stock for five or more years may exclude up to $15 million from federal tax. This is the Qualified Small Business Stock (QSBS) exclusion. It is one of the most powerful tax benefits available to startup founders globally. Corporations in the US pay 21% on gains, with no equivalent exclusion.

How Do Latin American CGT Rates Compare?

Latin American CGT rates compare by showing a wide range. Individual rates run from 5% in Peru to 40% in Chile. Most rates are higher than Singapore or the US long-term rate. The table below shows individual and corporate CGT rates across the region’s main startup markets.

| Country | Corporate CGT Rate | Individual CGT Rate | Key Condition |

|---|---|---|---|

| Colombia | 15% flat | 15% flat | Assets held 2+ years; otherwise ordinary income up to 39% |

| Brazil | 34% (CIT) | 15–22.5% | Complex FX repatriation rules apply |

| Mexico | 30% (CIT) | 25–35% withholding | Non-residents face higher withholding |

| Chile | Standard CIT | Up to 40% | One of the highest individual rates in LatAm |

| Peru | Standard CIT | 5% | One of the lowest individual rates in LatAm |

| Guatemala | 10% | 10% | Flat rate for both |

Colombia stands out as the most tax-efficient major market in the region for founders holding assets long-term. A flat 15% rate on gains from assets held more than two years is competitive by any global standard. Brazil’s corporate rate of 34% is the highest in the region. It is compounded by currency repatriation complexity, adding cost and time to any exit involving foreign acquirers.

Chile’s individual rate of up to 40% is among the highest in Latin America. Founders incorporated in Chile should plan their holding structures early. Mexico’s 30% corporate rate is standard, but non-resident buyers face 25–35% withholding on deal proceeds. That can affect deal terms and purchase price negotiations.

How Do Investor Protection Laws Affect Startup Acquisition Deals?

Investor protection laws affect startup acquisition deals by controlling who can block a sale. They also determine who gets paid first and how much each party receives. These rules differ significantly by jurisdiction. The country where a startup is incorporated, not where it operates, usually determines which rules apply.

How Do Liquidation Preferences Affect Exit Proceeds?

Liquidation preferences determine the order and amount in which investors are paid before founders and common shareholders. As of H1 2025, 93% of US VC deals use non-participating preferred liquidation preferences. That is up from 88% in 2020. Non-participating preferred means investors choose between two options. They can take their preference amount, or they can convert to common shares and receive their pro-rata share of proceeds. They cannot take both.

This structure protects investors in small exits. It also protects founders in large exits, because investors convert to common rather than stacking their preference on top. In contrast, participating preferred, common in some non-US jurisdictions, lets investors take both their preference and their pro-rata share. That structure can leave founders with very little in mid-size exits.

In Q3 2024, 100% of US venture deals included broad-based weighted average anti-dilution provisions. These clauses protect investors when a company raises at a lower valuation than a previous round. They reduce the conversion price of preferred shares, giving investors more common shares. Jurisdictions that allow stronger anti-dilution protections shift more exit value to investors.

How Do Drag-Along and Tag-Along Rights Work Across Jurisdictions?

Drag-along and tag-along rights work by giving majorities and minorities defined powers over a sale. In most major jurisdictions, including the US, UK, Australia, Singapore, UAE, and India, these rights are contractual, not statutory. Courts enforce them strictly as written. Precise drafting is essential.

Drag-along rights allow majority shareholders to compel minority shareholders to sell in an acquisition. In the US, they are typically triggered when 51–75% of voting shares approve the sale. The Delaware Supreme Court confirmed that drag-along clauses are fully enforceable when minorities agreed with legal counsel. This includes advance waivers of appraisal rights.

However, procedural compliance is mandatory. In Halpin v. Riverstone National (2015), a Delaware court voided a drag-along right entirely. The majority had failed to give advance notice as the agreement required. Tag-along rights work in reverse. They let minority shareholders join a sale on the same terms as the majority. Both rights are critical to structuring a clean exit.

How Did Delaware’s 2025 Law Reform Improve Deal Certainty?

Delaware’s 2025 Senate Bill 21 improved deal certainty by introducing statutory safe harbours for conflicted transactions. Signed on March 25, 2025, it overhauled the Delaware General Corporation Law (DGCL). The reform also added controller exculpation, meaning deals involving controlling shareholders now face clearer legal standards. Buyers and sellers have more certainty that an approved deal will not be challenged after closing.

Approximately 88% of C-corp startups on PitchBook were Delaware-incorporated in late 2024. This reform directly benefits VC-backed startups globally, including those operating in Latin America but incorporated in Delaware.

Which Countries Have the Most Founder-Friendly Exit Regulations?

The countries with the most founder-friendly exit regulations are Delaware (United States) and Singapore at the global level. No single country is perfect across all four dimensions. These are: low capital gains tax, predictable courts, fast deal timelines, and a deep acquirer pool. Founders must match their incorporation strategy to the exit environment they expect.

Which Global Jurisdictions Lead on Exit Regulation?

The two global leaders are Delaware (United States) and Singapore. Delaware dominates on legal infrastructure. It incorporated 80% of all US IPOs in 2023 and is home to 88% of VC-backed C-corps worldwide. The Delaware Court of Chancery is the most experienced corporate law court in the world. Deal disputes are resolved quickly and predictably. The QSBS exclusion adds a major tax benefit. Founders holding qualifying stock for five or more years can exclude up to $15 million of gain from federal tax.

The US and Europe together account for 73% of global startup exits. The US accounts for 35% and Europe for 38%. Both jurisdictions offer the deepest pools of strategic buyers and the most developed M&A legal infrastructure. A startup acquired by a US or European buyer can close faster than in most other markets.

Singapore leads on tax efficiency. It offers 0% capital gains tax on qualifying disposals, a 17% corporate tax rate, and tax-exempt dividends from qualifying subsidiaries. It also has more than 90 double taxation agreements. These reduce withholding taxes on cross-border exit proceeds. For Asia-Pacific and Latin American founders who plan exits to global buyers, a Singapore holding company is a widely-used structure.

How Do Latin American Countries Compare?

Latin American countries compare by showing improvement in regulatory speed but still lag behind Delaware and Singapore overall. Brazil has made the biggest regulatory progress. CADE, Brazil’s antitrust authority, reviewed a record 712 merger notifications in 2024. That is 20% more than 2023. Summary mergers averaged just 15.1 days for review. Ordinary mergers averaged 93.9 days. That speed is competitive for the region.

The table below compares the four largest Latin American startup markets on key exit-friendliness factors.

| Country | Max Individual CGT | Average M&A Timeline | Notable Feature |

|---|---|---|---|

| Colombia | 15% (assets held 2+ years) | Not publicly benchmarked | Most tax-efficient major LatAm market |

| Brazil | 22.5% individual / 34% corporate | 15–94 days (CADE, 2024) | Record M&A review speed; complex FX repatriation |

| Mexico | 30% (residents) | Not publicly benchmarked | 25–35% withholding for non-residents |

| Chile | Up to 40% (individuals) | Not publicly benchmarked | Highest individual CGT in major LatAm markets |

Colombia is the most tax-efficient major exit market in Latin America for founders who hold assets long-term. Brazil offers the fastest and most transparent antitrust review process in the region. Mexico and Chile present higher tax burdens, particularly for individual founders and non-resident acquirers.

Learn more about startup funding conditions in Latin America at The Startup VC.

Which Emerging Markets Are Becoming Founder-Friendly?

The most founder-friendly emerging markets are the UAE and Saudi Arabia. In Europe, France and the Nordic countries also deliver strong conditions. The UAE and Saudi Arabia have introduced founder-friendly tax and ownership policies for AI, fintech, and e-commerce ventures. The UAE offers 0% personal income tax and free zone structures that allow 100% foreign ownership.

In Europe, France, Sweden, and the Nordic countries consistently deliver strong startup exit outcomes. Their ecosystems combine deep research and development infrastructure with active acquirer markets. Several Nordic countries offer specific tax reliefs for qualifying startup founders. These environments are not the cheapest, but they provide reliable legal certainty and access to global buyers.

How Do Cross-Border M&A Regulations Complicate International Startup Exits?

Cross-border M&A regulations complicate international startup exits by adding review layers that neither the buyer nor seller controls. More than 100 jurisdictions now apply some form of foreign direct investment (FDI) screening. That number has grown sharply from a decade ago. Each review is independent, and a deal can clear one jurisdiction only to be blocked in another.

How Does CFIUS Review Affect Deals Involving US Buyers?

CFIUS review affects deals involving US buyers by adding a national security layer. It applies to any transaction where a foreign party acquires influence over a US business. In 2024, CFIUS reviewed 325 transactions. It imposed five civil penalties, the most ever in a single year. Its largest-ever penalty was $60 million, issued to a company that completed a transaction without required filings. CFIUS also opened 76 formal inquiries into non-notified transactions in 2024, a 27% increase from 2023.

CFIUS enforcement is intensifying. Founders selling to US buyers that have foreign investors on their cap table may trigger a CFIUS review. This applies even when the target company is not in the US.

A second layer of complexity took effect on January 2, 2025. A new outbound investment rule, sometimes called “reverse CFIUS,” took effect January 2, 2025. It restricts all US persons from investing in Chinese businesses developing AI, semiconductors, and quantum computing. This rule directly affects any cross-border exit where US investors hold equity in a startup with China-linked operations or acquirers.

How Does EU FDI Screening Add Complexity to European Exits?

EU FDI screening adds complexity to European exits by multiplying the number of regulatory bodies that must approve a transaction. EU Member States reviewed 3,136 transactions via national FDI screening in 2024. That is a 75% increase over the prior year. As of 2024, 24 of 27 EU member states have FDI screening legislation. Just 14 had it in 2019. The EU Parliament endorsed new, stricter EU-wide screening rules on May 8, 2025.

The UK’s Competition and Markets Authority (CMA) now operates as a third major regulatory body for cross-border tech deals. It works alongside the US Department of Justice and Federal Trade Commission. After Brexit, the CMA acts independently. A deal that clears EU and US review can still be blocked or conditioned by the CMA.

Deals involving Chinese acquirers are described by M&A practitioners as effectively non-viable for US-based acquirers and most EU targets. National security concerns mean that even commercially attractive deals are withdrawn before formal review.

How Do Currency and Repatriation Rules Affect Latin American Exits?

Currency and repatriation rules affect Latin American exits by adding cost and unpredictability to moving proceeds out of the country. Each country in Latin America has its own FX, tax, and capital repatriation rules. There is limited harmonisation across the region.

Brazil’s taxed foreign exchange environment creates friction for exit proceeds. Foreign acquirers must convert Brazilian reais into their home currency through Brazil’s official FX market. This involves registration requirements and additional taxes. Non-Resident Accounts (NRAs) reduce some documentary burden, but the process remains more complex than in Singapore or the US.

Argentina maintains strict capital controls and currency conversion restrictions. Acquisition proceeds can effectively be trapped inside the country. Founders operating in Argentina must plan exit structures that account for currency risk from the first day of operations. Colombia and Peru have more open capital accounts, making repatriation more straightforward.

What Questions Do Founders Ask Most Often About Regulatory Frameworks and Startup Exits?

Does it matter where I incorporate if I operate in Latin America?

Yes, incorporation jurisdiction determines which corporate law governs your exit. Most VC-backed startups incorporate in Delaware even if they operate in Latin America. Delaware offers the most predictable courts and investor-friendly legal defaults. Your operating country affects local tax and labour obligations, but it does not control the exit structure.

How long does a typical cross-border M&A deal take to close?

A straightforward deal without regulatory hurdles takes 3 to 6 months. Deals requiring CFIUS review, EU FDI screening, or multiple national antitrust approvals can take 12 to 24 months. Deals with China-linked parties are often withdrawn before formal review completes.

What is the QSBS exclusion and who qualifies?

The QSBS exclusion lets US founders exclude up to $15 million of capital gains from federal tax. To qualify, you must hold shares in a qualifying Delaware C-Corp for at least five years. The company must have had gross assets under $50 million when the shares were issued. This is one of the most powerful founder tax benefits available anywhere in the world.

Can I avoid capital gains tax in Latin America by using a Singapore holding company?

A Singapore holding company can reduce or eliminate capital gains tax at the holding level. You still owe local taxes on operations in each country. Brazil, Mexico, and Colombia each have withholding tax rules. These can apply when proceeds flow upward to a foreign holding entity. Retrofitting a holding structure after investors are on the cap table is complex and expensive.

What happens if an acquirer is in a country with FDI restrictions?

The acquirer’s home country is not the only relevant jurisdiction. CFIUS reviews the target’s US nexus. The EU reviews transactions affecting European markets. The UK’s CMA reviews deals with UK impact. You should identify all jurisdictions with a potential regulatory interest before signing a term sheet. Missing a mandatory filing can result in penalties of up to $60 million, as CFIUS demonstrated in 2024.

How do drag-along rights protect founders in an M&A exit?

Drag-along rights protect founders by allowing the majority to compel minority shareholders to sell. Without drag-along rights, a single minority investor could block an otherwise agreed acquisition. The key risk is procedural failure. Courts have voided drag-along rights when majority owners skipped required advance notice steps. Every drag-along clause must be drafted precisely and followed exactly when invoked.

Ready to Plan Your Startup Exit Strategy?

Exit planning starts long before a buyer calls. Your incorporation country, tax structure, and investor rights all shape your eventual outcome. At The Startup VC, Craig Dempsey’s team has built and exited companies across Latin America. We understand the legal and regulatory terrain in Brazil, Colombia, Mexico, and Chile. We also understand cross-border transactions with US and European buyers. Whether you are structuring your first cap table or navigating an acquisition, we offer practical, experience-backed guidance.

Contact us today to discuss your exit strategy.